IIMS Journal of Management Science

Search

Search

Ronald Ebenezer Essel1

1 University of Cape Coast (UCC), College of Distance Education (CoDE), Unit of Business Programmes, Cape Coast, Ghana

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This inquiry examined the moderating influence of board size, board independence, and board gender diversity on the association between corporate social responsibility (CSR) and firm performance (FP) in Ghana. It utilized data from audited financial statements of all 36 firms listed on the Ghana Stock Exchange, spanning 2010–2020. The study espoused system-GMM for the empirical estimation. Findings show that CSR demonstrated significantly positive relationship with FP, consistent with the stakeholder theory, which is aligned with Carroll’s four-factor-pyramid theory but inconsistent with the agency cost theory. Again, findings depict that all three board structure elements moderated the relationship between CSR and FP.

Board size, board independence, board gender diversity, corporate social responsibility, firm performance

Introduction

Corporate social responsibility (CSR) and corporate governance (CG) issues have become very crucial for firms’ success in today’s competitive global business environment. Business success is dependent on how well management decisions are made. These managerial decisions are also hugely affected by the composition and quality of the board of directors (BOD). This is because some vital managerial decisions may have to go through BOD approval before implementation. CSR has egressed as one of the significant concerns of managers given the heightened cognizance, evolving ecological/sustainable demands and attention/pressure originating from regulatory authorities, policy-makers, the media, industrial practitioners, researchers/academia and the general public (Oduro & Haylemariam, 2019). Consequently, firms are progressively divulging information concerning their CSR activities. This is in the quest to satisfy stakeholders and to establish positive brand images to gain competitive advantages in the business environment, thereby creating value for shareholders (Ratnasari et al., 2021). CSR disclosure aids businesses to boost investors’ confidence in investment decisions.

There is no universally explicitly accepted definition of CSR as its definition has evolved in a manner that integrates economic, social, environmental, and sustainable developmental facets into corporate strategy (Babajee et al., 2022; Singh & Misra, 2021). CSR is a firm’s governance strategy, considered international private voluntary corporate self-regulation (Sheehy, 2015), as those activities are not obligated by the civic administrative authorities in most regulatory jurisdictions. Such activities are deemed societally and ecologically friendly, ethical, and beneficial and contribute to a stronger firm’s brand image. Carroll (1991) categorized CSR as a pyramid of responsibilities, with economic responsibilities at the base, followed by legal, ethical, and discretionary/philanthropic responsibilities.

The European Commission (2001) defines CSR as activities that permit businesses not only to fulfil their mandate but also to exceed it and invest in an employable workforce in their communities and solidify stakeholder relations. Whereas some shareholders view CSR activities as an interruption of the firm’s fundamental objective of shareholder wealth maximization, other stakeholders’ especially top-level management view CSR as a societal obligation with enormous financial rewards to the business, which can serve as a recipe for solving the agency problem. A corporation’s BOD, is one key structure, that business owners rely on via their mechanisms to solve the agency problem as their routine function of monitoring, supervision, strategic direction, oversight control, and proper governance bring into line, managers’ interests with those of non-management shareowners at the least feasible cost, thereby adding value to the firm (Feng et al., 2018). Different BOD dynamics may have different influences on decision-making as to whether to allocate resources or not for CSR activities. The BOD must be responsive to the core duties allotted them, not indulging in opportunistic activities and funds tunneling. BOD’s focus should be on strategically directing management to enhance the day-to-day running of the firm. The CG metrics of importance to this current study are board size (BS), board independence (BI), and board gender diversity (BGD). It is highly imperative to therefore examine the interconnectedness between CSR and board structure elements like BS, BI, and BGD to apprehend their combined moderating influence on listed firms’ performance in Ghana.

CSR-firm performance-(FP) nexuses have been and continue to be a subject matter of strong academic/scholarly research interest. Numerous studies have been performed to explore the influence of CSR on FP worldwide. Many of these studies were conducted in industrialized economies with scanty studies performed in emerging economies, such as Ghana (Babajee et al., 2022; Waheed, 2021).

Extant literature indicates that several inquiries that assessed the association between CSR and FP yielded either positive (Babajee et al., 2022; Feng et al., 2018; Javeed & Lefen, 2019; Nyeadi et al, 2018; Waheed et al., 2021); negative (Hirigoyen & Poulain-Rehm, 2017), neutral (McWilliams & Seigel, 2000), insignificant relationship (Okafor et al., 2021) or U-shaped/inverted U-shaped relationship (Grassmann, 2021).

Authors such as Babajee et al. (2022) and McWilliams and Siegel (2000), attributed the mixed results to the diversity of data sources, differences in investigational periods, contextual variances and flawed econometric specifications, in particular, the usage of static regression models, that ignored the elements of dynamism and also failed to control for endogeneity, heterogeneity, heteroscedasticity, simultaneity and reverse causality issues. Moreover, Babajee et al. (2022) are of the view that simulating pecuniary performances of businesses is a non-static activity, and therefore, applying static regression models in such a scenario produces spurious/biased/inconsistent results. It is, therefore, highly imperative to examine those variables that aid in explicating the inconclusive empirical findings. This necessitates further inquiries into the association between CSR and FP.

While authors like Galbreath (2018) and Saleh et al. (2020) are of the view that subsequent studies should consider the possibility of moderating the relationship between CSR indices and FP metrics to strengthen the said relationship, as the direct link is regarded too simplistic, others such as Waheed et al. (2021) have called for deeper/further investigations from ensuing researchers on the influence of CSR on FP in developing countries like Ghana, where the literature of this kind is near-absent. This current study, therefore, investigates the moderating role of board structure elements like BS, BI, and BGD on the relationship between CSR and listed companies’ performance in Ghana, deploying a robust system-GMM to address this ignored phenomenon.

The main goal/aim/objective/purpose of this inquiry is to empirically explore the moderating role of board structure metrics of BS, BI, and BGD in the association between CSR and FP in Ghana, a lower-middle-income West African country, south of the Sahara.

The contribution of this study to the extant literature is the exploration of the moderating influence of BS, BI, and BGD on the association between CSR and the performance of firms listed on the GSE, which to the best of the author’s awareness is the foremost research to examine such moderating associations in Ghana. By utilizing a robust dynamic panel system-GMM, this inquiry adds to the extant literature in view of the fact that it deals with the non-static nature of pecuniary performance simulation (Babajee et al., 2022) in addition to probable unobserved heterogeneity, heteroscedasticity, endogeneity, simultaneity, and reverse causality concerns likely to be present in the CSR-FP literature.

The remaining sections of this article are organized in the following manner: The second segment reviews the theoretical and empirical literature and formulates the study’s hypotheses. Data and research methodology follow in section three. A presentation and discussion of the research results are provided in section four. Limitations and areas for further inquiries are offered in the fifth segment. Conclusion, policy, and managerial implication relevance end the study in section six.

Literature Review and Hypotheses Development

Theoretical Literature

Underpinning Theories: Carroll’s Theory and the Stakeholder Theory

This study presents Carroll’s 4-factor Pyramid theory as the chief basis for a firm to undertake CSR activities in Ghana. This is theoretically aligned with the stakeholder theory which explains that a corporation does not only exist to create value for its shareholders but also for the needs of diverse stakeholders like the employees, customers, suppliers, creditors, the general public, government, and state agencies, social, legal, ethical and community needs and is entirely required to create excellent relationships with such stakeholders. Managers are principally charged not only to seek stockowners’ interest but with the more social responsibility of synchronizing all stakeholder interests, harmonizing any arising conflict, and optimizing the aggregate gains over all times horizons.

Carroll (1979) provided a theoretical hypothesis that systematically explains indispensable portions of CSR, namely, (a) the constituent of CSR (b) The social issues to be addressed by corporate entities and (c) the organizational philosophy of social responsiveness. From Carroll’s perspective, CSR activities should commence from the base of the pyramid to the apex, that is, from economic responsibilities through to philanthropic responsibilities. When a firm fulfils its primary economic responsibility efficiently, then it can move to legal responsibility in that order. Carroll (1991) is of the view that the foremost stage in executing CSR is to engage in a business venture and realize profits. According to Carroll, profits are required to compensate providers of capital to the business. Furthermore, profits must be ploughed back into the business to sustain business growth.

The focal notion of Carroll’s theory is to implement CSR activities in an ordered format, which when implemented results in a positive relationship with FP. A business is recognized as societally responsible if it functions profitably, conforms to the law, engrosses in moral/ethical behavior and donates to society via philanthropic activities. Windsor (2001) asserts that pecuniary and lawful obligations are needed socially, ethical responsibilities are expected socially and philanthropic agendas are desired socially. When Carroll formulated his original theory in 1979, which metamorphosed into his four-element pyramid theory in 1991, it was vividly executed having American kind capitalist civilizations at the background. Nonetheless, Crane and Matten (2016) noted that all the strata of Carroll’s theory were useful in Europe. Similarly, Visser (2016) assessed Carroll’s theory in emerging economies especially, African economies, and contends that the classical Carroll’s theory differs in the order of arrangement in the African context. According to Visser (2016), in emerging economies, economic responsibility is regarded as the most important, followed by philanthropic responsibilities, then legal, and finally ethical responsibilities (Wayne, 2010). Given the above, businesses must shed light on the nature of the environment in which they operate before implementing Carroll’s concept. To maximize the gains associated with CSR, firms need to take into consideration the immediate community’s requirements and thus adopt projects that have an analogous fit with that society.

CSR of Firms in Ghana

In Ghana, firms that are considered good corporate citizens are awarded annually by The Centre for CSR, West Africa during the Ghana CSR Excellence Awards in various categories for their CSR engagements. The basis for the awards includes beneficiary-focused initiatives, commitment to sustainability, execution of outcome-focused CSR ingenuities for each period, and established allegiance to the tripartite bottom line (people, planet, profit).

The Ghana CSR Excellence Awards was instituted to ensure that corporate bodies become more socially responsible and sustainability conscious when undertaking their core business functions. To improve the livelihood of the people in their operating environs, the types of CSR firms in Ghana engage in include the building of mechanized boreholes and provision of portable drinking water in the remote countryside, sanitation projects, schools, provision of scholarships to needy but brilliant students, sports sponsorships, financial supports to orphanages and needy institutions, market places, lorry parks, community centers, health facilities, electrification projects, road construction among other CSR projects. Concerning firms mining in Ghana, the Ghana Chamber of Mines require them to allocate at least US$1 of their operating income per ounce of Gold and also one percent of their earnings after interest and tax to aid repair the damages caused in their respective communities of operations (Source: Ghana Chamber of Mines, 2011). Several corporate entities (e.g., Fan Milk Limited) have also signed on to the UN Global Compact initiative that ensures that they operate in an ethical and socially responsible manner and act as good corporate citizens. CSR decisions of foreign firms operating in Ghana are mainly guided by legal prescriptions, those of the indigenous Ghanaian firms are guided mostly by discretionary and social considerations. The socially oriented CSR practices of the local firms are consistent with cultural expectations in Ghana that those with extra resources should support the less privileged members of the society. The empirical-based extant literature established that contemporary CSR in Ghana is framed within the context of development and reflects voluntary corporate self-regulation (Amo-Mensah, 2021) as the legal and legislative framework regulating CSR activities in Ghana is quite different from those in other emerging market economies. While in other emerging market economies, CSR are government-led, where company CSR decisions are guided by national laws, CSR activities in Ghana reflects a corporate self-regulatory approach, where, CSR laws have not been explicitly enshrined in any national legislation (Amo-Mensah, 2021). In addition, Ghanaian cultural values and principles had always shaped the CSR activities of businesses that operate in Ghana, thus making the kind and type of CSR firms undertake in Ghana quite unique and distinct from those of other emerging market economies (Amo-Mensah, 2021).

Empirical Literature

CSR and FP

CSR describes the sense of accountability businesses have for the societies they operate in and at the same time enhancing FP. The conventional method of CSR refers to the communal and ecological constructs, lead organizations to realize sustainable performance (Yong et al., 2022). CSR assists companies in eradicating or lessening the conflicting contentions institutional agents, that is, corporate managers and business owners (Sial et al., 2018), thus solving the agency problem within the firm. CSR undertakings create interpersonal resources and moral capital which enhances a company’s performance (Wang et al., 2008). CSR programs show a dip in employee resignations and raise workers’ loyalty (Santos, 2011), improve customer satisfaction level (Saeidi et al., 2015), increases client commitment (Weber, 2008), and assist companies to enhance their general reputation (Tencati et al., 2004).

The aforesaid dynamics support companies in reducing the transaction cost and increasing FP (Manchiraju & Rajgopal, 2017; Sprinkle & Maines, 2010). Those companies that engender sufficient and extra earnings are ardent to show social and environmental revelation in their reportage (Ho & Taylor, 2007). Besides, social-influence philosophy posit that CSR affect FP positively and enhances the communal relations of the firm (Cornell & Shapiro, 1987). Good corporate citizens convey pecuniary rewards to the institutions, thus reinforcing the connection between CSR and FP (Khan et al., 2020).

Information from prior studies reveals that CSR is an efficacious means, adeptly making institutions to realize greater performance (Lu et al., 2020). Supporters of the direct association between CSR and FP advocate that CSR enhances a company’s image/value, which further surges the long-run financial performance of firms. Undoubtedly, CSR enhances a company’s reputation, brand position, and image (Adapa, 2018; Kotler & Lee, 2005). Furthermore, it yields sales increments, re-enforces worker commitment and staff allegiance, upsurge labor efficiency, and offers further pay-offs (Mousiolis et al., 2015). Indisputably, executing CSR programs have demonstrated to lead to improved operational functionality, pecuniary business rewards, and alleviation of business hazards (Dhaliwal et al., 2011). Thus, partaking in CSR programs re-enforces a firm’s ethnic identity, yielding greater stakeholder satisfaction and enhanced financial performance (Okafor et al., 2021). Besides, numerous pieces of research establish a conspicuous notion of CSR on FP (Latif et al., 2020) by endorsing the direct association between CSR and FP (Ling, 2019).

In sum, the literature review largely depicts a direct correlation between CSR and FP. Building on the literature review, this inquiry formulates a testable hypothesis as follows:

H1: CSR has a positive and significant influence on FP.

CSR, BS, and FP

Ceteris paribus, increasing BS should result in a dip in discretional accumulations and enhance the quality of pecuniary reportage in view of BOD’s high inspection and monitoring levels. According to Fama and Jensen (1983), the BOD is the most essential conduit in the interior CG configuration of a company. Agency theory (AT) posit that, the bigger the board, the more attentive and watchful the board will be because a considerable number of veteran and knowledgeable board members will be monitoring and appraising managerial actions and inactions (Kiel & Nicholson, 2003). Again, AT’s viewpoint is that bigger boards assist efficient monitoring by cutting CEO power and safeguard shareowners’ interests (Singh & Harianto, 1989). They contended that bigger boards enhance the negotiating locus of the board vis-à-vis CEO and thus bigger boards are more efficient in monitoring managerial activities. Bigger boards are regarded as having adept board members, specifically those who are non-executive directors and can offer ecological links.

Contrariwise to research undertaken by the investigation of (Ujunwa, 2012) examining the influence of BOD features on Nigerians pecuniary performance, it was revealed that, BS was indirectly associated with FP. Saad (2010) indicated that the pecuniary performance of the company is enhanced with a bigger BS because the firm will have more knowledgeable directors to excellently execute their functional duties. Cheng (2008) opined that bigger BS is indirectly related to FP. Cheng maintained that having a bigger board will generate more bureaucratic delays during the decision-making process. BS is usually used as a signal for the advisory/monitoring role. Practical study findings on ideal BS are mixed. Opponents of bigger BS argue that, bigger BS increases operational expenses and BOD contentions. On the other hand, supporters of bigger BS contend that, small BS are ineffective in monitoring influential corporate heads and CEOs. Coles et al. (2008) also maintained that, BS has a direct correlation with firm size. Accordingly, based on the literature review, this article formulates hypothesis number 2 as follows:

H2: BS moderates and strengthens the relationship between CSR and FP.

CSR, BI, and FP

One school of thought is of the view that for BOD to be efficacious in its monitoring activities, then it should be autonomous. Besides, non-executive members’ inclusion on the BOD is a proficient means of lessoning the potential agency problems of corporate entities. Numerous prior studies’ assessment of BI as a moderator on the association between CSR and FP have yielded varied findings (Chen, 2011; Duru et al., 2016; Moussa, 2019; Karada et al., 2015; Wu & Wu, 2014). These researchers contend that non-executive members’ interest on the BOD has to do with mitigating corporate risk vis-à-vis investment decisions making. Conversely, others are of the opinion that the non-executive directors’ overly involvement in the routine dealings or happenings of the corporate entity may limit top-level authority holders to undertake their operational duties freely. The extant literature thus theorizes the moderating role of BI as follows:

et al., 2015; Wu & Wu, 2014). These researchers contend that non-executive members’ interest on the BOD has to do with mitigating corporate risk vis-à-vis investment decisions making. Conversely, others are of the opinion that the non-executive directors’ overly involvement in the routine dealings or happenings of the corporate entity may limit top-level authority holders to undertake their operational duties freely. The extant literature thus theorizes the moderating role of BI as follows:

H3: BI moderates and strengthens the relationship between CSR and FP.

CSR, BGD, and FP

The utmost extensively deliberated feature of BOD multiplicity and dynamics is gender. The structure of gender on the board is an imperative CG construct, since females and males are traditionally, dissimilar. For example, evidence from prior studies indicates that men and women are dissimilar concerning personality traits, style of communication, level of education, level of knowledge, and work experience. To validate this, contentions elements/factors like the speedy socialization experienced by the feminine gender, and gender’s influence on their behavior as females (Shepard et al., 1997). Some researchers’ document that feminine directors may play an inconsequential role in checking issues in view of gender-based predispositions (Galbreath, 2018). Studies on the impact of gender diversity in developing countries are comparatively scanty because of cynicism about involving female directors on the board of most corporate entities.

In 2009, Johl et al. (2015) analyzed the effect of BOD features and FP of 700 publicly companies operating on the Malaysia Stock Exchange and unveiled that female involvement yielded significantly direct association with ROA. This conforms to the works of Taghizadeh and Saremi (2013) whom in 2008 analyzed 150 publicly listed firms in Malaysia. Analogous findings were revealed by Hou et al. (2015) for companies operating on Singapore’s main bourse. Hou et al. (2015) revealed that female multiplicity upsurges the company’s stock market prices measured via TQ. Nonetheless, Marimuthu and Kolandaisamy (2009) study revealed insignificant association sex multiplicity and FP.

The association between sex multiplicity and myriad FP metrics (ROA, return on equity [ROE], and TQ) in Scandinavia countries is somewhat feeble. Daunfeldt and Rudholm (2012) and Schwizer et al. (2012) unveiled insignificant correlation between sex multiplicity and FP. Nonetheless, Ahern and Dittmar (2012) indicated that market share prices of companies in Norway drop with the inclusion of female BOD members to satisfy the country’s affirmative action drive.

One can, therefore, conclude that female directorship on the BOD yields healthier board crescendos and relatively enhanced FP. AT submits corporate managers would be effectively monitored with a more multifaceted BOD. On the basis of the findings of prior studies in the extant literature, this article formulates the fourth and final hypothesis as follows:

H4: BGD moderates and strengthens the relationship between CSR and FP.

Conceptual Framework (Research Model)

This study’s research model (conceptual framework) is built on the linkages between variables (prognostic, control, moderating, and response) in previous research. Figure 1 present a schematic view of the study’s conceptual framework guiding this empirical investigation, depicting that CSR decision of listed firms in Ghana affect FP via the moderating impact of board structure elements as follows: CSR index influences FP proxies by accounting-based profitability metric, that is, ROA and market value metric represented by TQ via the moderating influence of BS, BI, and BGD. The use of the word “outcomes” in Figure 1 is not referring to outcome variable as in dependent variable. It is only explicating the consequences or end result of the impact of CSR on FP. These outcomes are usually seen/reflected in the various communities of operations referred to as societal outcomes [1. Improve physical environment, 2. Improve social welfare, 3. Community development] or reflected in corporate performance referred to as corporate outcomes [1. Improved earnings, 2. Reduce operational cost, 3. Enhanced firm image 4. Satisfied employees] as shown in Figure 1.

Figure 1. Conceptual Framework (Research Model).

Data and Methodology

Sample and Data

The inquiry’s population comprised all 36 listed companies in Ghana. This form the study’s sampling frame and size. The researcher’s intent was to ascertain whether corporations’ CSR programs contributed value to Ghana’s capital market players. The study utilized pecuniary information pooled from the audited final accounts of listed firms for the period 2010–2020, yielding 396 balanced panel firm-year observations. The financial information was acquired from the facts book of the Ghana Stock Exchange and the websites of the companies via withdrawal technique. All 36-listed firms have in one way or another other engaged in CSR activities in Ghana over the study period. The author hand-gathered primary data on board structure variables (BS, BI, and BGD) via a structured (close-end) questionnaire (Appendix) administered to the top-level management of the listed firms and verified the information with information extracted from the Annual Corporate Governance Reports published by the GSE and information from the published audited final accounts.

Econometric Estimation Technique

This inquiry empirically investigates the impact of CSR on FP with respect to all 36 listed companies in Ghana via the moderating role of BS, BI, and BGD. The inquiry utilized a robust system-GMM estimation technique to specify the linkages between CSR and FP in Ghana as used by prior researchers (Asongu & De Moor, 2017; Asongu et al., 2018; Asongu & Acha-Anyi, 2019). The system-GMM estimator was chosen given its associated advantages and the dependability of related results. The system-GMM estimator uses the added set of level moment conditions in addition to the difference moment conditions for prediction in dynamic panel data. As such, it blends the difference equations and the level equations into one superior system of equations. According to Roodman (2009), this entails formulating a weighted dataset with doubled observations, where the difference equations precede the level equations. Since the differential equations and the level equations assume similar non-exponential specifications, the entire system can be specified by a single procedure that satisfies both systems of equations. The gains from using the Systems-GMM over the other known methodologies are as follows:

Systems-GMM incorporates the dynamism of the phenomena been investigated, that is, given the characteristic changing nature of a firm’s DP from its target in the SR, and the corresponding self-adjustment to its main target, in the long run, the system GMM is best suited for specifying CSR-FP models econometrically (Wooldridge, 2010). It does not discard cross-industry disparities in the specification (Asongu et al., 2018). It allows the error terms to be uncorrelated across individual observations (Gujurati, 2004). It can deal with unobserved heterogeneity with time-invariant indicators (Wooldridge, 2010) and endogeneity problems via an instrumentation process. It can control for heteroscedasticity concerns (Wooldridge, 2010). System-GMM is favored in this current inquiry because it offers the least bias and uppermost accuracy with small time dimension (t) (in this case 9 years) when matched to other econometric estimation techniques like the fixed effect (FE), random effect (RE), level or difference GMM. The present study handled all regressors stringently as exogenous, with the exception of the lagged regressants deployed as instruments in the models. By lagging the reggressants and utilizing them as regressors, it solves any endogeneity, reverse causality issues as well as inconsistencies outcomes resulting from pretermit variables.

Last, of all, four tests were utilized to corroborate the Blundell and Bond (1998) estimator comprising two serial-correlation tests: AR(1) and AR(2) - Arellano and Bond (1991), Sargan and Hansen overidentification restrictions tests (OIR) and contemporaneous correlation test (CD3) for correcting cross-sectional dependence. AR(1) test is performed on the grounds of the null hypothesis of no first order correlation of the idiosyncratic terms and the AR(2) test, is grounded on the null hypothesis of no second order correlation between the stochastic disturbance terms. Sargan and Hansen’s (OIR) tests must be insignificant because their null hypotheses are the positions that instruments are valid or uncorrelated with the white noises. In essence, while the Sargan OIR test is not robust but not weakened by instruments, the Hansen OIR is robust but weakened by instruments. To enforce identification restrictions, the author has ensured that instruments are lower than the number of cross-sections in most specifications (Asongu & De Moor, 2017). The estimated model is valid when the null hypotheses of the AR(1) and AR(2) tests are both accepted. For the Sargan and Hansen (OIR) test, it is expected that the null hypothesis is accepted, resulting in instruments that are uncorrelated with the residual terms.

The deployment of any good dynamic panel GMM estimation technique necessitates the substantiation of its framework with identification, simultaneity, and exclusion restrictions (ER). Identification denotes the selection of the outcome, endogenous variables explaining the strictly exogenous variables. Simultaneity bias, a problem that results when the explanatory variables are correlated with the residuals is solved with lagged explanatory variables deployed as instruments. ER is the procedure by which the strictly exogenous variables solely via the endogenous explaining variables impact the outcome variable. ER concept means that some of the exogenous variables may not be present/observable in the dynamic models and it’s mostly expressed by saying the coefficient next to that exogenous variable is zero, which may make this restriction (hypothesis) testable. As far as ER is concerned, only time-invariant variables are treated as strictly exogenous but all other explanatory variables are treated as suspected endogenous/predetermined variables (Asongu & Acha-Anyi, 2019).

These time-invariant variables influence the outcome variables exclusively via the suspected endogenous/predetermined variables, which is in line with the identification process. Also, the fundamental ER axiom is statistically valid if and only if the null hypothesis relating to the Difference in Hansen Test (DHT) for instrument exogeneity is supported. With respect to the moderating roles of the three selected CG elements, that is, BS, BI and BGD, the study employed moderated multiple linear regression analysis (interactive regression models) for its analyses. A moderator (also referred to as Effect modifiers; Effect-measure modifiers; Interacting factors) is a variable that systematically modifies the form or strength of a relation between an independent variable and a dependent variable (Baron & Kenny, 1986). Inculcating interaction variables in multivariate linear regression models alters the interpretation of the coefficient of the constituent variables, that is, the individual terms within the interaction.

In an interactive regression, the individual variables coefficient depict the effect of the variable only when the other variable equals zero (Burks et al., 2019). It must be noted that, many at times, this specific effect does not denote a central tendency or “main effect,” since the other individual variable assumes a zero value only at an extreme/unfeasible point. Observing a large change in the individual term coefficient after incorporating an interaction term to a previously specified regression model, simply reflect the newly conditional nature of the coefficient but cannot be interpretated as the presence/existence of collinearity between the individual term and the interaction (Burks et al., 2019). This does not invalidate the multivariate linear regression equations (Burks et al., 2019).

This current study employed mean centering technique before introducing the interaction terms as a means of alleviating structural multicollinearity concerns (structural multicollinearity is a mathematical term/variable caused by generating fresh regressors from other regressors, like generating the regressor x2 from the regressor x) and thus creating more stable estimates of regression coefficients. Mean centering also referred to as variable standardization via mean subtractions, encompasses computing the mean for the individual explanatory variables and then deducting the mean from all observed figures of that variable. The resultant centered variables are then used in the regression equations. Notwithstanding the fact that other standardization procedures exist, mean subtraction has the advantage in that, the interpretation of the coefficients does not change. The coefficients continue to represent the mean change in the response variable given a 1 unit change in the prognostic variable.

Empirical Model Specification

This inquiry used two FP metrics, namely, ROA a profitability/accounting measure and TQ, a stock market metric. Notwithstanding the associated advantages of utilizing the accounting measure-ROA, it can be manipulated by the firm’s management. The stock market value metric – TQ on the other hand is difficult to manipulate even though it reflects investors’ subjective assessment instead of the true economic reality of the corporation (Nyeadi et al., 2018). As such, this study utilized both measures as a robustness check, and also, one measure’s strengths might offset the shortcomings of the other. The initial equation sets modelled ROA and TQ for firm “i” at a time “t” on the CSR index and the related control variables without the interaction terms as follows:

[MODEL 1]

[MODEL 1]

[MODEL 2]

[MODEL 2]

The final equation sets modelled ROA and TQ for firm “I” at a time “t” on the CSR index and the related control variables with the introduction/addition of the interaction terms as follows:

[MODEL 3]

[MODEL 3]

[MODEL 4]

[MODEL 4]

Moderation effect is present in these models if, the coefficients of the interaction between the main predictor (CSR) and the moderator variables (BS, BI, BGD) are statistically significant. Put differently if CSR * BS; CSR * BI and CSR * BGD are found to be statistically significant, then a moderation effect is present and the strength of the relationship between the prognostic variable (CSR) and the criterion variable (FP) is changed (Mansour et al., 2022). Explicitly, when (BS, BI, BGD) strengthens (weaken) the effect of the CSR, the interaction term will have the same sign (opposite sign) as the CSR variable (Mansour et al., 2022). Put differently, if the moderation ends in strengthening the relationship between the independent variable and the dependent variable then both the independent variable and the interaction term will generate the same sign. On the other hand, if the modification ends in weakening the relationship between the independent variable and the dependent variable then both the independent variable and the interaction term will generate the opposite signs. In this study, CG metrics of BS, BI, and BGD were treated strictly as pure moderators and not quasi-moderators as they interact with the CSR index but have no direct relational impact on FP (ROA and TQ). Put differently, pure moderators are variables that must necessarily interact with the independent variable to modify the form or strength of the relationship between the dependent and independent variable but does not influence the dependent variable directly. Psychometrically speaking, pure moderators must enter into an interaction with the independent variable while having a negligible correlation with the dependent variable itself (Akhmadi & Januarsi, 2021; Otero-González et al., 2021; Sharma, 2003). A quasi-moderator on the other hand is a variable that interact with the independent variable to modify the form or strength of the relationship between the dependent and independent variable and in addition acts as a predictor itself in influencing the dependent variable. The variables were selected on the basis of data availability and peculiarity of the happenings in the Ghanaian capital market vis-à-vis CSR-FP nexuses. The measurements of the study’s variables, their definitions, and empirical source literature are presented in Table 1.

Table 1. Measurement of Variables.

![]()

Note: NB: Variables were winsorized at the 5th & 95th percentiles so as to minimize the effect of possible extreme values acting as outliers, except for the firm-specific effects and time fixed effects dummy variables.

Results and Discussion

Regression Assumptions Testing

The authors ensured that the standardized multivariate linear regression models satisfy all the assumptions [Normality, heteroskedasticity, autocorrelation, endogeneity and heterogeneity] necessary under multiple linear regression analysis to avoid a situation where an assumption would be violated which will result in biased/spurious outcomes.

The assumption testing guarantee that the models are fit for regression. The regression assumption testing results are presented in Table 2.

Table 2. Testing Regression Assumptions Summary.

Descriptive Statistics

Table 3 presents the summary descriptive statistics of the response, prognostic, moderating, and control variables. As mentioned earlier, this study utilizes 36 cross-sectional units for an 11-year time period, generating 396 firm-year balanced observations.

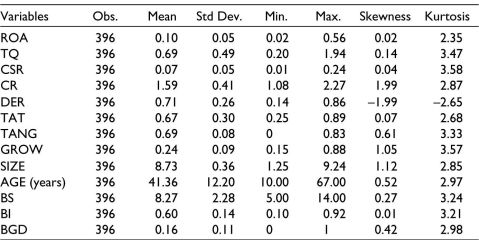

Table 3. Descriptive Summary Statistics of Dependent and Independent Variables.

The 36 listed companies recorded an average profitability-ROA of 0.10, meaning that for each cedi in assets, the firms generated 10 pesewas in profits. The mean TQ for the firms was 0.69, suggesting that majority of the companies operating on the GSE on average made losses; as their current market values exceeded their replacement costs.

The study recorded a CSR value of 0.07, implying that, listed firms on average channeled 7% of their net profit after interest and tax into CSR projects. The company’s mean CR was 1.59, suggesting a quite satisfactory liquidity position stemming from fairly good working capital management practices.

Concerning gearing, listed companies employed more debt financing than equity financing as they recorded an average DER of 71%. This conjecturally signals the under-developed status of Ghana’s bourse as a source of raising equity finance. An average of 67% and 69% were recorded for TAT and TANG, respectively, signifying that, the listed firm’s total assets generated 67% of their sales, while 69% of their total assets were injected into fixed assets. The average sales growth rate of the listed firms was 24%, and an 8.73 average SIZE was recorded for the listed companies. The study recorded a mean age of 41 years, with the youngest firm being ten years, and the oldest firm, having been in operations for 67 years in Ghana. There were 8 board members on average with a maximum BS of 14 and a minimum size of 5. On average, 60% of the board members were non-executive (outside) directors which are good for CG purposes and 16% of board members were females which is rather on the low side.

Correlation Analysis

The study prepared a correlation matrix to ascertain whether multicollinearity was an issue in the sampled dataset. In addition, the correlation matrix was performed to ascertain the associations between the response variables and the predictor, moderating, interaction terms and control variables as well as explore the associations among all the independent variables. Furthermore, all the predictors recorded the highest VIF of 1.25, 1.30, 1.11, 1.32, 1.13, 1.12, 1.34, 1.56, 1.64, 1.44, and 1.50, respectively, for the explanatory variables. These VIFs fall below the criteria of 10, suggesting the absence of multicollinearity (Kennedy, 1998). The VIF values are presented in Table 4. This was performed to circumvent a scenario where two or more highly correlated variables would be included in a regression model. Table 4 presents the correlation analysis with ROA and TQ as the dependent variables against the other independent, moderating and control variables.

Table 4. Pearson Correlation Matrix and Multicollinearity Test of Study Variables.

Notes: ***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

VIFs denote variance inflation factors for explanatory variables.

Variables were winsorized at the 5th & 95th percentiles so as to minimize the effect of possible extreme values acting as outliers.

The correlation test performed revealed that the correlation between the variables included in the regression all fell below Hair et al. (2016) recommended criterion of 0.6, and as such, the absence of multicollinearity. DER depicted a negative and significant association with ROA and TQ, signifying that, highly leveraged companies performed appallingly. This can be attributed to the high-interest rate on loanable funds in the Ghanaian financial market. All the other independent variables depicted significantly positive associations with ROA and TQ.

Empirical Baseline Regression Results and Discussion

As indicated earlier, the objective of this scientific inquiry is to empirically investigate the effect of CSR of the performance of listed firms in Ghana, via the moderating influence of BS, BI and BGD. The study utilized two measures of FP-(ROA and TQ) as a means of avoiding potential variable mismatch issues in addition to ensuring a robustness check of the study findings. The study foremost examined the individual effect of CSR on the performance of listed firms in Ghana directly without the moderation effect. The study then assessed the effect of CSR on FP with the interaction/moderation influence. Table 5 presents the baseline regression results performed via a robust two-step system-GMM in two separate fashions. The results without moderation interactions and the results with moderated interactions.

Model 1 presents the result without moderated interactions using ROA as the criterion variable.

Model 2 presents the result without moderated interactions using TQ as the response variable.

Model 3 presents the result with moderated interactions using ROA as the dependent variable.

Model 4 presents the result with moderated interactions using TQ as the criterion variable.

All the four-test performed to corroborate the Blundell and Bond (1998) system-GMM estimator were demonstrated to be statistically valid as Sargan and Hansen test confirmed the absence of overidentification issues, AR(1) and AR(2) passed the test for no-first and second-order serial-correlation in errors and the CD3 test showed no issue of contemporaneous/cross-sectional dependence in the study results. The adjusted R2 values for all four models as presented in Table 5 is reasonable, depicting that the independent variables explained substantial proportions of the variances in the dependent variables. The F-statistics values for all 4 models are also reasonable depicting satisfactory overall performance and model fit. Therefore, Table 5 results demonstrate statistical validity for all four models.

Table 5. System GMM Regression Results for the Relationship Between CSR and FP (ROA and TQ), Without Moderation Interaction.

Notes: The robust standard errors (SEs) are reported in parentheses.

Each model estimation incorporated both time and industry dummies, but the estimates are not reported.

***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

The use of the word centering indicates that mean centering were applied before introducing the interaction terms in the regressions models as a means of alleviating structural multicollinearity issues.

With respect to the non-moderated regression results, Models 1 and 2 show that CSR had a positive and significant (at 5%) influence on FP. This implies that firms that invested more in CSR activities improved their financial performance in terms of ROA and TQ. Consequently, the benefits of investing in CSR programs are that they yield a positive comeback of the markets, surge earnings, and strengthen the solidness of entire financial growth/development. This is consistent with the theoretical proposition of the stakeholder theory that, when all of a firm’s stakeholder requirements are equally addressed, the firm’s core economic responsibility, that is, shareholder wealth maximization via returns-generation (both dividends and capital gains) for stockholders is also met, resulting in improved firm image and reputation and hence enhanced FP (Nyeadi et al., 2018). These findings support hypothesis 1 [H1] and it conforms with the findings of authors such as Nyeadi et al. (2018), Feng et al. (2018), Javeed and Leven (2019), Waheed et al. (2021). This result, however, is at Caretta with the theoretical prediction of the agency cost theory which contends that firms that inject funds into CSR projects distract the firms’ fundamental mandate of creating wealth for the providers of equity capital to the business thereby impacting FP adversely. Concerning the control variables, except for DER which recorded a negative impact on FP-(ROA and TQ), all the other six control variables exhibited positive influences on FP-(ROA and TQ).

DER exhibiting a negative association with FP-(ROA and TQ), shows that companies that are highly geared performed poorly concerning ROA and TQ which could conjecturally be attributed to the high cost of debt financing emanating from high-interest rates on loanable funds on the Ghanaian financial market which invariable impacted unfavorably on FP-(ROA and TQ). This result is in line with Kim et al. (2014), Yang and Baasandorj (2017), and Nyeadi et al. (2018).

CR relates positively with ROA and TQ, suggesting that profitable listed firms embarked on prudent liquidity management via sound working capital management, which culminated in improved FP-(ROA and TQ). This result is in line with the findings of Agyei, Sun, and Abrokwah (2020).

TAT also associates positively with FP-(ROA and TQ), implying that listed firms with high sales generation via total assets utilization achieved high FP(-ROA and TQ). This result conforms with the findings of Agyei et al. (2020).

TANG also correlates positively with FP-(ROA and TQ), meaning, listed firms with high investment in fixed assets experienced an improvement in FP-(ROA and TQ). This finding is in line with the findings of Agyei et al. (2020).

GROW relates directly with FP-(ROA and TQ), signifying that, high sales growth levels resulted in improved FP-(ROA and TQ). This result is in line with the findings of Agyei et al. (2020).

Similarly, SIZE associates positively with FP-(ROA and TQ), depicting that larger firms performed comparably better than their smaller counterparts, as larger institutions optimize their economies of scale in addition to the fact that they are better placed to access funding opportunities from the investment world both debt and equity, while smaller firms do not have such advantages. Thus, larger firms are in a position to inject huge resources into CSR projects and reap their corresponding benefits consistent with the stakeholder theory. This result tally with the findings of Agyei et al. (2020) but is at loggerhead with Nyeadi et al. (2018) and Waheed et al. (2021).

Likewise, AGE correlates positively with FP-(ROA and TQ), suggesting that aged firms performed comparatively better than their younger counterparts as long-lived institutions have developed better operational and managerial competencies through direct/indirect on-the-job experience resulting in improved FP-(ROA and TQ). These findings are consistent with the findings of Agyei et al. (2020) but contrary to Kim et al. (2014), Yang and Baasandorj (2017), Nyeadi et al. (2018), Waheed et al. (2021).

Concerning the moderated interaction linear multiplicative regression effect, all three CG elements of BS, BI, and BGD moderated the association between the CSR index and FP-(ROA and TQ) (evident in the significant results generated from the CSR*BS, CSR*BI, and CSR*BGD interaction presented in Table 6 and Table 7). With regards to Model 3 for ROA, the results of the moderated interaction linear multiplicative regression analysis depict that the coefficient of the interaction terms between [CSR and BS (CSR × BS)]; [CSR and BI (CSR × BI)]; and [CSR and BGD (CSR × BGD)] were 0.2198; 0.2205 and 0.2030, respectively positive and significant at 5% level, supporting H2 H3 H4, respectively for ROA. This is also the case for Model 4 for TQ as can be seen in Table 7. The results of the moderated interaction regression analysis suggest that, as firms practice good CG (arising from the influential activities of the number of members on the board, independency on the board and BGD) reflected in better monitoring and control of managerial behavior, coupled with greater alignment with all stakeholders’ interests, translated into higher firm ability to access funds from financial institutions, improving the cash inflow generating pattern of listed firms, which translated into firms ability to engage in well thought through CSR programs that eventually improved FP.

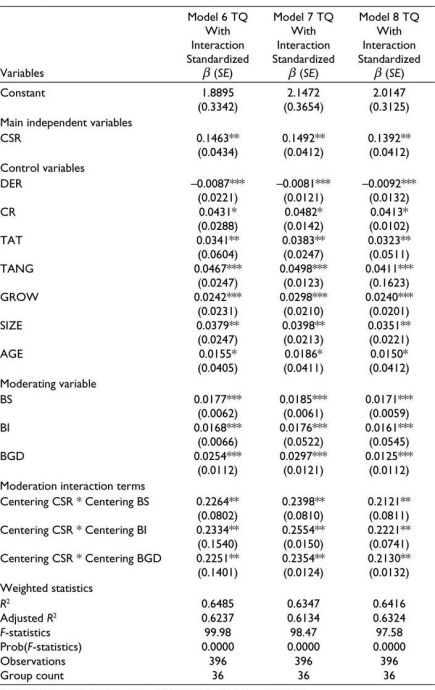

Table 6. System GMM Regression Results for the Relationship Between CSR and ROA as Dependent Variable, with Moderation Interaction.

Notes: The robust standard errors (SEs) are reported in parentheses.

Each model estimation incorporated both time and industry dummies, but the estimates are not reported.

***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

The use of the word centering indicates that mean centering were applied before introducing the interaction terms in the regressions models as a means of alleviating structural multicollinearity issues.

Table 7. System GMM Regression Results for the Relationship Between CSR and TQ as Dependent Variable, with Moderation Interaction.

Notes: The robust standard errors (SEs) are reported in parentheses.

Each model estimation incorporated both time and industry dummies, but the estimates are not reported.

***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

The use of the word centering indicates that mean centering were applied before introducing the interaction terms in the regressions models as a means of alleviating structural multicollinearity issues.

This study’s theoretical proposition formulated in the hypotheses has been confirmed by the significance of the interactions in the study’s results presented in Table 6 and Table 7. Furthermore, the complementary relationships between the three CG metrics of BS, BI and BGD and CSR has been corroborated via the synergistic impact of the moderated interaction. The confirmation is verified in the statistically significant and positive association between the moderated interaction terms and the performance metrics of ROA and TQ of listed firms in Ghana. The implication of the study results is that the interaction term has a significant marginal effect on FP so far as listed firms on the GSE are concerned. The results from the study’s findings can also be interpreted that, with the inculcation of the moderators (BS, BI and BGD) into the regression models, the moderators positively influenced (positively interaction) the association between the main/only prognostic variable (CSR) and the criterion variables (ROA and TQ), which had been tremendously enhanced.

This study’s findings are in line with the stakeholder theory which opines that, when all of a firm’s stakeholder requirements are equally addressed, the firm’s core economic responsibility, that is, shareholder wealth maximization via returns-generation (both dividends and capital gains) for stockholders is also met, resulting in improved firm image and reputation and hence enhanced FP (Nyeadi et al., 2018).

Robustness Checks

This study investigated the impact of CSR on the performance of listed firms in Ghana, via the moderating role of BS, BI and BGD. A robust dynamic panel two-step system GMM was espoused for the empirical estimation. In order to check the robustness of the study findings, the results were subjected to some robustness tests via using an alternative econometric estimation technique this time a static econometric estimation technique, that is, FE. The FE was used after performing all necessary and prerequisite tests, that is, Hausman specification test (HST) to determine the appropriateness of the FE as against the RE. In addition, an alternative measure of accounting profitability, that is, ROE was employed to test the study’s robustness. The results of this exercise are presented in Table 8 and Table 9. The findings in Table 5 is consistent (in terms of analogous expected theoretical signs and significance at all conventional levels) with those reported in Table 6 and as such the study is deemed to have the required reliability, validity, and robustness. The results from the alternative accounting profitability measure, that is, ROE are also similar to that of the ROA results, further supporting the robustness of the study.

Table 8. Robustness Checks: Fixed Effect Regression Results of CSR and Other Explanatory Variables Effect on ROE as the Dependent Variable.

Notes: The robust standard errors (SEs) are reported in parentheses.

***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

Table 9. Robustness Checks: Fixed Effect Regression Results of CSR and Other Explanatory Variables Effect on TQ as the Dependent Variable

Notes: The robust standard errors (SEs) are reported in parentheses.

***, ** and * denote significance at the 1%, 5%, and 10% levels, respectively.

Conclusion and Limitations

This research examined the moderating role of BS, BI and BGD on the association between CSR and FP-(ROA and TQ). Espousing a robust system-GMM, which controlled for unobserved heterogeneity, heteroscedasticity, simultaneity, reverse causality, endogeneity, overidentification issues, first and second-order serial-correlation in errors and contemporaneous/cross-sectional dependence, the study concluded that, all the predictors had a statistically significant impact on FP. Except for DER which recorded an indirect relationship with FP, all the other predictors exhibited direct relationships with FP. Furthermore, BS, BI, and BGD moderated the relationship between CSR and FP. This inquiry corroborates the stakeholder theory in the Ghanaian context in explicating the CSR-FP nexus. This inquiry’s findings are generally consistent with similar research results in the extant literature.

There are several policy, managerial and scholarly implications of this study that is highly imperative for corporate financial managers and impending research for the improvement of CSR activities. The study recommends businesses to improve their profitability levels via engaging in diversified capital budgeting projects that yields positive net present values to ensure firm’s self-sustainability as this is the first stage that guarantee that businesses would be in a position to give back to society via CSR programmes. To ensure improved FP via enhanced profitability, corporate financial managers should utilize more retained earnings as internal financing source to minimize the high-interest cost on debt financing. In addition, the study recommends policymakers and GSE’s authorities to revamp Ghana’s capital market to encourage equity investment in other to enable businesses access long-term capital necessary for their business operations.

This study’s implication is to aid institutional managers make decisive financial decisions on CSR (i.e., invest in CSR projects and not to ignore CSR activities) so as to optimize the benefits associated with equally meeting all stakeholder needs in other to improve overall corporate image and reputation with the replica effects reflected in enhanced FP.

In so doing, business owners must examine their board mechanisms and ensure that the board is well-structured in terms of its composition (enforcement of a fair representation on the board in terms of outside/non-executive directors), size and gender diversity (noting that, evidence from this present study has revealed that large BS and the presence of female directors on the board did affect CSR decision-making to further influence FP). Familiarity with this may have crucial consequences for firms’ CSR dispersion.

Furthermore, businesses should ascertain the societal issues prevalent where they operate and formulate excellent solutions to address these problems.

This study is not without limitations. This current inquiry was wholly based on companies operating on the GSE, abandoning companies not listed on the GSE. The econometric estimation equations excluded some macroeconomic control variables like taxation, gross domestic product, inflation, exchange rate, interest rate. Consequent studies should consider the incorporation of these macroeconomic metrics and the activities of other companies not listed on the GSE to have a larger view of the impact of CSR on FP in Ghana.

Code Availability Statement

The authors declare that STATA codes for running the estimations for this article will be available upon request.

Data Availability Statement

The authors declare that there is perfect data transparency and data will always be available at any time upon request.

Declaration of Conflicting Interests

I hereby confirm that there is no actual or potential conflict of interest including any financial, personal, or other relationships with other people or organizations within three years of beginning the submitted work that could inappropriately influence, or be perceived to influence, the work.

Ethical Approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

ORCID iD

Ronald Ebenezer Essel https://orcid.org/0000-0002-2735-1252

Adapa, S. (2018). Indian smart cities and cleaner production initiatives-integrated framework and recommendations. Journal of Cleaner Production, 172, 3351–3366.

Agyei, J., Sun, S., & Abrokwah, E. (2020). Trade-off theory versus pecking order theory: Ghanaian evidence. Sage Open, 1–13. https://doi.org/10.1177/2158244020940987

Ahern, K. R., & Dittmar, A. K. (2012). The changing of the boards: The impact on firm valuation of mandated female board representation. The Quarterly Journal of Economics, 127(1), 137–197.

Akhmadi, A., & Januarsi, Y. (2021). Profitability and firm value: Does dividend policy matter for Indonesian sustainable and responsible investment (SRI)-KEHATI listed firms? Economies, 9(4), 163.

Amo-Mensah, M. (2021). Corporate social responsibility in contemporary Ghana: A literature review. International Journal of Business and Management Review, 9(5), 78–93.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

Asongu, S. A., & Acha-Anyi, P. N. (2019). The murder epidemic: A global comparative the study. International Criminal Justice Review, 29(2), 105–120.

Asongu, S. A., & De Moor, L. (2017). Financial globalization dynamic thresholds for financial development: evidence from Africa. The European Journal of Development Research, 29(1), 192–212.

Asongu, S. A., & Nwachukwu, J. C. (2018). Openness, ICT and entrepreneurship in Sub-Saharan Africa. Information Technology People, 31(1), 278–303. https://doi.org/10.1108/ITP-02-2017-0033

Babajee, R. B., Seetanah, B., Nunkoo, R., & Ramdhany, N. G. (2022). Corporate social responsibility and hotel financial performance. Journal of Hospitality Marketing and Management, 31(2), 226–246. https://doi.org/10.1080/19368623.2021.1937433

Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51, 1173.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87, 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

Burks, J. J., Randolph, D. W., & Seida, J. A. (2019). Modeling and interpreting regressions with interactions. Journal of Accounting Literature, 42, 61–79. https://doi.org/10.1016/j.acclit.2018.08.001

Carroll, A. (1979). A three-dimensional conceptual model of corporate performance. Academy of Management Review, 4(4), 497–505.

Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48. https://doi.org/10.1016/0007-6813(91)90005-g

Chen, H. L. (2011). Does board independence influence the top management team? Evidence from strategic decisions toward internationalization. Corporate Governance: An International Review, 19(4), 334–350.

Cheng, S. (2008). Board size and the variability of corporate performance. Journal of Financial Economics, 87(1), 157–176. https://doi.org/10.1016/j.jfineco.2006.10.006

Coles, J. L., Daniel, N. D., & Naveen, L. (2008). Boards: Does one size fit all? Journal of Financial Economics, 87(2), 329–356.

Cornell, B., & Shapiro, A. C. (1987). Corporate stakeholders and corporate finance. Financial Management, 16(1), 5–14.

Crane, A., & Matten, D. (2016). Business ethics: Managing corporate citizenship and sustainability in the age of globalization (p. 87). Oxford University Press.

Daunfeldt, S. O., & Rudholm, N. (2012). Does gender diversity in the boardroom improve firm performance. Departamento de Economía de la Universidad de Dalarna, 781, 88.

Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Accounting Review, 86, 59–100.

Duru, A., Iyengar, R. J., & Zampelli, E. M. (2016). The dynamic relationship between CEO duality and firm performance: The moderating role of board independence. Journal of Business Research, 69, 4269–4277.

Essel, R., & Addo, E. (2021). SMEs corporate governance mechanisms and business performance: Evidence of an emerging economy. Journal of Governance and Integrity, 5(1), 155–169.

Essel, R., & Brobbey, J. (2021). The impact of working capital management on the performance of listed firms: Evidence of an emerging economy. International Journal of Industrial Management, 12(1), 389–407.

European Commission. (2001). Green paper promoting a European framework for corporate social responsibility.

Fama, E., & Jensen, M. (1983). Agency problems and residual claims. Journal of Law and Economics, 26(2), 327–349.

Feng, Y., Chen, H. H., & Tang, J. (2018). The impacts of social responsibility and ownership structure on sustainable financial development of China’s energy industry. Sustainability, 10(2), 301.

Galbreath, J. (2018). Is board gender diversity linked to financial performance? The mediating mechanism of CSR. Business and Society, 57(5), 863–889. https://doi.org/10.1177/0007650316647967

Grassmann, M. (2021). The relationship between corporate social responsibility expenditures and firm value: The moderating role of integrated reporting. Journal of Cleaner Production, 285, 124840.

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2016). Multivariate data analysis. Prentice Hall.

Hirigoyen, G., & Poulain-Rehm, T. (2017). An international comparative approach to corporate governance: An empirical study. In Colloque Gouvernance, Marrakech.

Ho, L. C. J., & Taylor, M. E. (2007). An empirical analysis of triple bottomline reporting and its determinants: Evidence from the United States and Japan. Journal of International Financial Management and Accounting, 18(2), 123–150.

Hou, K., Xue, C., & Zhang, L. (2015). Digesting anomalies: An investment approach. The Review of Financial Studies, 28(3), 650–705.

Javeed, S. A., & Lefen, L. (2019). An analysis of corporate social responsibility and firm performance with moderating effects of CEO power and ownership structure: A case study of the manufacturing sector of Pakistan. Sustainability, 11(1), 248.

Johl, S. K., Kaur, S., & Cooper, B. J. (2015). Board characteristics and firm performance: Evidence from Malaysian public listed firms. Journal of Economics, Business and Management, 3(2), 239–243.

Karada?, E., Tosunta?, ?. B., Erzen, E., Duru, P., Bostan, N., ?ahin, B. M., Çulha, ?., & Babada?, B. (2015). Determinants of phubbing, which is the sum of many virtual addictions: A structural equation model. Journal of Behavioral Addictions, 4(2), 60–74.

Kennedy, P. (1998), A guide to econometrics (4th ed.). The MIT Press.

Khan, T. M., Gang, B., Fareed, Z., & Yasmeen, R. (2020). The impact of CEO tenure on corporate social and environmental performance: An emerging country’s analysis. Environmental Science and Pollution Research, 27(16), 19314–19326.

Kiel, G. C., & Nicholson, G. J. (2003). Board composition and corporate performance: How the Australian experience informs contrasting theories of corporate governance. Corporate Governance: An International Review, 11(3), 189–205. https://doi.org/10.1111/corg.2003.11

Kim, Y., Li, H., & Li, S. (2014). Corporate social responsibility and stock price crash risk. Journal of Banking and Finance, 43, 1–13.

Kotler, P., & Lee, N. (2005). Corporate social responsibility: Doing the most good for your company and your cause. John Wiley and Sons, Inc.

Latif, K. F., Sajjad, A., Bashir, R., Shaukat, M. B., Khan, M. B., & Sahibzada, U. F. (2020). Revisiting the relationship between corporate social responsibility and organizational performance: The mediating role of team outcomes. Corporate Social Responsibility and Environmental Management, 27(4), 1630–1641. https://doi.org/10.1002/csr.1911

Ling, Y.-H. (2019). Influence of corporate social responsibility on organizational performance: Knowledge management as moderator. VINE Journal of Information and Knowledge Management Systems, 49(3), 327–352. https://doi.org/10.1108/VJIKMS-11-2018-0096

Lu, J., Ren, L., Zhang, C., Rong, D., Ahmed, R. R., & Streimikis, J. (2020). Modified Carroll’s pyramid of corporate social responsibility to enhance organizational performance of SMEs industry. Journal of Cleaner Production, 271, 122456. https://doi.org/10.1016/j.jclepro.2020.122456

Manchiraju, H., & Rajgopal, S. (2017). Does corporate social responsibility (CSR) create shareholder value? Evidence from the Indian companies act 2013. Journal of Accounting Research, 55(5), 1257–1300.

Mansour, M., Al Amosh, H., Alodat, A. Y., Khatib, S. F., & Saleh, M. W. (2022). The relationship between corporate governance quality and firm performance: The moderating role of capital structure. Sustainability, 14(17), 10525. https://doi.org/10.3390/su141710525

Marimuthu, M., & Kolandaisamy, I. (2009). Ethnic and gender diversity in boards of directors and their relevance to financial performance of Malaysian companies. Journal of Sustainable Development, 2(3), 139–148.

McWilliams, A., & Siegel, D. (2000). Corporate social responsibility and financial performance: Correlation or misspecification? Strategic Management Journal, 21(5), 603–609. https://doi.org/10.1002/(SICI)1097-0266(200005)21:5<603::AID-SMJ101>3.0.CO;2-3

Moussa, F. B. (2019). The influence of internal corporate governance on bank credit risk: An empirical analysis for Tunisia. Global Business Review, 20(3), 640–667.

Mousiolis, D. T., Zaridis, A. D., Karamanis, K., & Rontogianni, A. (2015). Corporate social responsibility in SMEs and MNEs. The different strategic decision making. Procedia-Social and Behavioral Sciences, 175, 579–583.

Nyeadi, J. D., Ibrahim, M. I., & Sare, Y. A. (2018). Corporate social responsibility and financial performance nexus Empirical evidence from South African listed firms. Journal of Global Responsibility, 9(3), 301–328. https://doi.org/10.1108/JGR-01-2018-0004

Oduro, S., & Haylemariam, L. G. (2019). Market orientation, CSR and financial and marketing performance in manufacturing firms in Ghana and Ethiopia. Sustainability Accounting, Management and Policy Journal, 10(3), 398–426.

Okafor, A., Adusei, M., & Adeleye, B. N. (2021) Corporate social responsibility and financial performance: Evidence from US tech firms. Journal of Cleaner Production, 292, 126078.

Otero-González, L., Durán-Santomil, P., Lado-Sestayo, R., & Vivel-Búa, M. (2021). Active management, value investing and pension fund performance. European Journal of Management and Business Economics, 30, 299–317.

Ratnasari, S. L., Rahmawati, R., Ramadania, R., Darma, D. C., & Sutjahjo, G. (2021). Ethical work climate in motivation and moral awareness perspective: The dilemma bythe Covid-19 crisis? Journal of Public Policy and Administration, 20(4), 398–409. https://doi.org/10.13165/VPA-21-20-4-04

Roodman, D. (2009). How to xtabond2: An introduction to difference and system GMM in Stata. Stata Journal, 9(1), 86–136.

Saad, N. M. (2010). Corporate governance and the effects to capital structure in Malaysia. International Journal of Economics and Finance, 2(1), 105–114. https://doi.org/10.5539/ijef.v2n1p105

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. Journal of Business Research, 68(2), 341–350.

Saleh, M. W. A., Zaid, M. A. A., Shurafa, R., Maigoshi, Z. S., Mansour, M., & Zaid, A. (2020). Does board gender enhance Palestinian firm performance? The moderating role of corporate social responsibility. Corporate Governance. https://doi.org/10.1108/CG-08-2020-0325

Santos, M. (2011). CSR in SMEs: Strategies, practices, motivations and obstacles. Social Responsibility Journal, 7(3), 490–495.

Schwizer, P., Soana, M., & Cucinelli, D. (2012). The relationship between board diversity and firm performance: The Italian evidence [Working Paper]. Department of Banking and Insurance, Faculty of Economics, University of Parma.

Sharma, N. (2003). The role of pure and quasi-moderators in services: An empirical investigation of ongoing customer–service-provider relationships. Journal of Retailing and Consumer services, 10(4), 253–262.

Sheehy, B. (2015). Defining CSR: Problems and solutions. Journal of Business Ethics, 131(2015), 625–648.

Shepard, J. M., Betz, M., & O’Connell, L. (1997). The proactive corporation: Its nature and causes. Journal of Business Ethics, 16(10), 1001–1010.

Sial, M. S., Zheng, C., Cherian, J., Gulzar, M. A., Thu, P. A., Khan, T., & Vinh, K. N. (2018). Does corporate social responsibility mediate the relation between boardroom gender diversity and firm performance of Chinese listed companies? Sustainability, 10(10), 35–91.

Singh, H., & Harianto, F. (1989). Management-board relationships, takeover risk, and the adoption of golden parachutes. Academy of Management Journal, 32(1), 7–24.

Singh, K., & Misra, M. (2021). The evolving path of CSR: Toward business and society relationship. Journal of Economic and Administrative Sciences¸38(2), 304–332.

Sprinkle, G. B., & Maines, L. A. (2010). The benefits and costs of corporate social responsibility. Business Horizons, 53(5), 445–453.

Taghizadeh, M., & Saremi, S. (2013). Board of directors and firms performance: Evidence from Malaysian public listed firm. International Proceedings of Economics Development and Research, 59, 178.

Tencati, A., Perrini, F., & Pogutz, S. (2004). New tools to foster corporate socially responsible behavior. Journal of Business Ethics, 53(1), 173–190.

Ujunwa, A. (2012). Board characteristics and the financial performance of Nigerian quoted firms. Corporate Governance, 12(5), 656–674. https://doi.org/10.1108/14720701211275587

Visser, W. (2016). The future of CSR: Towards transformative CSR, or CSR 2.0. In Research handbook on corporate social responsibility in context (pp. 339–367). Edward Elgar Publishing.

Waheed, A., Hussain, S., Hanif, H., Mahmood, H., & Malik, Q.A. (2021). Corporate social responsibility and firm performance: The moderation of investment horizon and corporate governance, Cogent Business and Management, 8(1), 1938349. https://doi.org/10.1080/23311975.2021.1938349

Wang, H., Choi, J., & Li, J. (2008). Too little or too much? Untangling the relationship between corporate philanthropy and firm financial performance. Organization Science, 19(1), 143–159.

Wayne, V. (2010). The age of responsibility: CSR 2.0 and the new DNA of business (p. 231). Emerald Group Publishing Limited.

Weber, M. (2008). The business case for corporate social responsibility: A company-level measurement approach for CSR. European Management Journal, 26(4), 247–261.

Windsor, D. (2001). Corporate social responsibility: A theory of the firm perspective: some comments. Academy of Management Review, 26(4), 502–504.

Wooldridge, J. M. (2010). Econometric analysis of cross-section and panel data. MIT Press.

Wu, J., & Wu, Z. (2014). Integrated risk management and product innovation in China: The moderating role of board of directors. Technovation, 34(8), 466–476.

Yang, A. S., & Baasandorj, S. (2017). Exploring CSR and financial performance of full-service and low-cost air carriers. Finance Research Letters, 23, 291–299.

Yong, H., Muddassar, S., Rimsha, K., Ilknur, O., & Jasim, T. (2022). Does corporate social responsibility and green product innovation boost organizational performance? A moderated mediation model of competitive advantage and green trust. Economic Research-Ekonomska Istraživanja, 35(1), 5379–5399. https://doi.org/10.1080/1331677X.2022.2026243