IIMS Journal of Management Science

Search

Search

Gaurav Talwar1 and Sabyasachi Sinha1

and Sabyasachi Sinha1

1 Indian Institute of Management Lucknow, Uttar Pradesh, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Banks and financial institutions have been experiencing slow growth after the financial crisis due to loss of trust, regulations, changing customers and digital disruption unleashed by fintechs. While the emergence of fintech is a global phenomenon, we are starting to see some standout banks collaborating efficiently with them to help self-renew themselves and, in turn, win back customers, improving margins, bolstering growth aided by data insights, simplifying operations and acting with speed to customer requirements. Enhancing scope and scale at speed supported by fintech collaboration is helping these banks to manage better uncertainty, front load benefits to end consumers, orchestrate capabilities, manage change and navigate the complexity associated with climate and corporate governance actions.

FinTech, digital transformation, banking and financial services, startups, strategic renewal, corporate governance, climate change

Introduction

The 2008–2009 financial crisis brought about an irreversible transformation in the financial industry’s structure. A pervasive lack of consumer confidence in banking and financial products prevailed, prompting a widespread preference for cash over traditional financial instruments. This crisis-induced mistrust persisted beyond 2010, forcing banks and financial institutions to confront the challenge of regaining the trust of their customers. Simultaneously, the emergence of high-speed mobile internet and touch-enabled smartphones initiated a seismic shift in consumer preferences, while new regulatory measures further complicated the industry’s dynamics. Climate and corporate governance issues began to take centre stage, reshaping financial institutions’ operations.

The financial sector found a panacea in digital transformation catalysed by financial technology (fintech). It brought banking services just a click away from consumers, enabling them to access their accounts and perform many financial transactions. This self-service approach restored trust and bolstered confidence in financial institutions. For banks that had grappled with the aftermath of the crisis for several years, embracing fintech represented a means of strategic renewal. Strategic renewal, a concept now essential in the corporate world, involves adjustments to the strategic direction of an organization to ensure long-term competitiveness.

Recent research underscores the transformational impact of electronic and digital banking on the financial sector. Digitization enhanced cost control and profitability while facilitating an exponential increase in customer base and retention. Climate concerns, regulatory pressures, technological advancements, shifting customer expectations and competition from fintech entrants have made the financial industry question its long-term survival and evolving role.

The future for traditional retail banks appears uncertain, yet the blueprint for their survival might be found in industries like automotive, where transformative technologies have driven unprecedented innovation. Fintechs are redefining banking services worldwide, igniting revenue growth, and facilitating digital transformation. The omnipresence of digital technology, driven by fintech, is causing disruptions in various industries, urging incumbents to embrace offensive strategies that leverage digital capabilities. Global banks’ recent strategic renewal initiatives have emphasized their vulnerability to change, driving them to collaborate with technology, media and telecom companies. As the industry continues to consolidate, the influence of fintech disruption in embracing change becomes increasingly evident.

In this article, we delve into how fintech has been instrumental in helping banks regain their growth trajectory and rebuild trust through digital transformation. We explore the diverse strategies employed by banks across the globe to leverage fintech. While local variations play a role, digital transformation through fintech is a global trend with standard best practices that large financial institutions have adopted to renew themselves strategically and remain relevant in a dynamic market. We also highlight the unique capabilities of fintech supporting strategic renewal and present an emerging framework for adoption, outlining imperatives for banks seeking to embark on their renewal journey. Climate and corporate governance are central themes intertwined with this transformation, making it an all-encompassing revolution in the financial sector.

Theoretical Background

In the financial crisis of 2008–2009, consumer confidence in banking and financial products was at an all-time low, with a majority holding cash rather than putting in any financial instruments. Though by 2010, the financial crisis was behind, banks and financial institutions were still grappling with customers’ acceptance of financial instruments. Consumer preferences were changing, coupled with the emergence of high-speed mobile internet and touch-enabled phones. With new regulations coming in, financial institutions faced the dilemma of winning back trust and meeting changing customer requirements.

The digital transformation powered by fintech happened as a panacea for financial institutions. It brought the bank a click away from the customer; now, the customer can access his bank account and do almost everything he wishes. Self-serving was game-changing as it helped win back trust and gain confidence. Banks, struggling for 3–5 years post-financial crisis, started seeing fintechs as a means for strategic renewal.

Figure 1. Consumer Trust Deficit with Banks.

Strategic renewal has become an essential theme in today’s time with traditional firms looking to reinvent and reinvigorate themselves with significant new disruptions coming either from new competitors or technologies or ecosystem-related changes, which makes them do a course correction or change the way they used to operate before (Chaola et al., 2015). Strategic renewal involves initiating change and achieving a shift in strategic direction that can ultimately shape the long-term competitive position of a firm, often leading to a fundamental alteration of the original foundation (Schmitt et al., 2018). Banks which were historically struggling by adopting digital technologies powered by fintech not only helped self-serve customers but also increased the profitability of banks by making the existing staff focus on playing more of an advisory role and thus assisting banks to grow.

A recent study (Gautam, 2012) revealed how electronic and digital banking had helped banks and financial institutions leapfrog competition by improving profitability and margins. Digitization has helped them have much stronger control over cost and enable them to earn near-term profits. This transformation from traditional to digital banking has helped banks gain a significant competitive advantage, helping them increase their customer base manifold and providing a much more accessible platform for retention. Global banks like HSBC have started piloting smartwatches for mobile banking and are conducting pilots with technology providers in this space (Maras, 2018). A lot of this has been achieved through innovative alliances with fintech players or, in some instances, acquiring those to leapfrog the learning curve quickly and offer innovative digital services to its customers. Emirates NBD bank has been partnering with fintech firms to enable biometric-based logging capability and using mobiles to seamlessly ease cheque deposit facilities, saving precious time (Al-Zubaidi, 2021). Resource fit analysis of external demands and resource/capability mix has helped provide a pioneering framework to evaluate how digital transformation is helping clients grow and stay relevant (Liu, Chen, & Chou, 2011). The financial services sector is undergoing significant shifts, from ever-increasing regulatory pressures to rapid changes in technology, changes in customer expectations and loss of business revenue to new entrants (e.g. fintechs). The sector has faced sluggish growth since the last financial crisis, and traditional organizations are experiencing high cost/income ratios due to capital and human-intensive processes and lower levels of automation and digital enablement. How will the traditional institutions—retail banks—survive for the next 100 years? What does the future hold, and do they all become platform and technology companies with a banking license? How will their business model evolve, and what role will technology play in this transformation at an industry level? Banks and financial institutions, while heavily consumer-focused, can take examples from traditional industries that have leapfrogged into the digital age. A case in point is the automobile industry, where Tesla Model S off-the-air updates allow Tesla to offer superior customer service and experience at scope, scale and speed never imagined before.

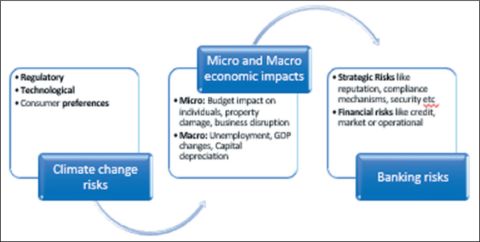

Effective corporate governance hugely impacts the banking industry’s response to climate change (Furrer et al., 2012). This significantly impacts policies, sustainable investment practices and risk management. The role of the chief executive, leadership, board of directors and the various regulatory bodies has become of immense importance (De Andres & Vallelado, 2008). They play a pivotal role in ensuring environmentally friendly decision-making in banking institutions.

Figure 2. Climate Change to Banking Risks.

Green fintech has been gaining ground, especially in the Western economies. Puschmann et al. (2020) discusses how fintech in Switzerland has facilitated the movement to a low-carbon green economy. The entire spectrum of green financing, carbon neutrality through sustainable investment practices and leveraging digital platforms to promote climate-friendly banking and financial services is gaining ground across the globe. This also significantly has become a phenomenon where banks are increasingly seeing it to renew themselves strategically to be relevant and, at the same time, be environmentally conservative.

Fintechs are helping reinvent services offered by banks across the globe, increasing the global retail banking revenues, the digital concept implementation of banks and the digital transformation of these banks in retailing service. An offensive strategy utilizing fintechs involves disrupting existing processes and systems and aggressively moving to new digital models. Companies following the offensive play are reporting superior earnings growth. Incumbents are reluctant to overhaul legacy systems due to inertia, and the ability to orchestrate and be strategic about the change can strain already constrained resources and lead to their nemesis.

The last few years have seen some major strategic renewal exercises conducted by global banks as they have concluded that they are no longer immune to change. The increased adoption of mobiles, e-commerce and live interactions has led the financial services industry to increasingly collaborate with technology, media and telecom companies to continue strategic renewal. Financial services industry consolidation has been going on for some years. It is gathering steam, especially in the last few years, with fintech disruption playing a pivotal role in banks embracing change.

Research Objective

This article discusses how fintechs have helped banks get back to growth and win trust by digitally transforming them with green, environmentally conducive priorities. The article’s research objective is to dive deep into how fintechs are aiding strategic renewal in banks in the context of climate change and corporate governance. Banks have taken various routes to leverage fintechs, and as part of this research, we have covered banks across the globe as it is a global phenomenon rather than being restricted to a region. What we also notice is that while local nuances do play an important role, the phenomenon of leveraging fintechs for digital transformation to transform operations is more of a worldwide phenomenon with certain standard best practices that these large financial institutions have adopted to be successful in strategically renewing themselves in this carbon sensitive market and stay relevant. We also find unique capabilities of fintechs supporting strategic renewal and showcasing an emerging framework for adoption and imperatives for banks as they look to join the bandwagon for renewing themselves and doing right ethically and in an eco-friendly way.

Methodology

As a part of the research exercise, the first step was narrowing down on a research question that has yet to be delved into much literature but offers scope for enhancement and enlightenment of academia. While stand-alone, we find research on the strategic renewal of banks and fintech evolution; there have been only peripheral studies on how fintechs are fuelling a strategic revival in banks. As part of the search strategy for doing a focused search, we used the SPICE (Setting, Perspective, Intervention, Comparison, Evaluation) model. All medium to large-size banks across the globe, pure-play fintech and technology-driven digital natives present across towers like fintech, insuretech and agritech were part of the inclusion criteria. Coverage ensures that all large regions are covered. Excluded from the search were small size banks (< $100 million in revenues), Chinese and Japanese banks; while some of them are large, not much information is available on them in English; recently formed banks, that is, telecom players getting banking licenses are not part of the search. As part of the strategic literature review, several databases were evaluated, these included EBSCO, Web of Science, Venture Intelligence-M&A, Financial Times, Elsevier.

Also, a detailed systematic literature review was conducted. The broader context of this study is to investigate how banks’ strategic renewal is aided by fintechs when corporate governance and climate actions are centre stage. A systematic literature review is conducted to help support the interpretation of all available research on a specific area or phenomenon of interest (Kitchenham et al., 2009). A systematic literature review serves to unveil new perspectives and unexplored domains within studies. This method facilitates the accumulation of evidence from research across diverse contextual settings and enables the extraction of informed insights. The systematic literature review is typically structured around three distinct phases: planning, conducting and reporting the review.

The planning phase in this context involved elaborating on the research, establishing the protocol and validating the review protocol. The protocol, serving as a set of guidelines, aimed to mitigate bias in the study by delineating the conduct of the systematic review and specifying the criteria for study selection. As per the defined protocol for this systematic literature review, previous primary research has been limited to top management journals, with a focus on strategic renewal in banks across various context settings such as climate change and sustainability.

Following the definition of the selection criteria, the subsequent stage involved meticulous and practical screening to ensure alignment of the selected studies with the area of interest, strictly adhering to the established protocol and criteria to manage the review process effectively. This process was carried out by thoroughly reviewing the abstracts of the articles (Gopalakrishnan & Ganeshkumar, 2013). The primary objective during this process was to uphold the comprehensiveness of the review. To achieve this, the broad criteria included considerations such as content relevance, language, publication in esteemed journals and the number of citations to gauge the extent of influence. By applying practical screening methods, the initial list was effectively narrowed down to lesser number of articles that met the specified criteria.

In the subsequent stage, a quality appraisal of the refined articles was undertaken to ensure compliance with minimum quality criteria and to assign a quality score to each article (Gioia, 2021). The output of the systematic literature review is directly influenced by the quality of the included articles, hence the importance of this step. Quantitative appraisal of the study involved a comprehensive assessment of an article’s data collection methodology, analysis, results and conclusions. Conversely, qualitative appraisal utilized a broader assessment of the claims presented, the evidence supporting these claims and the substantiation of the evidence. Following this rigorous quality check, the number of articles was further reduced, resulting in a manageable list of 50 articles for the review (Kitchenham et al., 2009).

Figure 3. Systematic Literature Review.

During the data extraction stage, the extraction of information from each article played a vital role in providing the input for detailed synthesis. The synthesis phase involved the aggregation, organization and comparison of articles to elucidate emerging themes and patterns from the various studies, aiding in the refinement of the research criteria. In the final step, the review was composed to report the findings and disclose any unexpected results or novel ideas for future research (Aznoli & Navimipour, 2017).

Examined studies which met the criteria laid above, specific precaution on the point that banks we narrow down on have had strategic renewal fuelled by fintechs. Following both the SPICE method and detailed systematic literature review led to us narrowing down on five banks where such phenomenon has played, and the routes taken by them to engage fintechs keeping in line with corporate governance and climate change requirements. Data was extracted on the banks displaying this phenomenon, and broader themes emerged from this related data were looked at to conceptualize and arrive at the framework and provide recommendations for a practice where clear arguments backed by quality evidence emerged.

Findings: Collaborating with Fintech to Grow and Better Serve Customers

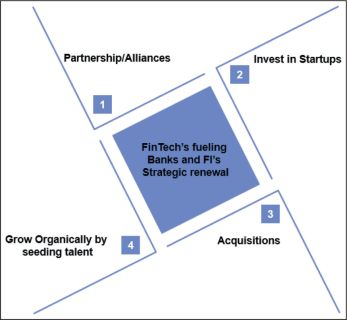

Routes Taken by Banks to Engage Fintech and Expand the Ecosystem

Banks are taking various ways to infuse innovation in the firms to remain competitive and relevant. Looking at the last few years, most major banks have increased their engagement with fintechs. Banks have been engaging with fintechs in multiple ways. Broadly, these routes can be classified into:

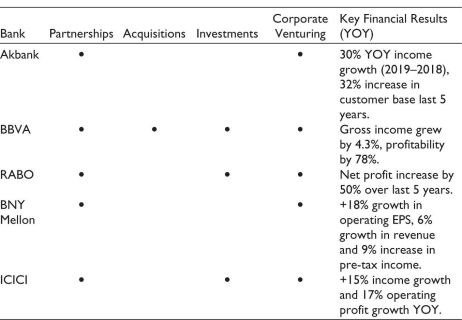

We analysed several leading banks using systemic literature review and SPICE methodology; we covered banking leaders across the globe to ensure this is a global phenomenon. While we looked at several banks as part of the study, we narrowed it down to five banks: Akbank, ABN AMRO, BBVA, BNY Mellon and ICICI as they have shown the most willingness in their regions to collaborate and harness agility, which is brought by fintech and also had highlighted environmental conservation as a priority. These took all the above-defined routes to market, and we highlight that through examples as we go deeper into each of the ways.

Route 1: Partnerships

The first and foremost path banks take is to build alliances and partnerships with leading fintechs to leapfrog on technologies, that is, Akbank partnered with Ripple for blockchain infrastructure and Daon for face recognition technologies to enable it to act quickly and offer superior customer experience. It has simplified its operations by building phygital branches, a mobile sales force and harvesting massive data to make frictionless customer journeys and channel optimization. This has led to a robust 30% increase in year-over-year income for Akbank and an increase in customer base by 4.2 million (+32%) over the last five years by front-loading benefits to the end customer.

Figure 4. Routes to Engage Fintechs.

The European banking industry has witnessed significant changes after the financial crisis, Brexit and Euro depreciation. These changes have affected the structure of the operations, along with how these changes can have a multiplier effect through interaction and reinforcement. When it comes to strategic renewal, attitude and how fast you can move directly impact renewal projects, Rabobank has uniquely pioneered how it utilizes innovation processes to respond and anticipate changes in a more predictable way (Smits & Groeneveld, 2001). Rabobank has had a history of being a leader in innovation. It was one of the few banks globally to recognize the power of online banking to build an organizational structure and buffers against environmental turbulence (Hensmans et al., 2001). Through its innovation focus, Rabobank could perceive competition from KPN DT (incumbent telecom players who evolved into payment banks). It was able to offer its customers many more functionalities and features through partnerships with fintech by running marquee programs like Rabo Frontier Ventures Rabobank Innovation Fund. It has also partnered with the leading trading platform. Trade for a blockchain project and Peaks, an investment app to help cattle farmers track herds with mobile tracking technology leveraging data insights and simplifying how it operates. This has aided Rabobank to significantly improve its profitability, with net profits increasing by over 50% in the last five years.

BNY Mellon has partnered with Volante for pay-tech innovation by creating and deploying technology to ensure real-time payments in the US and internationally; it also has partnered with likes of The Clearing House to ensure real- time payments and Zelle for peer-to-peer payments successfully. BNY Mellon showed +18% growth in operating Earning per Share (EPS) with a healthy 6% growth in revenue and 9% in pre-tax income.

ICICI has been at the forefront of embracing digital change and was one of the first Indian banks to leverage design thinking workshops leveraging IDEO methodology to enable digital transformation (Adhikari & Ghosh, 2022). By partnering with fintech, they want to provide superior customer service, improve financial services, delight customers and have a robust control mechanism to meet all regulatory requirements (Bhutani, 2014). It has recently partnered with IndoStar to finance commercial vehicles and target small and medium fleet owners. It has also partnered with Open Financial Technologies Pvt Ltd to create and deploy an integrated payments platform for micro, small and medium enterprises. Innovating through partnerships also shows up in results, with fee income growing 15% year-over-year and operating profit improving by 17% year-over-year in 2019.

Route 2: Investment in Fintechs

Not to miss the fintech blitz, central banks have also started investing in early-stage fintechs to leapfrog the technology curve and be able to offer services at speed and simplify their operations. For BBVA’s corporate entrepreneurship division, BBVA Ventures has, over the years, continued to be an innovator by actively investing in disruptive technologies, that is, SumUp, which enables point-of-sale payments through mobile; Radius, which is gaining significant ground in the US by providing business analytics and insights to SME businesses; Freemonee, which customizes and creates relevant offers from retailers by analysing transaction data and Ribbit Capital, which fintech-focused Venture Capital (VC) initiative. These partnerships and investments over the years have provided significant data-driven insights that simplified how it serves its customers at speed; this has helped BBVA leapfrog competition and shows up in promising results, with gross income going up by 4.3% and net attributable profit up by close to 78%.

Rabobank is injecting an additional €80 million into its venture fund, effectively doubling Rabo Frontier Ventures’ commitment to €150 million, thereby providing the opportunity to broaden its investment focus to global hubs. It has recently invested in an early-stage startup facility that provides an accounting tool for freelancers, making accounting extremely easy for entrepreneurs. It has also invested in KOMGO, which is helping move commodity trade to blockchain and thus providing a fully decentralized solution for data exchange to the industry. Also, it recently announced a tie-up with Facturis Online to help move the entire invoicing process online and make seamless and faster-making operations simple and agile with the customer at the centre of the solution.

ICICI Bank has invested over 100 crores (Sharma, 2013) in the last few years to make early-stage investments in fintech. One of the critical investments is Fingpay, which allows merchants to accept payments through biometric technology, and Arteria, which offers supply chain solutions on Cloud and payments.

Route 3: Acquisitions

We have also begun to see some acquisitions by the leading players to give them an edge over the competition. BBVA has been a first mover in this space, and seeing the widespread adoption of mobile and ease of internet availability, it acquired a leading fintech, an American online banking platform, Simple, as part of its digital transformation and showed how it significantly improved its digital properties and gained a significant advantage by this buyout (Wisniewski, 2014).

Simple will reinforce our global digital transformation while BBVA will provide the ways and means to help Simple maximize its strong growth potential. —BBVA Chairman & CEO, Francisco González

Source: BBVA.com.

Route 4: Organically Seeding Corporate Venturing Effort to Seed Fintech Expertise

Witnessing the kind of growth that fintech has seen, most central banks have started internal ventures and corporate initiatives, carving out units that are much more entrepreneurial and customer-facing than traditional banks have begun. We look at some of the key initiatives the five banks, mentioned earlier, took.

Akbank had a legacy of being the best in financial services in Turkey (Erol et al., 2013), but it very quickly realized that for it to continue to maintain its position and reputation in the digital era, it had to strategically renew itself very quickly for continued dominance and relevance with its customers. Through Akbank Labs and periodic hackathons, it has started offering innovative solutions and products with collaboration from fintechs and regularly conducting proof of concepts with startups to further partnerships. It has started offering digital banking services under Akbank Direkt, providing real-time financial services. BBVA continues to renew itself by thinking ahead of the curve and innovating to serve its customers. As stated by its CEO:

We innovate to serve a client that is changing. —Eduardo Torres-Llos

Source: BBVA.com.

The bank was a first mover concerning digital transformation in the markets it operates and continues to report a healthy increase in customers using its digital channels, offering almost 95% of its services through the digital channel as of date, translating into better customer service and results for the bank overall.

Digital transformation is having a positive impact on our business and is ensuring the sustainability of results in the future, as evidenced in terms of growth, transactionality, productivity and efficiency. —OnurGenc, CEO of BBVA

Source: BBVA.com.

Not so long before, CEO Francisco Gonzalez had predicted that many banks might fail for not undergoing a digital transformation and highlighted the adoption of digital banking technology by BBVA as of 2015.

Through its growth and innovation-focused arm, Teckle, Rabobank has been helping startups scale and partner and has now expanded its presence across the Netherlands. Further, Rabobank has launched a €60 million VC fund through its RABO Frontier Ventures to proactively incubate some of these technologies internally to offer its customers quicker service.

BNY Mellon has, in a way, ‘platformed’ the financial services industry by coming together with a much simpler digital platform where both its employees and customers are contributing to building the landscape and initiating services without building them up from scratch and improving effectiveness in the financial market through usage of digital technology.

Fintech innovation significantly impacts Indian banks, with fintech at the forefront of bringing cutting-edge technology and click-click business models to the 125 crores+ aspiring and prospering Indian diaspora. Since the reforms started in 1991, Indian banks have continued on a consistent transformation journey post-liberalization, privatization and globalization. They are constantly seeking best practices from the Western world and offering products and services to their consumers (Rani & Rani, 2018). ICICI bank has been aggressively opening innovation labs, taking the organic route to fintech adoption, investing smartly in promising fintech startups and partnering with them to build and innovate cutting-edge digital technologies (ICICI fintech). It has also spearheaded a software robotics initiative in-house and moved to process a million transactions onto software robots, automating almost 20% of its transactions.

Table 1. Summary of Key Banks and Routes to Engage Fintechs with Crucial Impact on Financial Results.

We want to be digital at the core, remove the paper and as many people as possible and have end-to-end processes driven by technology. —B. Madhivanan, Chief Technology Officer, ICICI

Source: ICICI.COM.

As we saw, while some banks took all the available routes to market, some focused on specific routes to leverage fintechs and bolster results. All the leading banks showed improvement across the reported financial parameters compared to previous years aided by fintechs.

An Emerging Framework for Adoption

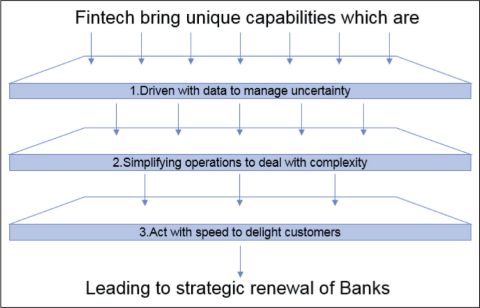

As we saw from the above examples, banks have taken various routes to engage with fintech and have shown strong uptake concerning the financial results. The standouts have collaborated with fintech to leverage data insights better, act with speed and agility to delight customers and massively simplify how they operate to deal with complexity; this has aided banks in strategically renewing themselves in the changing market dynamics.

The key imperatives which emerge from this adoption on how fintech aid the strategic renewal of banks collaborating successfully.

Imperatives for the Adoption of Fintech: Aiding Strategic Renewal of Banks by

Figure 5. Emerging Framework.

Figure 6. Imperatives for Adoption by Fintech.

Discussion and Implications

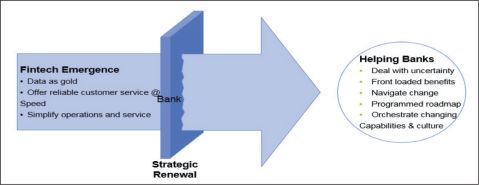

Global financial institutions have realized the potential of fintech and how it helps them operate efficiently and offer better customer experience. However, most of them face an uphill task with digital disruptors or digital natives and how they completely change the way they do business. From the insights drawn from above, we find banks and financial institutions have either learned, built alliances or acquired these digital disruptors (fintechs). Banks have also begun to strongly appreciate how these fintechs, aka digital native companies built on data and focus on business intelligence, follow where the data leads, are relentless about designing and improving the client experience, and move quickly with speed improving things on the go. The article also highlights how fintech aids corporate governance and climate change actions. While financial institutions traditionally have been bureaucratic and slow, adopting and working closely with these fintechs is no longer a choice but a compulsion to stay in the game. We see a few emerging points from these leading banks that have successfully engaged with fintech as follows:

Conclusion

While several banks appreciate the lead of adopting fintech and the power it brings to the consumer, very few banks and financial institutions have embraced fintechs. They are using it to provide superior customer service. While technologies, including Cloud, analytics, security and blockchain, are all-pervasive, most of the senior executives in the banks need to be prepared and more knowledgeable on how this transformation will take place. The benefits of adopting digital or partnering with fintech only happen if you look beyond technology adoption and listen to making your organizational structure nimble and carbon-neutral and building a network of relationships across the ecosystem. Banks and financial institutions looking to adopt or partner with fintechs should not limit their thinking to the current environment but must see how it impacts future operating models. The network of relationships, also called ecosystems, is the key to the digital world. How you collaborate with technology startups or large digital companies is fundamental to how well you can tread the path of digital transformation, offering the needed transparency. By 2025, if not sooner, most banks and financial institutions will find digitization at the core of everything they do. The future of banking and financial services is to embrace scope, scale and speed, leveraging and collaborating with technology startups, partnering, acquiring or investing in them not only to gain a first-mover advantage but also to gain a mover advantage at size and scope by building simplified internal processes which recognize and respond to customers to this change. Banks and financial institutions that appreciate the power of technology and connectivity and leverage scale, scope and speed will outshine the journey to the digital future, witnessing exponential growth while being on the right side of corporate governance and climate action.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Gaurav Talwar https://orcid.org/0000-0002-5967-3811

Adhikari, K., & Ghosh, A. (2022). Size and financial performance: A study of Indian life insurance sector. In N. Barman (Ed.), Research trend in business and economics (pp. 39–47). REDSHINE Publication.

Al-Zubaidi, A. P. D. M., & Alsaadi, A. H. H. (2021). Technology of financial and technical information and its contribution to improving the financial inclusion of the Iraqi banking sector for the period from (2014-2018): Exploratory study. Al-Qadisiyah Journal for Administrative and Economic Sciences, 23(2), 146–152.

Aznoli, F., & Navimipour, N. J. (2017). Cloud services recommendation: Reviewing the recent advances and suggesting the future research directions. Journal of Network and Computer Applications, 77, 73–86.

Bhutani, P. (2014). Challenges before Indian financial sector in information age. CLEAR International Journal of Research in Commerce & Management, 5(12).

Chaola, P., Pratoom, K., & Raksong, S. (2015). A conceptual model of strategic management renewal orientation and firm performance. Proceedings of the Academy of Strategic Management, 14(2), 18–31.

De Andres, P., & Vallelado, E. (2008). Corporate governance in banking: The role of the board of directors. Journal of Banking & Finance, 32(12), 2570–2580.

Erol, C., Seven, Ü., Aydo.png) an, B., & Tunc, S. (2013). The Impact of Financial Restructuring after 2001 Turkey Crisis on the Risk Determinants of Turkish Commercial Bank Stocks. International Journal of Economic Perspectives, 7(4).

an, B., & Tunc, S. (2013). The Impact of Financial Restructuring after 2001 Turkey Crisis on the Risk Determinants of Turkish Commercial Bank Stocks. International Journal of Economic Perspectives, 7(4).

Furrer, B., Hamprecht, J., & Hoffmann, V. H. (2012). Much ado about nothing? How banks respond to climate change. Business & Society, 51(1), 62–88.

Gautam, V. (2012). Measuring the impact of new technologies through electronic-banking on profitability of banks: Evidence form Indian banking industry. Romanian Journal of Marketing, 3, 20–26.

Gioia, D. (2021). A systematic methodology for doing qualitative research. The Journal of Applied Behavioral Science, 57(1), 20–29.

Gopalakrishnan, S., & Ganeshkumar, P. (2013). Systematic reviews and meta-analysis: Understanding the best evidence in primary healthcare. Journal of Family Medicine and Primary Care, 2(1), 9–14.

Hensmans, M., Van Den Bosch, F. A. J., & Volberda, H. W. (2001). Clicks vs. Bricks in the emerging online financial services industry. Long Range Planning, 34(2), 231–247.

ICICI. (n.d.). ICICI Digital. https://www.business-standard.com/article/finance/icici-bank-s-digital-push-sets-up-innovation-lab-enters-fintech-tie-ups-118052500580_1.html

Kitchenham, B., Brereton, O. P., Budgen, D., Turner, M., Bailey, J., & Linkman, S. (2009). Systematic literature reviews in software engineering – A systematic literature review. Information and Software Technology, 51(1), 7–15.

Liu, D., Chen, S., & Chou, T. (2011). Resource fit in digital transformation: Lessons learned from the CBC Bank global e-banking project. Management Decision, 49(10), 1728–1742.

OnurGenc. (n.d.). Digital Transformation BBVA. Digital transformation is having a positive impact on our business and is ensuring the sustainability of results in the future, as evidenced in terms of growth, transactionality, productivity and efficiency. –OnurGenc, CEO of BBVA

Puschmann, T., Hoffmann, C. H., & Khmarskyi, V. (2020). How green FinTech can alleviate the impact of climate change—The case of Switzerland. Sustainability, 12(24), 10691.

Rani, V., & Rani, A. (2018). Current practices of e-banking technology: Study of service quality in Tricity (Chandigarh, Mohali & Panchkula). Journal of Commerce & Accounting Research, 7(2), 56–67.

Schmitt, A., Raisch, S., & Volberda, H. W. (2018). Strategic renewal: Past research, theoretical tensions and future challenges. International Journal of Management Reviews, 20(1), 81–98.

Sharma, N. (2013). Analysis of Customer Satisfaction from E-Banking Services. A comparative study of HDFC and ICICI bank.

Smits, H., & Groeneveld, J. (2001). Reflections on strategic renewal at Rabobank-A CEO perspective. Long Range Planning, 34(2), 249–258.

Wisniewski, M. (2014). Why BBVA Compass is sending customers to an online rival. American Banker, May, 8.