IIMS Journal of Management Science

Search

Search

1Westminster International University, Tashkent, Uzbekistan

2School of Management, Presidency University, Bengaluru, Karnataka, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Several studies have been conducted to establish the relationships of different factors associated with the e-wallet usage in the recent times. But the effect of COVID-19 pandemic has impacted the e-wallet usage in transformed perspectives. In the crisis period, the acceptance of technology by the customers has definitely brought in the various dimensions to the business stakeholders to leverage on the benefits. It is very much evident for organizations to rework on their strategic viewpoints based on the trends and changes. The pandemic has brought in diverse experiences for the customers as well as businesses. The purpose of this research article leads to ascertaining the frugal consumers by analyzing their buying behavior and to further test the conceptual model of the impact of e-wallets on their buying behavior. This study uses the technology acceptance model (TAM) involving variables such as “Perceived Usefulness,” “Perceived Ease of Use,” “Perceived Risk,” “Trust,” “Social Influence,” “Promotional Benefits,” “Attitude,” “Behavior Intention to Buy Using E-wallets,” and the “Actual Usage of E-wallets.” Findings of this study portray the frugality of the consumers by the nature of their buying behavior, and they also show a strong relation between the frugal consumers and the positive or negative influence of e-wallets on their buying behavior. The results of the study can be applied by concerned organizations to improve their business model with respect to the variables mentioned.

Perceived usefulness, frugality, ease of use, usage rate, promotional benefits, behavioral intention

Introduction

In the age of information, digitization has played a major role accompanied with the increasing use of Internet and increase growth in the use of digital payment. Consumers are of different mindsets and personalities (Dehkordi et al., 2012). Digital payment mechanism is the essence of an electronic wallet by which a payment is done by a customer either via plastic cards or uploaded cash from a bank account to a wallet account, thus enabling the transfer of funds to others with digitization. This has increased the use of smartphones consumers who can now access wallets easily via smartphones. Smartphones do the function of a leather wallet called a “digital wallet”, “electronic wallet,” or a “mobile wallet”. It is a prepaid mode of transaction using the mobile phone application where the cash is, first, deposited just like placing inside a wallet and then transactions are made conveniently and more efficiently when compared to the conventional mode of payment (Kumar, 2016). E-wallets thus play an important role in luring the consumers into buying with attractive discounts and offers of cashback. The study is focused on the frugal consumers and the influence of e-wallets on their buying pattern. Furthermore, there is inadequate research available on a comparative study probing as how e-wallets influence the buying pattern of frugal consumers during the pre-COVID and COVID times.

Statement of the Problem

The study focuses on understanding the frugality of a consumer during pandemic/crisis and analyze if there is a change in the frugal behavior of the consumer from that of pre-pandemic state, and this makes it unique. The different aspects that influence the consumer to adopt e-wallets during the pandemic are also studied in detail, and a corresponding analysis is done.

Research Objectives

Literature Review

Significant investments were done.by telecom companies to boost the connectivity by making it easily accessible by providing vouchers of prepaid recharges, low tariff rates, and different handsets which are affordable (Madan & Yadav, 2016). “Mobile ecosystem” has changed the life of people with reference to social and financial status in the development of countries. The geography in which previous studies have been conducted provides a research gap. Also, there are studies conducted for the intention of use of e-wallets either before the pandemic or during the pandemic.

Frugality is viewed from different aspects covering the religious, cultural, psychological, and economic perspectives. The consequences confirmed that frugal customers are less materialistic, much less fame aware, and much less concerned with manufacturers than different purchasers, but are independent from the evaluations of others in their customer choice making. This study allows in knowing the mindset of the frugal consumers who can assist advertising management in promoting sustainable consumption and consumer welfare. It is indicated that consumers who are frugal spend fewer portions of their monthly earnings on living expenditure. Frugality lowers monthly spending, as it undoubtedly influences the incentive to keep. Frugal purchaser lowers usual month-to-month spending and spending on customer items which can be priced efficiently in favor of commodities which are priced less (Pan et al., 2019). After doing numerous researches, the authors came to a conclusion that frugality is a “one-dimensional consumer life-style trait”. Frugality has substantially prolonged the knowledge of the traits of the segments (Coskun & Yetkin Özbük, 2019). The authors gave various suggestions which showed the significance of remaining frugal to acquire the market share which leads to economies of scale with cost benefit aspect (Malik et al., 2019). The study looks at measuring the dimensions related to problems in use of e-wallets and customer satisfaction with the help of a model. It studies the relationship between problems associated with the usage of e-wallets and customer satisfaction, and there is a significant difference (Yadav & Arora, 2018).

Due to the growing complexities in the consumers’ need of e-wallets, mobile transfers, and mobile banking, digital wallet has made a significant change (Slade et al., 2015). People have started trusting and adopting online shopping additionally as online payment services. The study aimed to deepen further our understanding of frugality in buying behavior by examining its association with (frugality, values, lifestyle, non-consumption) variables during the survey (Todd & Lawson, 2003). Trust acts as a key factor which affects the user’s agenda to use e-wallets. There is an established relationship between trust and attitude towards the usage of e-wallets (Trivedi, 2016).

E-wallets encourage increase in sales since customers use digital pockets with the enhanced technology and pressing situation (Sivakavitha & Bhuvaneswari, 2017). Convenience, transaction in online mode, and useful approach of e-wallet are the major factors among consumers. The influential factors affect the adoption of consumers (Bhagyashri & Pachpande, 2018). There exists an established associaton among the “Intention to Use E-wallets” and “Perceived Ease of Use” as the test proves that the null hypothesis is rejected (Nag, 2019).

Privacy and transaction-related security issues have been identified as the important aspects among the users (Doan, 2014). An individual’s intention is attributed to the individual’s usage-related behavior of mobile wallet (Shin, 2019). Techies are moving towards the retail experiences (Rathore, 2016). The factors which influence consumers are better understood through technology acceptance model (TAM; Shaw, 2014). Social influence indirectly affects the intention of mobile payment usage (Rani, 2014). The results of the analysis to find the association among risk, security, and the use of e-wallets intentions proved positive as it showed a good significant relationship between the two variables (Nag, 2019).

There were further studies which were done to examine how value co-creation is created and what are its effects on customers and companies (Lawson, 2003). According to the various studies done on the frugal consumers, “Buying Behavior” concluded that frugality restricts expenses by increasing the motivation to save. Frugality decreases expenses by enhancing the urge to save (Pan et al., 2019). Various factors are responsible which impact the buying behavior of frugal consumers (Malik et al., 2019). Attitude is considered as one of the variable digital transactions (Kurniawan, 2019).

The study establishes the positive effect between “Perceived Ease” and “Perceived Usefulness” with an impact on the attitude while using the e-wallet applications (Kustono et al., 2020). The findings reveal the motive of different countries in support by the respective government authorities towards the use of e-wallets. Further, it also describes the mediated effect of the variables in using the e-wallets (Aji et al., 2020).

Research Methodology

The data for the research was gathered by the respondents of the survey with a questionnaire. There was a precondition that the respondents of the survey should have an Internet-connected smartphone. The survey was conducted through both online and offline channels using smartphones. A 5-point Likert scale was framed which consisted of 17 items to assess the variables of independent factors and further 8 items were applied to evaluate the behavior intention of the user. All the items were also used to identify the frugality of the consumer. The data was collected by the method of convenience sampling with sample size of around 381 respondents to understand frugal consumer’s adoption behavior.

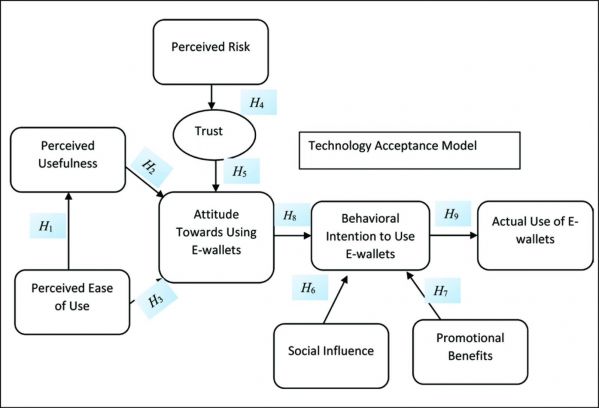

Conceptual Framework

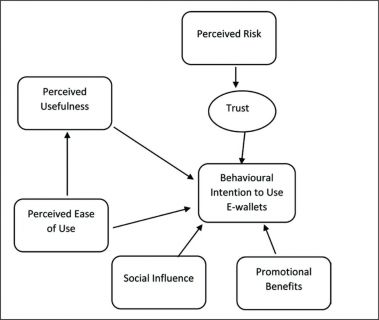

The ultimate focus of the framework was to find out variables which affect or promote the use of e-wallets.

With the inputs from literature review, the model is developed as depicted in Figure 1 which is conceptual.

Figure 1. Conceptual Framework Model

Hypothesis

Based on the review of literature, five factors—Promotional Benefits (PB), Behavioral Intention (BI), Ease of Use (EU), Technology Fit (TF), and Social Influence (SI)—were identified as antecedents of frugal consumers’ behavioral intention which is focused further on the adoption of the wallet apps. The association was tested among “Behavioral Intention” with reference to the adoption of the app and its antecedents. The following hypotheses were formulated.

H1: There is a significant and a positive association between frugal consumers’ “Perceived Ease of Use” of e-wallets and “Perceived Usefulness.”

H2: There is a direct association between “Perceived Usefulness” and “Attitude” towards using e-wallets.

H3: There is a direct association between “Perceived Ease of Use” of e-wallets and “Attitude” towards using e-wallets.

H4: There is a direct association between “Perceived Risk” and “Trust” to buy using e-wallets.

H5: There is a significant and a positive association between “Trust” and “Attitude” towards using e-wallets.

H6: There is a significant and a positive association between “Social Influence” and “Behavioral Intention” to use e-wallets.

H7: There is a significant and a positive association between “Promotional Benefits” and “Behavioral Intention” to use e-wallets.

H8: There is a direct association between “Attitude” towards using e-wallets and the “Behavioral Intention” to buy using e-wallets.

H9: There is a direct association between “Behavioral Intention” to use e-wallets and the “Actual Usage” of e-wallets.

Data Analysis

Demographics

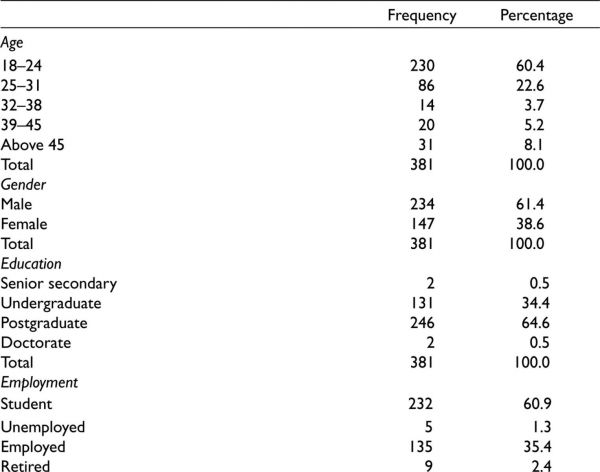

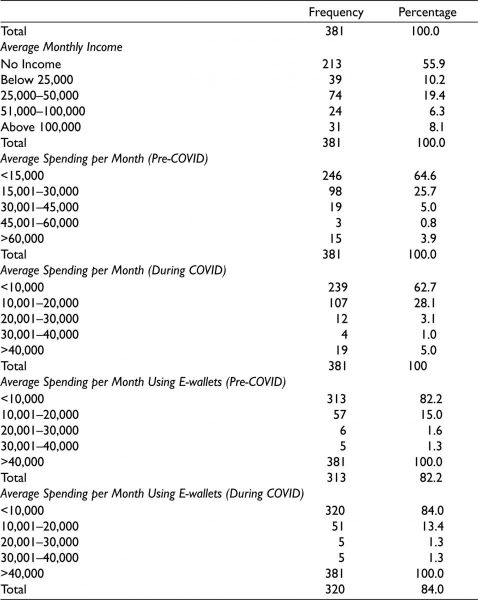

The classification of respondents with percentage is depicted in Table 1. With respect to age groups, respondents between 18 and 24 years of age constitute the majority of the sample with 60.4% followed by the age group of 25–31 constituting 22.6% of the total sample size. It is observed that 61.4% of the respondents were male and the rest 38.6% were female. With reference to education, 64.6% of the respondents were postgraduates and 60.9% of the respondents were students. In addition to these straightforward statistics, we have 55.9% of the respondents with no source of income, and when it comes to expenditure, both pre-COVID-19 timeline and the duration of COVID-19 pandemic, the percentage values were nearly the same with a small increase in the expenditure during the COVID-19 pandemic in general. Expenditure using the e-wallets during the COVID-19 pandemic remained the same with a small difference that can be shown in Table 1 with the mean values showing the small decrease in expenditure using e-wallets.

Table 1. The Frequencies of the Demographic Variables Measured on the Nominal Scale

Exploratory Factor Analysis

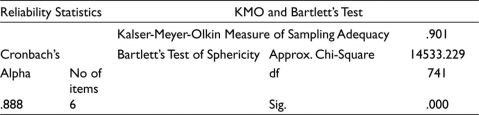

Kaiser-Meyer-Olkin (KMO) and Bartlett’s tests were done to check the sample adequacy. The value was 0.901, which comes in between the range of being excellent, and hence, we can clearly say that the factor analysis is apt for the collected data. The factor analysis has been done to reduce the quantity of factors under consideration for this study.

Interpretation: In Table 2, the Cronbach’s alpha value is 0.888, which shows the data collected is 88.8% reliable. The KMO value is 0.901, and the Bartlett’s test is found to be highly significant (p < .01); and thus, the factor analysis is suitable. Table 3 deals with the total variance explained for the same.

Table 2. Reliability Statistics, KMO and Bartlett’s Tests

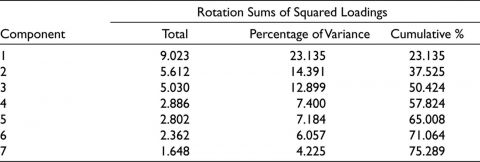

Table 3. Total Variance Is Explained

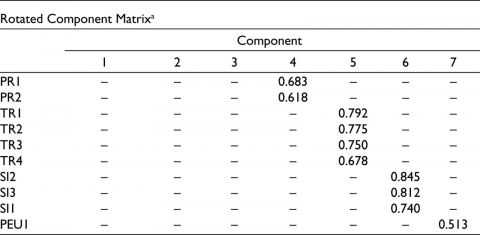

Table 4 is developed based on the rotation component matrix; 39 items were classified into 7 components.

Table 4. Rotated Component Matrix Table

Note: a The key output of principal components analysis.

Interpretation: From Table 4, it can be concluded that the first 12 items are categorized as Factor 1, and it is named as “Behavior Intention” (BI). Factor 2 has 9 items, and it is named as “Perceived Usefulness” (PU). Factor 3 has 6 items, and it is named as “Promotional Benefits (PB)”. Factor 4 has 4 items, and it is named as “Perceived Risk” (PR). Factor 5 has 4 items, and it is named as “Trust” (TR). Factor 6 contains 3 items, and it is named as “Social Influence” (SI). Factor 7 has only 1 item, and it is named as “Perceived Ease of Use” (PEU). “Actual Use” is denoted as AU.

The model developed in Figure 2 is based on the factor analysis.

Figure 2. Model Based on Factor Analysis

Regression Analysis

Regression analysis is done to ascertain the relationship among the variables and understand significant variables.

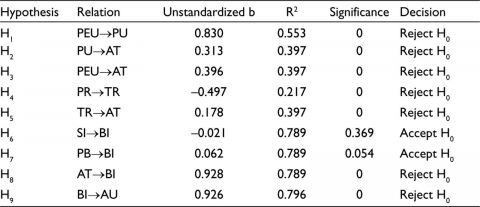

Interpretation: Table 5 depicts that there is a significant association among “Perceived Ease of Use” (PEU) and “Perceived Usefulness” (PU) of the e-wallets (H1), and it is also found to have a negative influence of “Perceived Risk” (PR) on “Trust” (H4). Table 5 also reveals a significant positive association among “Attitude” (AT) and “Perceived Usefulness” (H2), “Perceived Ease of Use” (H3), and “Trust” (H5). The table also shows a significant association among “Attitude” (AT) towards using e-wallets and “Behavioral Intention” (BI) to use e-wallets (H8). Also, a significant positive association can be seen among “Behavioral Intention” (BI) to use e-wallets and “Actual Usage” (AU) of e-wallets (H9).

Table 5. Regression Analysis to Ascertain Relationship Between the Variables

Notes:

PU = 0.830 * PEU + 0.502

TR = –0.497 * PR + 5.490

AT = 0.313 * PU + 0.396 * PEU + 0.178 * TR + 0.365

BI = 0.928 * AT + 0.134

AU = 0.926 * BI + 0.380

Data Analysis and Interpretation of the Study Conducted During Pre-COVID Situations

These values, tables, and text are taken from a previous study conducted during pre-COVID conditions. Only the most apt values with which a comparative study can be done are shown in Table 6.

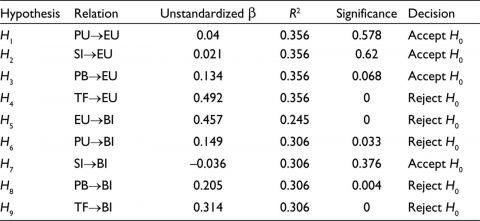

Table 6. Regression for Pre-COVID Conditions

Notes:

EU = 0.492 * TF + 1.331

BI = 0.457 * EU + 1.331

BI = 0.149 * PU + 0.205 * PB + 0.314 * TF + 1.524.

Interpretation: Table 6 depicts that there is a significant association among “Technology Fit” (TF) of the use of e-wallets and the “Ease of Use” (EU) of using the e-wallets to make purchases (H4), and there is also a positive impact of “Technology Fit” (TF) on “Behavior Intention” (BI) to buy using e-wallets (H9). It also shows that the “Ease of Use” (EU) to make purchases has a significant association with the “Behavior Intention” (BI) of the consumer to buy using e-wallets (H5). The promotional benefit has a significant impact on the “Behavior Intention” (BI) of the consumer to purchase using e-wallets (H8). The “Perceived Usefulness” (PU) of the e-wallet has a significant relationship with the “Behavior Intention” (BI) to buy using e-wallets (H6).

Findings and Discussion

The study described the frugality of the consumers by the nature of their buying behavior, and it also shows a strong relation between the frugal consumers and the positive influence of e-wallets on their buying behavior. The findings of the study can be applied by concerned organizations to improve their business model with respect to the variables mentioned. Our conceptual model explains the effect of “Perceived Ease of Use,” “Perceived Usefulness,” “Trust,” “Perceived Risk,” “Social Influence,” “Promotional Benefits,” “Attitude” on the “BehaviorIntention” to buy using e-wallets and the “Actual Usage” of e-wallets by frugal consumers. The results showed the significance and importance of model in order to understand the buying behavior of frugal consumers.

The current study has numerous implications to the concerned organizations and mobile banking services to explore new strategies for the mobile wallet usage and factors to keep in mind to know the buying behavior of frugal consumers. They are independent from the opinion of other people. Frugality reduces monthly expenses because it positively influences the intention and urge to save.

Companies that are into e-commerce, digital payments, and mobile banking services can make use of this study to understand that consumers are still frugal, although the perspective has changed from products to essential products, as they do not want to spend unnecessarily. These companies can, hence, make some changes in the offers that they provide to the customers. Although based on this study, “Promotional Benefits” has not been a major factor affected by the demographic variables, which proves that the consumers now are more health and priority oriented, it also can be said that offers given for the right products can attract the customers.

Conclusion

This study examined the customer’s intention to use e-wallets. This research has summed up that “Perceived Ease of Use,” “Perceived Usefulness,” and “Trust” shows an important role in tuning the attitude of consumer’s intention to adopt e-wallets. COVID-19 has pressurized people to start using digital payment-related applications. The usefulness of e-wallets and the ease of the usage of these digital wallets were seen as important factors that affect a consumer based on age, gender, employment, and also average income. With the advent of a lockdown and also a large number of people using the e-wallets for the first time, it can be seen that the “Perceived Risk” has an impact on the “Trust” of the consumer towards e-wallets which directly affects the “Behavioral Intention” and the “Actual Usage of the E-wallet.” With the imposition of the lockdown being taken, the study can also be conducted to analyze further change in the consumer’s behavior towards e-wallets and also towards the usage of promotional benefits which has seen a major drop in the COVID situation. Thus, through this study, the behavioral change in the consumer towards the use of e-wallets is studied, observations are noted, and conclusions are made based on these observations. During post-COVID times, some factors may get added to improve the model from the pre-COVID times. Multimodel analysis using structural equation modeling can be taken up in the future scope of the work.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Aji, H. M., Berakon, I., & Husin, M. M. (2020). COVID-19 and e-wallet usage intention: A multigroup analysis between Indonesia and Malaysia. Cogent Business & Management, 7(1), 1804181.

Bhagyashri, R., & Pachpande, A. A. (2018). Study of e-wallet awareness and its usage in Mumbai. Journal of Commerce & Management Thought, 9(1), 33–45.

Co?kun, A., & Yetkin Özbük, R. M. (2019). Environmental segmentation: Young millennials’ profile in an emerging economy. Young Consumers, 20(4), 359–379.

Dehkordi, G. J., Rezvani, S., Rahman, M. S., Fouladivanda, F., & Jouya, S. F. (2012). A conceptual study on e-marketing and its operation on firm’s promotion and understanding customer’s response. International Journal of Business and Management, 7(19). https://ccsenet.org/journal/index.php/ijbm/article/view/17362

Doan, N. (2014). Consumer adoption in mobile wallet: A study of consumers in Finland. Turku University of Applied Sciences.

Kumar, N. (2016). Growth drivers and trends of e-wallets in India. Manthan: Journal of Commerce and Management, 3(1), 65–72.

Kurniawan, B., Wahyuni, S. F., & Valentina, T. (2019) The influence of digital payments on public spending patterns. Journal of Physics: Conference Series, 1402(6), 066085.

Kustono, A. S., Nanggala, A. Y. A., & Mas’ud, I. (2020). Determinants of the use of e-wallet for transaction payment among college students. Journal of Economics Business & Accountancy Ventura, 23(1), 85–95.

Lawson, S. T. (2003). Towards an understanding of frugal consumers. Australasian Marketing Journal (AMJ), 11(3), 8–18.

Madan, K., & Yadav, R. (2016). Behavioural intention to adopt mobile wallet: A developing country perspective. Journal of Indian Business Research, 8(3), 227–244.

Malik, A. Suresh, S., & Sharma, S. (2019). An empirical study of factors influencing consumers attitude towards adoption of Wallet Apps. International Journal of Management Practice, 12(4), 426–442.

Nag, K. A., & Gilitwala, B. (2019). E-wallet-factors affecting its intention to use. International Journal of Recent Technology and Engineering. International Journal of Recent Technology and Engineering (IJRTE), 8(4). https://doi.org/10.35940/ijrte.D6756.118419

Orhun, A. Y. (2016). Frugality is hard to afford. Journal of Marketing Research, 56(1), 1–17.

Pan, L. (Sunny), Pezzuti, T., Lu, W., & Pechmann, C. (Connie). (2019). Hyperopia and frugality: Different motivational drivers and yet similar effects on consumer spending. Journal of Business Research, 95(C), 347–356.

Rani, P. (2014). Factors influencing consumer behaviour. International Journal of Current Research and Academic Review, 2(9), 52–61.

Rathore, D. H. (2016). Adoption of digital wallet by consumers. BVIMSR’s Journal of Management Research, 8(1). https://bvimsr.org/wp-content/uploads/2020/04/10.-Dr-Hem-Shweta-Rathore.pdf

Shaw, N. (2014). The mediating influence of trust in the adoption of the mobile wallet. Journal of Retailing and Consumer Services, 21(4), 449–459.

Shin, D.-H. (2019). Towards an understanding of the consumer acceptance of mobile wallet. Computers in Human Behavior, 25(6), 1343–1354.

Sivakavitha, S., & Bhuvaneswari, D. (2017). An intellectual study on preference towards the usage of electronic wallets among urban population of Chennai city. Imperial Journal of Interdisciplinary Research, 3(9), 894–898.

Slade, E., Dwivedi, Y. K., Piercy, N. C., & Williams, M. D. (2015). Modeling consumers’ adoption intentions of remote mobile payments in the UK. Psychology and Marketing, 32(8), 860–873.

Todd, S., & Lawson, R. (2003). Towards an understanding of frugal consumers. Australasian Marketing Journal, 11(3), 8–18.

Trivedi, J. (2016). Factors determining the acceptance of e-wallets. International Journal of Applied Marketing and Management, 1(2), 42–53.

Yadav, M. P., & Arora, M. (2018). A study on impact on customer satisfaction for e-wallet using path analysis model. Innovation Finance & Accounting. https://events.rdias.ac.in/wp-content/uploads/2021/06/6.-A-Study-on-Impact-on-Customer-Satisfaction-for-E-Wallet-Using-Path-Analysis-model.pdf