IIMS Journal of Management Science

Search

Search

Arpita Ghosh1 , Ananya Das2 and Poulomi Bhattacharya2

, Ananya Das2 and Poulomi Bhattacharya2

1 Symbiosis Centre for Management Studies, Symbiosis International (Deemed University), Pune, Maharashtra, India

2 Indian Council for Research on International Economic Relations (ICRIER), New Delhi, Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Supporting systems and measures continue to proliferate worldwide as more nations declare their commitment to net zero in response to adverse climate changes. To achieve net zero by 2070, it is crucial that Indian businesses focus on business sustainability by incorporating detailed information related to sustainable development goals in their disclosures. This study discusses critical focus areas based on three dimensions, namely economic, social, and environmental using bibliometric and sensitivity analysis for integrating the issue of sustainability into the business operations in India. Businesses that embrace sustainability can reduce risks, add value for stakeholders and forward the objectives of sustainable development. R-studio and VOS viewer were used to conduct bibliometric analysis for the last 30 years publication in this domain on 506 documents published. The study critically puts forward ways to increase the general public’s understanding of environmental issues using sensitivity analysis. The study identifies lack of government funds, green taxonomies, peer group discussions, and training programs that could lead to new possibilities for developing a sustainable environment in India. Furthermore, the study aims to assist managers upholding sustainability values in comprehending the relevant green practices. The study’s findings indicate the need for additional future investigations that empirically examine the components of sustainable organizational success.

Sustainability, strategy, supply chain, organizations, ESG

Introduction

The effect of climate change is visible everywhere, right from weather patterns to our health and world economy. Every year there are more than a billion deaths due to air pollution. The UNFCCC’s Nationally Determined Contribution Synthesis Report, 2022, warned that even if all existing climate pledges were delivered, the world would be heading for 2.4__degreesignC of warming by the end of this century, far ahead of the safe limit of 1.5__degreesignC. India has the densest population and is considered the most populous country in 2023 (United Nations, 2023). With increasing population, resource exploitation, and pollution, India has become a major stakeholder in the succession of sustainable development goals (SDG) as well.

Sustainability seeks to ensure intergenerational equity and is frequently characterized as development that “meets the demand of the present without compromising the potential of future generations to satisfy their own needs” (United Nations, 1987). It is increasingly crucial for firms to embrace sustainable practices in order to improve the continuity and future prospects of their business (Cheema et al., 2020). Seventeen SDGs were also proclaimed in this context at the United Nations Sustainable Development Summit in 2015 for setting the global objectives to address the grave economic, social, and environmental concerns. Since then, governments in many wealthy and developing nations have passed regulations requiring enterprises to find more sustainable solutions for their operations as a result of the rapid depletion of natural resources and rising pollution (El-Kassar & Singh, 2019).

The target for reducing the carbon emission intensity announced by India in COP 28 is an important agenda to achieve by 2030 (Das & Ghosh, 2023). For that, industries need to reduce their carbon footprint, reduce fossil fuel burning, and so on by more usage of renewable energy sources (Sheng et al., 2024; Trivedi et al., 2024). Further, climate risks continuously threaten many business sectors economically. The traditional businesses must start making significant strategic changes if they want to integrate sustainability into their everyday operations. Modern academics have proposed green in this situation (Fatoki, 2019; Ghosh et al., 2023; Harris & Crane, 2002; Kim et al., 2014; Paillé et al., 2014; Pham et al., 2019; Roscoe et al., 2019; Smith & Muller, 2016; Wang, 2014).

The incorporation of green ideals within the organization’s mission statements, strategy plans, and internal communities can assist eco-friendly corporate management methods (Kucukoglu & Pinar, 2015; Pradhan et al., 2020; Yong et al., 2020, Yusliza et al., 2020). Another study conducted by Kamble et al. (2019) asserts that corporations can only satisfy multiple needs of stakeholders if they give equal priority to the 3Ps—profit, people, and planet. Elkington (1998) introduced the idea of the triple bottom line, which contends that an organization’s ability to sustain itself depends on how well it performs in terms of its economic, environmental, and social performance. As an emerging field of study, sustainable organizational performance, this idea has arisen (Hao et al., 2021; Khan et al., 2021; Iqbal et al., 2020; Shahzad et al., 2020).

Inception of the Idea

As explained in the previous section, focusing on business sustainability is crucial to achieve net zero targets. The importance of sustainable business practices in international companies, based on observations from Indian and international publications, was focused. The study emphasizes the vital role that sustainability plays in promoting long-term value creation, reducing risks and building resilience in a world that is changing quickly by combining information from several sources. The incorporation of viewpoints from Indian periodicals emphasizes how applicable and pertinent sustainability issues are, given the socioeconomic situation of India.

International publications have chronicled the development of sustainable techniques in great detail, emphasizing how they have revolutionized industries and businesses of all kinds (Smith & Jones, 2023). Research indicates that the incorporation of sustainability principles into business operations results in increased competitiveness, enhanced brand equity, and superior financial outcomes (Johnson & Patel, 2024). Furthermore, by tackling urgent global issues like resource scarcity, social inequity, and climate change, sustainability programs help.

Indian journals provide special perspectives on the applicability of sustainable techniques in the Indian environment. According to literature, Indian companies are realizing more and more how crucial sustainability is to spurring innovation, drawing in capital, and satisfying stakeholder expectations (Kumar & Gupta, 2022). Furthermore, the implementation of sustainability programs is vital in tackling India’s socio-economic predicaments, encompassing issues like poverty reduction, rural development, and environmental preservation.

There is a convergence of global and Indian attitudes regarding the significance of sustainability practices in enterprises, even though the particular challenges and opportunities may differ across areas (Sharma & Singh, 2021). Indian and international journals agree that companies must embrace social responsibility, ethical governance, and environmental stewardship as part of a comprehensive strategy for sustainability. Furthermore, it is believed that long-term success depends on the incorporation of sustainability into fundamental corporate strategy.

The research by World Bank revealed that sustainability attracts more stakeholders to invest and employees to retain. To sustain a business in long term, investing for sustainability matters a lot. Many companies apprehend that due to low environmental, social, and governance (ESG) score, their company may face loss by losing support from investors (Sustainalytics, 2022). However, it should be noticed that there remains a huge disparity in ESG scores provided by different organizations due to individual reporting structures followed by them (Bhattacharya & Chakrabarty, 2023). Therefore, a unified structure should be followed. The top priorities of companies are obviously reducing carbon emission. To create sustainability reports that comply with government and consumer requirements, many firms opt to use frameworks of global reporting projects. However, in order to attract investors, the organizations could falsely claim to be green and sustainable—popularly known as “green wash” (Bhattacharya, 2022; Bhattacharya & Chakrabarty, 2023). Greenwashing is done by organizations to create investor confidence and receive funds with claims that are not credible. This could not just divert resources from eligible green players who could be medium-scaled firms and also create more unsustainable environment with polluting firms getting funds by mimicking. In order to ensure credibility of the disclosures by business organizations, it is important to identify the appropriate parameters that could assess and track business practices. The Business Responsibility and Sustainability Reporting (BRSR) by SEBI in 2021 has put forward some performance-based indicators like scope of emissions, carbon emissions, waste generated, energy consumed, and so on in Principle 6 to gauge an organization’s sustainable business practices. However, Bhattacharya and Chakrabarty (2023) show that it is not just carbon emissions that should be focused but per unit change in emissions with respect to a change in energy consumed that should be considered to track greenwashing. Alternate parameters like absolute difference between the change in emissions and change in energy consumed with respect to their level of market capitalization (representing organization’s capacity to reduce environmental damages) assist in identifying greenwashing. In order to spread the concept of environmental protection, the government must also invest more money in promoting sustainable products and regulations.

Statista (2021) shows the general mindset toward sustainability—global consumer survey from different countries including India.

Given the fact that the consumption demand for goods would increase with a huge increase in urban population, which is estimated to reach 590 million by 2030 (McKinsey, 2010), the economic output of these cities is expected to grow over time. Increase in output would then be accompanied by increase in emissions thus disturbing the environmental sanctity. Therefore, it becomes crucial for enterprises to address the business sustainability challenges in cities. Brundtland’s study from 1987 supports this conjecture that cities’ sustainability may be evaluated by looking at three factors: economic, social, and environmental, which together form the basis of sustainable performance (Büyüközkan & Karabulut, 2018). Sustainable consumption is a crucial factor in inducing sustainable business practices.

Furthermore, there is a huge need to explore differences in the business sustainability research domain and trend in developed and developing nations. A report entailed that renewable energy and freed-up investment will more than make up for the losses to the global economy, which will be suffered by countries that are sluggish to decarbonize, but early adopters will benefit. It emphasizes the danger of producing significantly more oil and gas than is necessary to meet future demand (Fossil Fuels, 2021). Citizens need to move toward sustainable lifestyle.

In light of the discussions above, this study attempts to answer the following research questions:

Relevant Literature on Sustainable Practices

According to a study’s findings (Attaianese, 2012; Roscoe et al., 2019), a green organizational culture encourages employees to participate in pro-environmental actions. After some time, however, the employees develop a behavior that gives them the authority to act with sustainability goals in mind. An employee who practices pro-environmental behavior will typically try to eliminate unnecessary production procedures (Simpson & Samson, 2010). According to a study by Dubey et al. (2017), organizational culture has a big impact on how pro-environmental and concerned people are about sustainability issues. In the period of sustainable development, an organization’s performance with regard to society, the economy, and the environment is referred to as sustainable organizational performance (Argandoña & von Weltzien Hoivik, 2009).

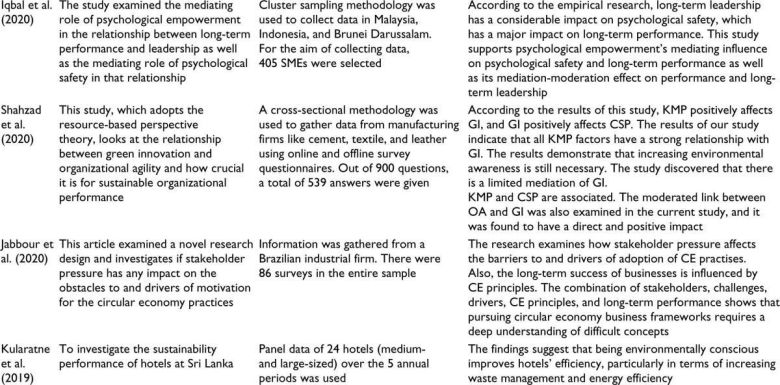

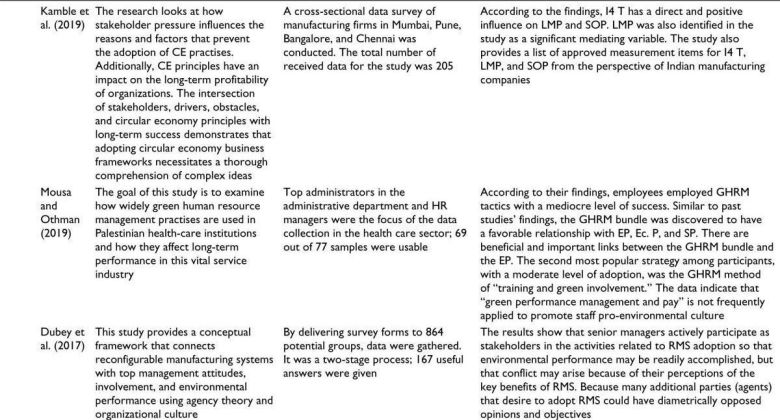

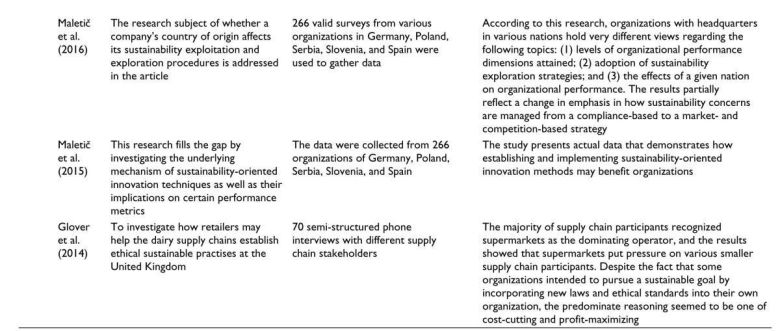

Review of the literature based on sustainable practices is shown in Table 1. The importance of eco-innovation methods in promoting the sustainable performance (economic, social, and environmental performance) of any company is the focus of a 2010 study by Carrillo-Hermosilla et al. According to this study, in order to achieve sustainable performance, certain business processes can make use of dimensions like design amplitude, user amplitude, product amplitude, governance amplitude, and stakeholders’ commitment to the process of sustainable innovation, which will ultimately lead to a sustainable society. Young and Tilley’s (2006) study emphasizes the importance of business leaders in reshaping the corporate sustainability landscape. These managers inspire their staff to view sustainability as a chance rather than a duty by encouraging them to view it as an opportunity.

Table 1. Literature Based on Sustainable Practices in Business.

In recent years, bibliometric studies in the domain of sustainability have been increased to showcase the research focus and its need in developing countries. According to Nobanee et al. (2021), USA was the first country to initiate research in more depth on work practices of sustainability. They did bibliometric analysis on sustainability and risk management. A bibliometric study was performed on “Sustainability and Corporate Social Responsibility” by Meseguer-Sánchez et al. (2021) and observed top research countries in this domain as the United Kingdom, Germany, and the Netherlands. China is seen to be the most prolific country with 1,893 publications on sustainability bibliometric study by Tang et al. (2018). A bibliometric study was conducted on “corporate sustainability” in 2005–2021 duration and was found that USA is the top highest publishing country in this research domain (Jan et al., 2023). Ensslin et al. (2022) conducted bibliometrics on Sustainable Management of Libraries in Higher Education Institutes and found it is an important aspect among stakeholders. Agrawal et al. (2022) reported bibliometrics analysis on sustainability of supply chain practices. A bibliometric study was performed on sustainable business performance by Bota-Avram (2023) and concluded that sustainability is the most trending topic in research in future time. Sustainability in organizations was bibliometrically analyzed by Ogutu et al. (2023). A bibliometric study was performed on “Sustainable business model innovation” by Pan et al. (2023).

Another study conducted by Rennings et al. (2006) covered various sustainable business practices that can improve an organization’s overall sustainability performance. In this essay, process innovation, product innovation, and organizational innovation were the three key themes highlighted. By streamlining the manufacturing process and generating the best output with the fewest inputs, process innovations contribute to an improvement in the economic performance of the organization. The second is product innovation, which corresponds with the manufacturing of items that are sustainability-oriented, including recycled goods and goods made of organic materials. This aids businesses in improving their financial performance because using effective production methods makes it simple for them to generate higher earnings. The third category is organizational innovations, which is the creation of novel management techniques that support the concept of sustainability. Different organizations have embodied holistic environment-friendly systems which serve as a dynamic for the improvement of the overall business performance.

Beske et al. (2014) discussed about sustainable supply chain importance in food industries. The elements of sustainable performance are accurately measured by a study based on lean manufacturing techniques (Sajan et al., 2017). The use of 14T, or industry 4.0, technology by businesses has been found to have a greater favorable impact on long-term organizational performance. In this study, it was emphasized that 14T plays a significant role in enhancing an organization’s performance in terms of its economic, social, and environmental performance. Economically speaking, 14T technologies allow for more flexible manufacturing and product customization, which further boosts client satisfaction and revenue. Employees also get the chance to pick up novel manufacturing processes, which boosts their motivation and morale in terms of social performance. Additionally, 14T technologies contribute to lowering greenhouse gas emissions, excessive fossil fuel usage, and lead to proper utilization of the resources.

This study also examines how ESG aspects are changing in the context of Indian supply chains and business. Through an analysis of ideas from multiple Indian journals such as Gupta and Sharma (2022), Patel and Desai (2023), Reddy and Singh (2024), and Sharma and Kumar (2021), it looks at how ESG integration is now understood, what it means for organizations, and what opportunities and difficulties lie ahead. The study also looks at possible approaches to deal with these issues and improve the efficiency of ESG practices in the Indian business community. The incorporation of ESG considerations has become increasingly popular worldwide as companies realize the value of sustainable operations (Gupta & Sharma, 2022). In India, where social and environmental issues coexist with economic expansion, ESG plays a critical role in supply chain and corporate management (Sharma & Kumar, 2021), in order to clarify the present situation of ESG practices, pinpoint areas in need of development, and suggest future paths for improving. In conclusion, domestic demands and worldwide trends are driving a rapid evolution of the function and breadth of ESG in Indian supply chains and industry. Stakeholders can work together to solve obstacles and capture opportunities for developing a more equitable and sustainable economy in India through ongoing study, discussion, and action. In ESG implementation, this study explores the body of literature from Indian publications.

While the literature has mostly focused on the factors that lead to sustainable business, the literature on credible reporting of sustainable practices undertaken is not explored much in developing economies, especially in India (Afsar & Umrani, 2020; Ansari et al., 2021). A bibliometric study on greenwashing by Santos et al. (2023) shows that the study of greenwashing in developing countries is scant. It includes one paper that is India based with respect to awareness toward greenwashing, consumer preferences, and green and sustainable consumption (Jog & Singhal, 2020). The literature on greenwashing in developed countries has mostly focused on corporate social responsibility in banking industry and financial performance, drivers of greenwashing, and their impacts and reporting overview. Sensharma et al. (2022) show how ESG and CSR disclosure scores in India could identify greenwashing practices of firms. On the other hand, Bhattacharya and Chakrabarty (2023) show that relying on ESG scores could also be misleading given the fact that there exists disparity in the reporting format of organizations, which could not compare across companies. They could also be attributed to the gap in understanding the difference between “clean” and “green,” which has not been clear yet. This article prescribes certain firm level parameters that should be focused to track greenwashing. Bhattacharya (2022) stresses the role of financial institutions to track such greenwashing. These articles focused on Indian business and proposes avenues of further research. Other issues of sustainable supply chains have been focused in the bibliometric section of this article to identify the gaps in research on sustainability in India.

Methodology

To measure a researcher’s impact on the field of research, bibliometrics statistically evaluates publications. We searched for papers using the renowned research database Scopus. Different searches were conducted using various keyword combinations such as “sustainable practice,” “organization,” and “business.” The appropriate article list was stored as a.csv file. Instead of selecting “all fields (total 17,000 articles),” the “article title” filtering criterion was used. Using the terms with “sustainable practice,” 506 documents (including book chapters: 48, articles: 309, conference papers: 84, reviews: 35, books: 12, note: 6, editorial: 5, conference review: 4, short survey: 2, letter: 1) were found.

The steps to simulate the database are as follows (Figure 1):

Stage 1: Scopus Database search, Keywords “sustainable-practice” in all field (17,000 article total found).

Stage 2: Filtration with article field only.

Stage 3: Language filtration (English).

Stage 4: Found 506 articles—384 sources and downloaded as .csv file.

Stage 5: Bibliometric review.

Figure 1. (a) Identification of Steps to be Followed Using PRISMA Framework. (b) The Framework of This Study.

The search was conducted on October 22, 2022. For the bibliometric analysis, R-studio Biblioshiny for Bibliometrix was used majorly in this study, whereas for some collaboration NETWORK analysis, the VOSviewer tool (1.6.18 for Microsoft Windows system) was also used. Further, Google News on “Sustainable-practice” last 2 weeks was converted into .csv file and explored via R-studio to understand the important words, frequency, and emotion.

Analysis and Discussion

Bibliometric Trend

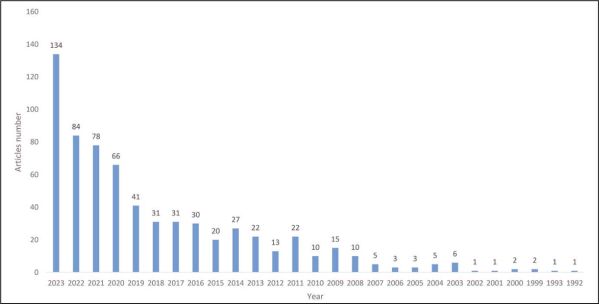

The supplementary image shows the main information like 384 sources for 506 documents, time span 1992–2022 (30 years), annual growth rate 15.1%, total 1,446 authors, 3.02 authors, 1,459 keywords in each publication, and so on in the research domain of sustainable practice. The average citation rate was observed to be 9.091 per document.

It was investigated how literature has changed over the past 30 years. The annual scientific output in this field of study is depicted in Figure 2 for the period of 1992–2022. From 1992 to 2002, a fairly slow publication pace (1–2 publications per year during this time) was seen. There has been a light rise in publications from 2003 to 2007 period (3–6 documents/year). From 2008 (10 documents), the significant rise has been observed till 2022. There were 65 and 76 publications in the most recent years of 2020 and 2021, respectively. Researchers are more interested in this type of research now than ever before because of the worldwide issue of climate hazards.

Figure 2. Annual Scientific Production in Last 30 Years in the Sustainability Domain.

Source: Scopus Database.

Figure 3 displays that the renowned journals in this field within the scholarly community are Journal of Cleaner Production (29 documents) and Sustainability (18 documents).

Figure 3. Top Journals in the Sustainability Domain.

Source: Scopus Database.

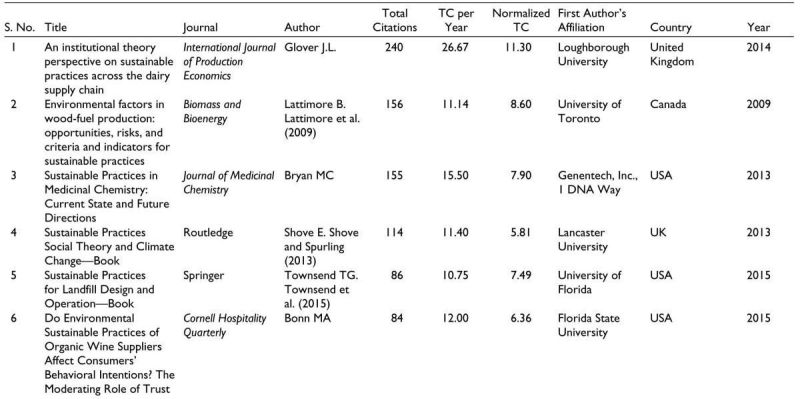

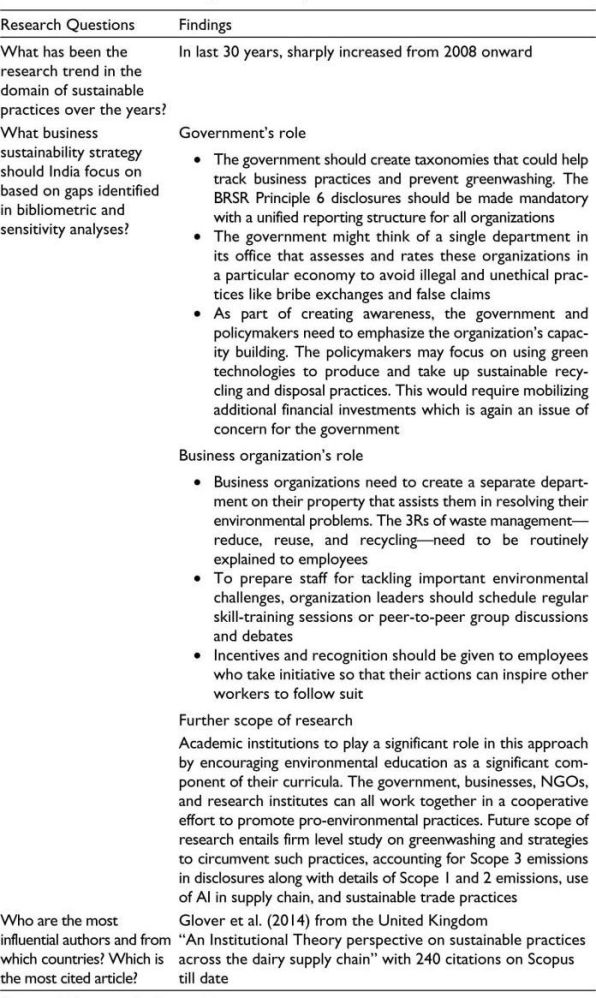

In the sustainable-practice domain from 1992 to 2022, the most notable documents are listed in Table 2. “An Institutional Theory perspective on sustainable practices across the dairy supply chain” authored by Glover J.L from Loughborough University, UK, received the highest number of Scopus citations (240) in this domain with total citations per year 26.67. Other influential authors are B. Lattimore, M. C. Bryan, and E. Shove from developed nations Canada, USA, and the United Kingdom, respectively (Bryan et al., 2013). It reveals that developed nations are more progressive in thought, research, and strategic planning regarding sustainable practices from the past.

Table 2. The Top 10 Most Cited Publications.

Source: Bibliometric Analysis and Google Scholar.

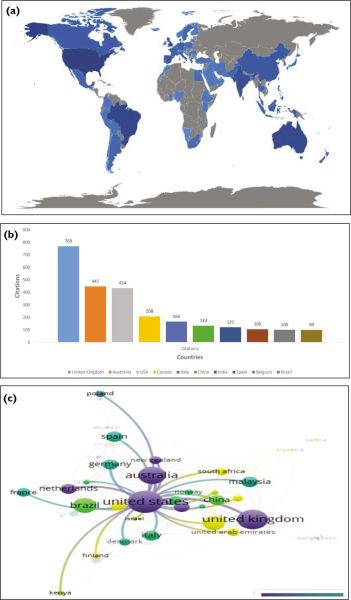

Figure 4a–c shows the influential countries in the research domain related to documents, citations, and collaboration network among the research countries. The United Kingdom received highest 769 Scopus citations in this domain followed by Australia (447), USA (434), and Canada (208). Among 80 countries 72 met the filtering threshold of minimum citation and document of 1. The major collaboration network among countries was observed among USA, Canada, Australia, New Zealand, Netherland, and Poland.

Figure 4. (a) Country Scientific Production in the Sustainability Domain. (b) Most Cited Countries in This Research Domain of Sustainability Practices. (c) Collaboration Network Between the Major Research Countries.

Source: (a) Scopus Database; (b) R-studio Analysis; (c) VOSviewer Analysis.

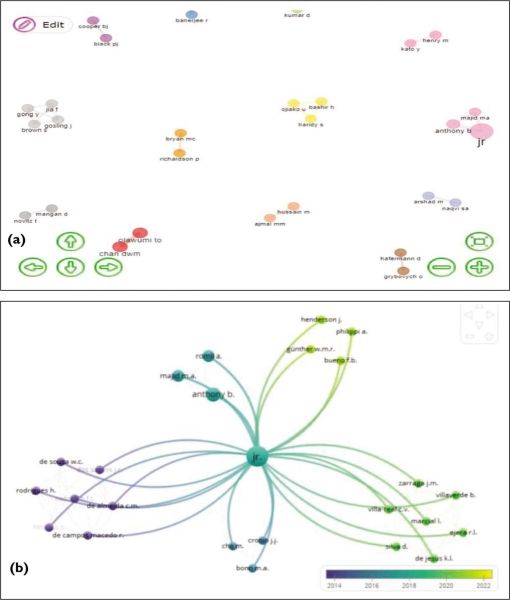

Figure 5a and b shows the collaborative network among the major authors. The collaboration network shows research among scientists like D. W. M. Chan with T. O. Olawumi, B. Anthony, M. A. Majid Jr. (Figure 5a) has network with B. Anthony, A. Romli, M. A. Majid (Figure 5a).

Figure 5. (a) The Collaboration Network Among Authors by Biblioshiny. (b) The Collaboration Network Among Authors by VOSviewer.

Source: (a) R-studio Analysis.

However, a separate attempt was made to explore the influential Indian authors in this domain. The authors like V. Aravamudhan, D. Kumar, I. Kumar, K. Mehta, S. Sharma, and R. Nagariya were found in the research domain with two articles (highest). Among them, the highest cited (citations 990 in Scopus) researcher is Prof. Divesh Kumar from MNIT Jaipur. In his recent article, he has suggested how to increase academic research motivations toward sustainable consumer behavior (Sheoran & Kumar, 2022).

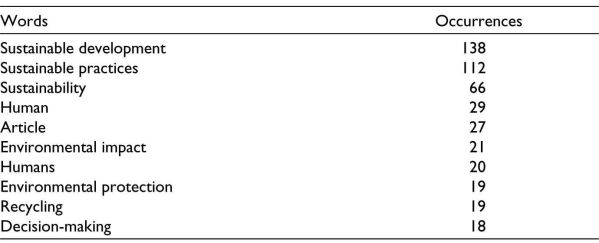

Figure 6a and b shows the word cloud, TreeMap of most frequent words in this research domain. Table 3 shows the mostly used words, their occurrences, and frequency. Sustained development, sustainable practices, sustainability, environmental impact, human, environmental protection, recycling, and decision-making are mostly sensitized words in this research domain with different frequency range (138–18). So, environment practitioners, decision maker, and climate leaders had inculcated strategies like recycling, sustainable practices to protect the environment and humans, and mitigate the environmental impact to achieve SDGs. As per Ehrlich or IPAT equation, we know that with increasing population, the impact on the environment also increased. Figure 7 (software-generated) shows the trending topics in the domain of sustainable practices in business which needs further attention in research, policy imposing, and so on. This figure shows the trending research topic in the domain from 2005 to 2021. It entails that before UN SDGs, that is, during the period of MDGs, gender equality and child development were majorly focused in the business sustainability domain. The male–female–adult research trends gained momentum during 2011–2013 following the goal of social and gender equality proposed in MDGs. From 2015, the focus shifted toward overall sustainable development, environmental protection, and human. During 2019, the major focus was on sustainability. This shows while initially socio-economic factors were given more importance, in the interim period emission-related studies came up which then led to the development of emission standards worldwide by nations. Now that recent years are focusing on sustainability issue, it implies that proper research avenues should be identified to develop robust firm-level policies.

Figure 6. (a) Words Cloud. (b) TreeMap.

Source: (a) R-Studio Analysis; (b) R-Studio Analysis.

Table 3. Most Frequent Words and Occurrences.

Source: Bibliometric Analysis.

Figure 7. Trending Topics from This Research Study.

Source: R-studio Analysis.

Source: R-studio Analysis.

Relevant News Analysis

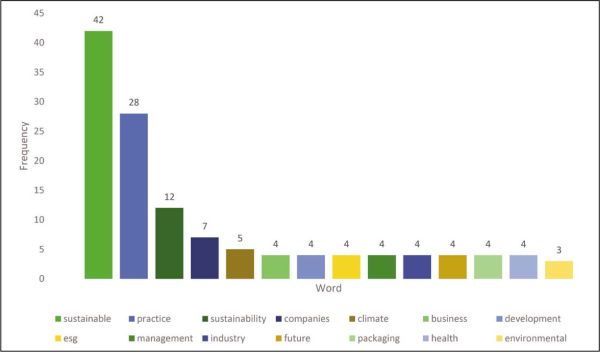

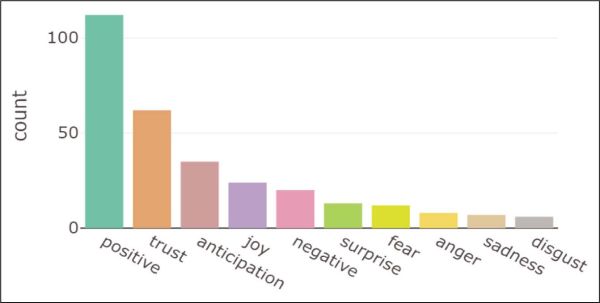

In recent years, social media has evolved into a virtual space where people can express their concerns about the environment, health, and other matters of public interest. The social media platform most encourages the expression of people–media opinion, because it encourages honest dialogue between users and makes it possible in the most widely accessible way (Chae, 2015; Park et al., 2020). A Google Search was made on Google News using the keyword “sustainable practice.” The search was made on May 30, 2022, using R studio. The search results were saved into .csv file and qualitatively analyzed through R studio. Analysis of the news articles showed the important of words cloud, their frequency, and their emotion on sustainable practice in business (Figures 8–10). Figure 8 and Figure 9 show that climate, sustainable development, ESG, business organizations, and management were most used words in those news. Figure 8 shows that most people’s emotion toward sustainable practice is positive and trustful. It entails that sustainable practice builds positive effect and trust among the system.

Figure 8. Word Cloud from News Articles.

Source: R-studio Analysis.

Figure 9. Word Frequency from News Articles.

Source: R-studio Analysis on News.

Figure 10. Emotion Type for Sustainable Practices.

Policy Implications from Bibliometric and Sensitivity Analysis

This subsection focuses on the factors influencing sustainable practices boiling down from the analysis done above-bibliometric and sensitivity analysis. The SDG 12 (i.e., responsible consumption and production) aims for 5R resource utilization principle like reduce, reuse, repurpose, recycle, and refuse. The open loop of linear material management like take–make–waste should be redirected to close loop of circular material management using 5R’s principle of resource utilization. The analysis from the bibliometric analysis and the sensitivity analysis above show that the developed nations also follow the circular material management of resources to achieve circular economy. This further leads to cost reduction and profit maximization with increase in productivity, that is, usage of a certain quantity of resources with minimum waste. Further climate investment for sustainable practices is extremely important nowadays at all business organizations. To achieve net zero carbon emission by 2070 (as promised in COP 26 at Glasgow), it is important to increase use of renewable energy rather than coal burning, prepare carbon sinks by green belts of trees, and so on. The policymakers need to focus in this direction more in developing countries mainly in most populated countries like India and China as these countries are major stakeholders for sustainability successfulness. The bibliometric analysis in Figure 7 shows that the sectors like hotel industry, health care delivery, supply chain management, leadership, construction industry, and project management in developing countries need to be focused for environmental sustainable practices, reuse, and recycling needs to be implemented for the resources (plastic, organic waste, and water resources) suitably rather than dumped in landfill or aquatic ecosystem; burning waste and increasing greenhouse gas emission or polluting water stream should be restricted. Further, the decision maker needs to motivate people in this direction by improving perception and giving visible incentives. Also, there were topics like human, adult, male, and female which reveal that human beings are major stakeholders in these sustainable practices. The sensitivity analysis shows that the organization’s transparency toward sustainable practices leads to more trust and creates further awareness in general societies leading to sustainable consumption and improves human health standards. Sustainable consumption is an important factor influencing sustainable business practices. Thus, there is a nexus between human health and environmental pollution sustainability.

Conclusion and Recommendation

An analysis of the numerous research mentioned in the above sections serves as the foundation for this study’s discourse. This study has made an effort to give a thorough analysis of the factors influencing sustainable practices by business organizations using bibliometric analysis and sensitivity analysis. Bibliometric analysis was performed using R studio and VOSviewer. Sensitivity analysis made use of the news contents understand the general awareness of sustainability and what influences sustainable practices. These analyses have been used in literature to raise researcher’s, policymakers’, and society’s awareness of environmental issues.

The research shows that climate consciousness has been steadily increasing over time. The most cited research paper is on sustainable practices in the dairy supply chain by a researcher from the United Kingdom. The research findings are also tabulated in Table 4. Appropriate recommendations have been suggested for all the stakeholders for enhancing the environmental concerns of the people at the societal level from trending topics in the analysis. The analysis assists in identifying the gaps in research to assess business sustainability in India. It not only guides on developed countries’ analysis trend that gives immense consideration to sustainable business but also identifies what needs to be focused by Indian businesses to attain business sustainability and hence its net zero target.

Table 4. The Research Findings in This Study.

Source: Bibliometric Analysis and Scopus.

This study offers important recommendations for the implementation of environment-friendly/business sustainable policies for organizations in India. The government and policymakers need to critically brainstorm the required policy to impose on business organizations to achieve sustainability. To prevent greenwashing, the government should create taxonomies that could help track business practices. The BRSR Principle 6 disclosures should be made mandatory with a unified reporting structure for all organizations. Legitimate parameters should be identified for reporting and the convenient monitoring of these reports. The government might think of a single department in its office that assesses and rates these organizations in a particular economy to avoid illegal and unethical practices like bribe exchanges and false claims. As part of creating awareness, the government and policymakers need to emphasize the organization’s capacity building. The policymakers may focus on using green technologies to produce and take up sustainable recycling and disposal practices. This would require mobilizing additional financial investments which is again an issue of concern for the government.

Nonetheless, it is not a one-sided work to be done by the government; the business enterprises are required to give more effort to ensure a sustainable environment with their business practices. This study recommends that businesses create a separate department on their property that assists them in resolving their environmental problems. The 3Rs of waste management—reduce, reuse, and recycling—need to be routinely explained to employees. Organizations can also work actively with NGOs engaged in the fields of sustainability and environmental protection to fulfill their corporate social obligations. Given that they prioritize environmental protection in addition to profit, this may increase the legitimacy of such organizations in the market. One employee’s pro-environmental values can simply be shared with their peer group. By considering the pro-environmental ideals through deeds rather than verbal debates, one employee can readily transmit them to their peer group. To prepare staff for tackling important environmental challenges, organization leaders should schedule regular skill-training sessions. Additionally, incentives and recognition should be given to employees who take initiative so that their actions can inspire other workers to follow suit.

With net zero targets in place, stakeholders are conscious about rationally investing in sustainable, green projects. They have an interest in evaluating the organization’s sustainability stance. For this reason, organizations must frequently communicate with them about their environmental reports and ESG score. In order to instill a sense of environmental worries in the public’s psyche, authorities should also levy environmental levies in their various states. Institutions at the national level should also make contributions in the form of high-caliber research projects that educate people about the negative effects of ecological degeneracy. On the basis of the analyses, this study consider academic institutions to play a significant role in this approach by encouraging environmental education as a significant component of their curricula. The government, businesses, NGOs, and research institutes can all work together in a cooperative effort to promote pro-environmental practices. Future scope of research entails firm level study on green washing and strategies to circumvent such practices. This study shows that substantial research scope exists in studying sustainable supply chains in India. Different aspects of sustainability could be focused in sectors like waste management, electric vehicle manufacturing, agriculture, sourcing critical metals. Studies on governmental sourcing of funds could add research avenues to create sustainable environment in India.

From the sustainability consciousness analysis among employees, the study yields valuable conclusions. Businesses that embrace sustainability can reduce risks, add value for stakeholders, and forward the objectives of sustainable development. The managers who are responsible for developing a culture that supports sustainability values would find the green practices useful.

To reduce maximum carbon emission from supply chain (Scope 3 source rather than Scope 1 and 2), the MSMEs are required to be made aware about the importance and accountability of carbon emission, which is a crucial parameter in ESG disclosure yet not a focused research topic in the literature. The reverse supply chain is also important to implement through artificial intelligence, which enables to reduce spoilage of many inventory items. In conclusion, research from international and Indian publications shows that the significance of sustainable business practices is cross-border. Therefore, sustainable trade practices also need to be taken care of, which paves way for another avenue of research. The study’s conclusions highlight how urgent it is to integrate sustainability into corporate decision-making procedures in order to promote a more just, resilient, and sustainable future for everybody.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplementary Material

Supplemental material for this article is available online.

ORCID iDs

Arpita Ghosh  https://orcid.org/0000-0002-4486-7613

https://orcid.org/0000-0002-4486-7613

Poulomi Bhattacharya  https://orcid.org/0000-0002-2326-8312

https://orcid.org/0000-0002-2326-8312

Afsar, B., & Umrani, W. A. (2020). Corporate social responsibility and pro-environmental behavior at workplace: The role of moral reflectiveness, coworker advocacy, and environmental commitment. Corporate Social Responsibility and Environmental Management, 27(1), 109–125. https://doi.org/10.1002/csr.1777

Agrawal, R., Majumdar, A., Majumdar, K., Raut, R. D., & Narkhede, B. E. (2022). Attaining sustainable development goals (SDGs) through supply chain practices and business strategies: A systematic review with bibliometric and network analyses. Business Strategy and the Environment, 31(7), 3669–3687.

Ansari, N. Y., Farrukh, M., & Raza, A. (2021). Green human resource management and employees’ pro-environmental behaviours: Examining the underlying mechanism. Corporate Social Responsibility and Environmental Management, 28(1), 229–238. https://doi.org/10.1002/csr.2044

Argandoña, A., & von Weltzien Hoivik, H. (2009). Corporate social responsibility: One size does not fit all. collecting evidence from Europe. Journal of Business Ethics, 89(Suppl 3), 221–234. https://doi.org/10.1007/s10551-010-0394-4

Attaianese, E. (2012). A broader consideration of human factor to enhance sustainable building design. Work, 41(1), 2155–2159.

Authors, C., Saleem, M., Mahmood, F., & Ahmed, F. (2019). Transformational leadership and pro-environmental behavior of employees: Mediating role of intrinsic motivation. Journal of Management and Research, 6(2), 113–137. https://doi.org/10.29145/jmr/62/060205

Beske, P., Land, A., & Seuring, S. (2014). Sustainable supply chain management practices and dynamic capabilities in the food industry: A critical analysis of the literature. International Journal of Production Economics, 152, 131–143.

Bhattacharya, P. (2022, June 24). The role of financial institutions to avert greenwashing, The GAIA perspectives. https://icrierclimatechange.wordpress.com/2022/06/24/the role-of-financial-institutionsto-avert-green-washing/

Bhattacharya, P., & Chakrabarty, H. S. (2023, October 4). Greenwashing in India Inc.: Environment scores create a sense of suspicion. Business Standard.

Bota-Avram, C. (2023). Bibliometric analysis of sustainable business performance: Where are we going? A science map of the field. Economic Research [Ekonomska istraživanja], 36(1), 2137–2176.

Bryan, M. C., Dillon, B., Hamann, L. G., Hughes, G. J., Kopach, M. E., Peterson, E. A., Pourashraf, M., Raheem, I., Richardson, P., Richter, D., & Sneddon, H. F. (2013). Sustainable practices in medicinal chemistry: Current state and future directions. Journal of Medicinal Chemistry, 56(15), 6007–6021. https://doi.org/10.1021/jm400250p

Büyüközkan, G., & Karabulut, Y. (2018). Sustainability performance evaluation: Literature review and future directions. Journal of Environmental Management, 217, 253–267.

Chae, B. (2015). Insights from hashtag #supplychain and Twitter analytics: Considering Twitter and Twitter data for supply chain practice and research. International Journal of Production Economics, 165, 247–259. https://doi.org/10.1016/j.ijpe.2014.12.037

Cheema, S., Afsar, B., Al-Ghazali, B. M., & Maqsoom, A. (2020). Retracted: How employee’s perceived corporate social responsibility affects employee’s pro-environmental behaviour? The influence of organizational identification, corporate entrepreneurship, and environmental consciousness. Corporate Social Responsibility and Environmental Management, 27(2), 616–629. https://doi.org/10.1002/csr.1826

Das, A., & Ghosh, A. (2023). Vision net zero: A review of decarbonisation strategies to minimise climate risks of developing countries. Environment, Development and Sustainability, 1–37. https://doi.org/10.1007/s10668-023-03318-6

Dubey, R., Gunasekaran, A., Helo, P., Papadopoulos, T., Childe, S. J., & Sahay, B. S. (2017). Explaining the impact of reconfigurable manufacturing systems on environmental performance: The role of top management and organizational culture. Journal of Cleaner Production, 141, 56–66. https://doi.org/10.1016/j.jclepro.2016.09.035

El-Kassar, A. N., & Singh, S. K. (2019). Green innovation and organizational performance: The influence of big data and the moderating role of management commitment and HR practices. Technological Forecasting and Social Change, 144, 483–498. https://doi.org/10.1016/j.techfore.2017.12.016

Elkington, J. (1998). Accounting for the triple bottom line. Measuring Business Excellence, 2(3), 18–22. https://doi.org/10.1108/eb025539

Ensslin, L., Dutra, A., Ensslin, S. R., Moreno, E. A., Chaves, L. C., & Longaray, A. A. (2022). Sustainability in library management in higher education institutions: A bibliometric analysis. International Journal of Sustainability in Higher Education, 23(7), 1685–1708.

Fatoki, O. (2019). Hotel employees’ pro-environmental behaviour: Effect of leadership behaviour, institutional support and workplace spirituality. Sustainability, 11(15), 4135. https://doi.org/10.3390/su11154135

Fossil Fuels. (2021). https://www.theguardian.com/environment/ng-interactive/2021/nov/04/fossil-fuel-assets-worthless-2036-net-zero-transition

Ghosh, A., Kumar, S., & Das, J. (2023). Impact of leachate and landfill gas on the ecosystem and health: Research trends and the way forward towards sustainability. Journal of Environmental Management, 336, 117708.

Glover, J. L., Champion, D., Daniels, K. J., & Dainty, A. J. D. (2014). An institutional theory perspective on sustainable practices across the dairy supply chain. International Journal of Production Economics, 152, 102–111. https://doi.org/10.1016/j.ijpe.2013.12.027

Gosling, J., Jia, F., Gong, Y., & Brown, S. (2016). The role of supply chain leadership in the learning of sustainable practice: Toward an integrated framework. Journal of Cleaner Production, 137, 1458–1469. https://doi.org/10.1016/j.jclepro.2014.10.029

Gupta, R., & Sharma, S. (2022). Integrating ESG principles into corporate strategy: Insights from Indian enterprises. Journal of Sustainable Business Management, 10(1), 45–60.

Hao, Z., Liu, C., & Goh, M. (2021). Determining the effects of lean production and servitization of manufacturing on sustainable performance. Sustainable Production and Consumption, 25, 374–389. https://doi.org/10.1016/j.spc.2020.11.018

Harris, L. C., & Crane, A. (2002). The greening of organizational culture: Management views on the depth, degree and diffusion of change. Journal of Organizational Change Management, 15(3), 214–234. https://doi.org/10.1108/09534810210429273

Iqbal, Q., Ahmad, N. H., Nasim, A., & Khan, S. A. R. (2020). A moderated-mediation analysis of psychological empowerment: Sustainable leadership and sustainable performance. Journal of Cleaner Production, 262, 121429. https://doi.org/10.1016/j.jclepro.2020.121429

Jabbour, C., Seuring, S., Jabbour, L., Jugend, D., De Camargo Fiorini, P., Latan, H., & Izeppi, W. C. (2020). Stakeholders, innovative business models for the circular economy and sustainable performance of firms in an emerging economy facing institutional voids. Journal of Environmental Management, 264, 110416. https://doi.org/10.1016/j.jenvman.2020.110416

Jan, A. A., Lai, F. W., Siddique, J., Zahid, M., & Ali, S. E. A. (2023). A walk of corporate sustainability towards sustainable development: A bibliometric analysis of literature from 2005 to 2021. Environmental Science and Pollution Research, 30(13), 36521–36532.

Jilani, M. M. A. K., Fan, L., Islam, M. T., & Uddin, M. A. (2020). The influence of knowledge sharing on sustainable performance: A moderated mediation study. Sustainability, 12(3), 908. https://doi.org/10.3390/su12030908

Jog, D., & Singhal, D. (2020). Greenwashing understanding among Indian consumers and its impact on their green consumption. Global Business Review, 1–21. https://doi.org/10.1177/0972150920962933

Johnson, L., & Patel, M. (2024). Navigating sustainability challenges: Lessons from global leaders. Sustainability Leadership Review, 18(3), 120–136.

Kamble, S., Gunasekaran, A., & Dhone, N. C. (2019). Industry 4.0 and lean manufacturing practices for sustainable organisational performance in Indian manufacturing companies. International Journal of Production Research, 58(5), 1319–1337. https://doi.org/10.1080/00207543.2019.1630772

Khan, N. U., Wu, W., Saufi, R. B. A., Sabri, N. A. A., & Shah, A. A. (2021). Antecedents of sustainable performance in manufacturing organizations: A structural equation modeling approach. Sustainability, 13(2), 897. https://doi.org/10.3390/su13020897

Kucukoglu, M. T., & Pinar, R. I. (2015). Positive influences of green innovation on company performance. Procedia—Social and Behavioral Sciences, 195, 1232–1237. https://doi.org/10.1016/j.sbspro.2015.06.261

Kularatne, T., Wilson, C., Månsson, J., Hoang, V., & Lee, B. (2019). Do environmentally sustainable practices make hotels more efficient? A study of major hotels in Sri Lanka. Tourism Management, 71, 213–225. https://doi.org/10.1016/j.tourman.2018.09.009

Kumar, R., & Gupta, S. (2022). Sustainability practices in Indian businesses: Trends and challenges. Indian Journal of Sustainability Management, 9(1), 56–72.

Lattimore, B., Smith, C. T., Titus, B. D., Stupak, I., & Egnell, G. (2009). Environmental factors in wood fuel production: Opportunities, risks, and criteria and indicators for sustainable practices. Biomass and Bioenergy, 33(10), 1321–1342. https://doi.org/10.1016/j.biombioe.2009.06.005

Lèbre, É., Corder, G. D., & Golev, A. (2017). Sustainable practices in the management of mining waste: A focus on the mineral resource. Minerals Engineering, 107, 34–42. https://doi.org/10.1016/j.mineng.2016.12.004

Maleti?, M., Maleti?, D., Dahlgaard, J. J., Dahlgaard-Park, S., & Gomiscek, B. (2015). Do corporate sustainability practices enhance organizational economic performance? International Journal of Quality and Service Sciences, 7(2–3), 184–200.

Maleti?, M., Maleti?, D., Dahlgaard, J. J., Dahlgaard-Park, S. M., & Gomiš?ek, B. (2016). Effect of sustainability-oriented innovation practices on the overall organisational performance: An empirical examination. Total Quality Management and Business Excellence, 27(9–10), 1171–1190. https://doi.org/10.1080/14783363.2015.1064767

McKinsey. (2010). McKinsey global institute report. https://www.mckinsey.com/~/media/

Meseguer-Sánchez, V., Gálvez-Sánchez, F. J., López-Martínez, G., & Molina-Moreno, V. (2021). Corporate social responsibility and sustainability. A bibliometric analysis of their interrelations. Sustainability, 13(4), 1636.

Mousa, S. K., & Othman, M. (2020). The impact of green human resource management practices on sustainable performance in healthcare organisations: A conceptual framework. Journal of Cleaner Production, 243, 118595. https://doi.org/10.1016/j.jclepro.2019.118595

Nobanee, H., Al Hamadi, F. Y., Abdulaziz, F. A., Abukarsh, L. S., Alqahtani, A. F., AlSubaey, S. K., Alqahtani, S. M., & Almansoori, H. A. (2021). A bibliometric analysis of sustainability and risk management. Sustainability, 13(6), 3277.

Ogutu, H., El Archi, Y., & Dénes Dávid, L. (2023). Current trends in sustainable organization management: A bibliometric analysis. Oeconomia Copernicana, 14(1), 11–45.

Paillé, P., Chen, Y., Boiral, O., & Jin, J. (2014). The impact of human resource management on environmental performance: An employee-level study. Journal of Business Ethics, 121(3), 451–466. https://doi.org/10.1007/s10551-013-1732-0

Pan, L., Xu, Z., & Skare, M. (2023). Sustainable business model innovation literature: A bibliometrics analysis. Review of Managerial Science, 17(3), 757–785.

Park, S. B., Kim, J., Lee, Y. K., & Ok, C. M. (2020). Visualizing theme park visitors’ emotions using social media analytics and geospatial analytics. Tourism Management, 80, 104127. https://doi.org/10.1016/j.tourman.2020.104127

Patel, A., & Desai, P. (2023). ESG considerations in Indian supply chains: Challenges and opportunities. Supply Chain Management Review, 15(2), 78–92.

Pradhan, R. K., Jena, L. K., & Panigrahy, N. P. (2020). Do sustainability practices buffer the impact of self-efficacy on organisational citizenship behaviour? Conceptual and statistical considerations. Journal of Indian Business Research, 12(4), 509–528. https://doi.org/10.1108/JIBR-05-2019-0170

Reddy, S., & Singh, M. (2024). Towards sustainable finance: Role of ESG integration in Indian capital markets. Indian Journal of Finance and Sustainable Development, 8(3), 112–128.

Rennings, K., Ziegler, A., Ankele, K., & Hoffmann, E. (2006). The influence of different characteristics of the EU environmental management and auditing scheme on technical environmental innovations and economic performance. Ecological Economics, 57(1), 45–59, https://doi.org/10.1016/j.ecolecon.2005.03.013

Roscoe, S., Subramanian, N., Jabbour, C. J. C., & Chong, T. (2019). Green human resource management and the enablers of green organisational culture: Enhancing a firm’s environmental performance for sustainable development. Business Strategy and the Environment, 28(5), 737–749. https://doi.org/10.1002/bse.2277

Sajan, M. P., Shalij, P. R., Ramesh, A., & Biju, A. (2017). Lean manufacturing practices in Indian manufacturing SMEs and their effect on sustainability performance. Journal of Manufacturing Technology Management, 28. https://doi.org/10.1108/JMTM-12-2016-0188

Santos, C., Coelho, A., & Marques, A. (2023). A systematic literature review on greenwashing and its relationship to stakeholders: State of art and future research agenda. Management Review Quarterly. https://doi.org/10.1007/s11301-023-00337-5

Sensharma, S., Sinha, M & Sharma, D. (2022). Do Indian firms engage in greenwashing? Australasian Accounting Business and Finance Journal, 16(5), 67–88.

Shahzad, M., Qu, Y., Zafar, A. U., Rehman, S. U., & Islam, T. (2020). Exploring the influence of knowledge management process on corporate sustainable performance through green innovation. Journal of Knowledge Management, 24(9), 2079–2106. https://doi.org/10.1108/JKM-11-2019-0624

Sharma, A., & Kumar, N. (2021). Enhancing ESG disclosure practices: A roadmap for Indian corporates. Journal of Corporate Governance and Ethics, 7(2), 145–160.

Sharma, A., & Singh, N. (2021). Towards sustainable business models: Perspectives from Indian enterprises. Journal of Corporate Sustainability, 8(2), 75–90.

Sheng, J., Sinha, A., Mansoor, S., & Zafar, M. W. (2024, March). Greening the energy future: Role of energy innovation as policy driver. Natural resources forum. Blackwell Publishing Ltd.

Sheoran, M., & Kumar, D. (2022). Conceptualisation of sustainable consumer behaviour: Converging the theory of planned behaviour and consumption cycle. Qualitative Research in Organizations and Management: An International Journal, 17(1), 103–135.

Shove, E., & Spurling, N. (2013). Sustainable practices: Social theory and climate change. Sustainable practices (pp. 1–13). Routledge.

Simpson, D., & Samson, D. (2010). Environmental strategy and low waste operations: Exploring complementarities. Business Strategy and the Environment, 19(2), 104–118. https://doi.org/10.1002/bse.626

Smith, E. E., & Muller, R. J. (2016). Creating a culture of sustainability in organisations in Nelson Mandela Bay. In Managing in resource restricted times make every day matter. Proceedings of the 28th annual conference of the Southern African Institute of Management Scientists (pp. 72–87).

Smith, J., & Jones, A. (2023). The business case for sustainability: Insights from global corporations. Journal of Sustainable Business, 12(2), 89–104.

Statista. (2021). Attitude towards sustainability. Consumer insights sustainable consumption. https://www.statista.com/global-consumer-survey/tool/30/sus_ind_202100?bars=1&index=0&absolute=0&missing=0&heatmap=0&rows%5B0%5D=v0602_mind_attitudes&tgeditor=0&pendo=0

Sustainalytics. (2022). The Morningstar Sustainalytics corporate ESG survey report 2022. https://www.sustainalytics.com/corporate-esg-survey-report?utm_campaign=scs_content_global_2210_surveyreport_en&utm_medium=email&utm_content=scs_global_em2_221104_follow-up-email_en&utm_source=email

Tang, M., Liao, H., Wan, Z., Herrera-Viedma, E., & Rosen, M. A. (2018). Ten years of sustainability (2009 to 2018): A bibliometric overview. Sustainability, 10(5), 1655.

Townsend, T. G., Powell, J., Jain, P., Xu, Q., Tolaymat, T., & Reinhart, D. (2015). Sustainable practices for landfill design and operation. Springer.

Trivedi, S. K., Singh, A., Irfan, M., Harigaran, T., & Patra, P. (2024). Energy transition, the next hotspot of energy research: A study using topic modeling. IEEE transactions on engineering management. (pp. 1–44). https://doi.org/10.1109/TEM.2024.3368153

United Nations. (2023). https://www.un.org/en/desa/india-overtake-china-world-most-populous-country-april-2023-united-nations projects#:~:text=24%20April%202023% 20%2D%20China%20will,the%20population%20of%20mainland%20China

Wang, C. J. (2014). Do ethical and sustainable practices matter? Effects of corporate citizenship on business performance in the hospitality industry. International Journal of Contemporary Hospitality Management, 26(6), 930–947. https://doi.org/10.1108/IJCHM-01-2013-0001

Yong, J. Y., Yusliza, M. Y., Ramayah, T., Chiappetta Jabbour, C. J., Sehnem, S., & Mani, V. (2020). Pathways towards sustainability in manufacturing organizations: Empirical evidence on the role of green human resource management. Business Strategy and the Environment, 29(1), 212–228. https://doi.org/10.1002/bse.2359

Young, W., & Tilley, F. (2006). Can businesses move beyond efficiency? The shift toward effectiveness and equity in the corporate sustainability debate. Business Strategy and the Environment, 15(6), 402–415. https://doi.org/10.1002/bse.510

Yusliza, M. Y., Yong, J. Y., Tanveer, M. I., Ramayah, T., Noor Faezah, J. N., & Muhammad, Z. (2020). A structural model of the impact of green intellectual capital on sustainable performance. Journal of Cleaner Production, 249, 119334. https://doi.org/10.1016/j.jclepro.2019.119334