IIMS Journal of Management Science

Search

Search

Samson Edo1

1 Department of Economics, University of Benin, Benin City, Nigeria

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.`

This study investigates how digital payment affects industrial sector activity in selected Sub-Saharan African countries. The selected countries are Nigeria and South Africa, which are the largest economies in the sub-region with rapid adoption of digital payment. The investigation is motivated by the strategic importance of the payment system in facilitating industrial production and turnover. The methodologies of unrestricted error correction model (UECM) and dynamic ordinary least squares model (DOLS) are employed in the study. The UECM results show that the adoption of digital payment impacted significantly on industrial sector activity in both countries. The impact is, however, lower than the impact of physical capital, human capital, and personal income. The positive role of digital payment is, therefore, strongly complemented by the three variables. On the other hand, trade openness has an insignificant effect, which indicates a relatively weak role in facilitating industrial activity. The DOLS results are not significantly different from the UECM results, which indicates that the estimated impacts on industrial activity are consistent. The findings suggest the need to deepen the digital payment system, in order to sustain its role in industrial production and expansion. This could be done by strengthening the internet technology that is used in digital payment. Furthermore, the role of physical and human capital needs to be sustained by encouraging capital investment, while that of personal income may be sustained by reducing income tax. The low effect of trade openness could be improved by controlling the import of industrial goods.

Digital payment, industrial activity, policy analysis, developing economies

Introduction

Financial transactions in developing countries are predominantly based on cash payments. However, the evolution of digital payment has significantly reduced dependence on cash payment, which seems to have influenced the level of industrial activity in most developing economies, particularly in Sub-Saharan Africa. The increasing adoption of digital payment in these countries reflects the perception that it has some economic advantages over cash payment. Indeed, it is argued that digital mode of payment tends to encourage activity in various sectors of the economy (Chen & Xie, 2019). It also facilitates international transactions and inflows of foreign investment to different sectors of the economy, leading to faster growth. Over the last decade, some countries in Sub-Saharan Africa, have witnessed a considerable shift from cash payment to digital payment, following the implementation of digital payment policy. However, the effect of this shift on industrial activity has remained a contentious issue.

Some economists argue that digital payment promote industrial activity by increasing product turnover. Furthermore, industrial activity is encouraged as foreigner can easily transfer funds to buy products of domestic industries. This view is supported by Li and Liu (2005) and Vertakova et al. (2015), who posited that such foreign transactions promote the growth of industries, directly and indirectly, through an increase in production and export of industrial goods. Some economists, on the other hand, hold the view that digital payment encourages foreign buyers of domestic manufactures, which may only have short-term positive effect on industrial activity. In support of this argument, Aga (2014) and Pandya and Sisombat (2017) posited that digital payment system that is not secured may discourage foreign buyers and slow industrial sector activity in the long run.

In spite of the contentions revolving around the role of digital payment, it is largely considered to be a potential driving force of industrial sector activity in developing countries. However, it is not yet clear whether this assertion holds true in the two leading economies of Sub-Saharan Africa, namely, Nigeria and South Africa. This study, therefore, attempts to investigate the role of digital payment in facilitating industrial sector activity and its policy implications in the selected countries. More precisely, the study aims to determine the short-run and long-run effects of digital payment on industrial sector activity. This issue has yet to be given adequate attention in empirical studies of Sub-Saharan African countries. The two countries under investigation have witnessed rapid adoption of digital payment over the period 2012–2022. In Nigeria, which is the largest economy in Sub-Saharan Africa, the volume of digital payment rose astronomically from 428.2 million in 2012, to about 25.13 billion in 2022 (Nigeria Bureau of Statistics, 2022). Similarly, South Africa, which is the second largest economy in Africa, witnessed tremendous increase in volume from 117.22 million in 2018, to about 8.39 billion in 2022 (International Trade Administration, 2023). Other countries have also witnessed the same phenomenon, but data are not yet available to investigate them.

The investigation is carried out by employing the unrestricted error correction model (UECM) and the dynamic ordinary least squares model (DOLS). In terms of scope, the study covers the period 2012Q1–2022Q4. It is structured into six sections comprising an introduction, literature review, empirical methodology, empirical results, policy implications and imperatives, and conclusion.

Literature Review

The theoretical literature on industrial sector activity draws heavily from the neoclassical and endogenous theories of growth (Grossman & Helpman, 1990; Romer, 1990; Solow, 1956; Swan, 1956), which relate production activity to physical and human capital. Therefore, physical and human capital form the basic factors in the theory of industrial sector activity (Kiely, 1994). However, there were concerns that these factors alone do not adequately explain industrial activity, which led to further extensions of the theory (Rahman, 2010; Sugihara, 2019). One such extension was propounded by Banerjee (2000), which links industrial sector activity to the state of the capital market. According to the theory, if the capital market is underdeveloped and unable to mobilize long-term funds, industrial sector activity remains low. In this situation, opportunities with high returns may abound for industries, but inadequate resources become a major constraint to expansion (Legros & Newman, 1995). Industries would, therefore, be characterized by slow growth. On the other hand, when the capital market is fairly well developed and able to mobilize long-term funds for industries, there would be rapid growth in activity, as well as sustainable development in the industrial sector (Morduch, 1990).

Another extension of the theory emphasized the important role of government in facilitating industrial growth (Tongxina et al., 2011). This model is derived from the Japanese experience that positively relates industrial performance to a policy environment that promotes market forces and competition. This model has remained the main attraction for developing countries aspiring to achieve rapid industrial growth similar to that of Japan and China. Furthermore, Worku (2010) posited that electronic payment drives industrial activity by lowering the cost of business.

The empirical aspect of industrial sector activity presents a considerable array of studies on its determinants, but not much has been done on the role of digital payment. However, Saroy et al. (2023) only investigated the role in the banking sector of India within the period 2011–2019, using data envelopment analysis and dynamic panel data methods. The empirical results showed that greater adoption of digital payment improved cost efficiency but not technical efficiency. This differentiated impact is attributed to a reduction in operational expenses without reducing the level of inputs. Similarly, Kasri et al. (2022) investigated the impact of digital payment on the banking system in Indonesia over the period 2013–2021, using the vector error correction model (VECM) and vector autoregressive model (VAR). The study found that digital payment transactions had a positive long-run relationship with banking stability. Furthermore, it was discovered that digital payment had unidirectional causality on banking stability. Past empirical studies on industrial activity seem to have focused more on other factors affecting the activity. Yang et al. (2021) analysed the transformation of the manufacturing industry of Hong Kong during the period 2008–2018, to determine the factors responsible for the phenomenon. After a careful investigation, it was discovered that technological innovation, scale agglomeration, and market demand were the major drivers, which suggests that appropriate policies are needed to sustain these factors. In a previous study, Vertakova et al. (2015) observed that membership of the World Trade Organization changed the composition of factors influencing industrial activity in Russia. It led to market competitiveness, reduction in state control, increase in cross-border investments, and improvement in credit to the private sector. All these changes caused appreciable growth of the industrial sector, characterized by new technologies and improved product quality. The drivers of industrial production in developing countries were again investigated in a study by Martorano et al. (2017), for two different periods of 1970–1990 and 1991–2014. The countries investigated were selected based on their pattern of industrialization that was considered quite remarkable and sustained over a long period of time. The empirical results revealed that production was driven by a combination of factors including country initial conditions, resource endowments, and geographical location. Other variables that influenced production include investment promotion, openness of the economy, financial development, as well as macroeconomic and institutional stability.

Singh and Kumar (2021) used state-wise panel data to examine the factors affecting industries in India, within the period 2003–2018. The linear, log-linear, and non-linear models were employed in estimating the effects, which revealed that capital formation, credit to economy, and literacy rate, were the strong drivers of growth in industrial sector activity. A previous study of Saudi Arabia by Ali (2020) revealed that the country witnessed rapid expansion in industrial sector within four decades, due to an enabling business environment. The study, however, concluded that there are small manufacturing industries in the country that should be given more attention to achieve substantial growth. It went further to recommend easy credit and technical assistance for the small manufacturing industries. Engidaw (2021) used a different approach to study the effect of country-level factors on micro and small enterprises in Ethiopia, by employing a framework of stratified and random sampling. It revealed a positive relationship between the factors and growth of the enterprises. More precisely, market demand, financial development, and infrastructure had significant positive effect on the level of activity. Among these variables, infrastructure had the most significant effect, hence the study recommended that more policy attention should be given to provision of infrastructure.

Global value chain (GVC) is also considered to be important in explaining growth in industrial sector activity across countries. Kummritz (2016) provided evidence on the role by using inter-country input-output tables, which revealed that participation in GVC led to higher productivity of industries in all the countries, independent of income levels. More specifically, the study revealed that 1% increase in participation led to 0.11% rise in value-added and 0.33% rise in labor productivity. In a more recent study of industries in Ethiopia, Whitfield et al. (2020) examined the benefits of GVC participation to manufacturing industries in Ethiopia. Generally, it was discovered that participation in GVC did not significantly improve the level of activity in manufacturing industries, due to the fact that industrial policy in the country favored domestic linkages more than global linkages.

Some studies in developing countries have also investigated the role of foreign direct investment (FDI) in industries. In a study conducted by Mishra et al. (2001), 1% increase in foreign investment to Africa was found to boost manufacturing activity by more than 5%, which is considered remarkable in a continent that is characterized by political instability and unfavorable investment climate. Further evidence from cross-country regression by Iamsiroroj and Ulubasoglu (2015), covering selected developing countries, revealed that FDI accelerated growth in industrial sector, especially in countries with a large pool of skilled labor. In these countries, the foreign investments in industries, which were largely channeled through the domestic capital market, led to significant increase in industrial turnover. The capital market was able to sustain the flow of foreign investments to industries, due to its resilience and capacity to hold industries accountable for invested funds. The capital market has been a major player in safeguarding industrial investment, in order to avoid financial crises that may occur due to mismanagement. Such crises have indeed occurred in some countries that opened up their economies to foreign capital (Hausman & Fernandez-Arias, 2000).

Samantha and Liu (2018) again investigated how inflow of foreign investments affected industries in Sri Lanka during the period of economic liberalization (1980–2016), using the autoregressive distributed lag model. The study found insignificant relationship in the short-run and long-run. It concluded that government policy should be focused on attracting more foreign investments with advanced technology capable of increasing industrial productivity. In another study, Inada (2013) examined the effect of foreign investment on industries in China, following the lifting of restriction on entry of foreign affiliates in 2002. The study used industry-level panel data, and found that the industries experienced a significantly larger turnover and export volume. It was also discovered that foreign investment significantly increased productivity of the industries, far beyond the level achieved before 2002.

In a recent study, Adejumo (2020) used Granger causality test to determine the effect of FDI on the manufacturing industries in Nigeria, under regulated and deregulated economic regimes of the period 1970–2015. It was discovered that the causality is unidirectional from FDI to manufacturing output and export, which supports the view that FDI is a strong determinant of industrial activity. The results, therefore, suggest that FDI is a strategic factor that needs adequate policy attention, in order to achieve rapid industrial sector growth in Nigeria, and indeed, other similar countries. This prescription was also made in an earlier study by Samouel and Aram (2016), underscoring the need for developing countries to formulate viable policies that can attract more FDI that would enhance industrial sector growth. Akpan and Eweke (2017) used VAR method to study the effect of FDI on industrial performance in Nigeria, during the period 1981–2015. It was revealed that FDI and industrial sector growth have a bidirectional causality, suggesting that they positively affect each other. The results, therefore, support the case that FDI significantly affects industrial growth.

So far, empirical studies have attributed growth in industrial sector activity to several factors. However, no study has given adequate attention to the role of digital payment in facilitating growth of industrial sector activity in Sub-Saharan African countries, thus creating a void in existing literature. It is, therefore, important to undertake study that would determine this role and its policy implications in typical Sub-Saharan African countries.

Empirical Methodology

Theoretical Modeling

The neoclassical and endogenous theories of growth emphasize the importance of physical and human capital in facilitating economic activity. It is hypothesized that increase in capital investment leads to expansion of activity in various sectors of the economy. However, it has been discovered that capital investment alone does not determine the level of industrial sector activity, hence Banerjee (2000) and Tongxina et al. (2011) proposed alternative explanations that focused on the role of capital market and policy environment. Furthermore, Worku (2010) proposed an explanation that focused on the important role of payment system in facilitating industrial sector activity. More precisely, electronic payment is posited to have lower cost that encourages industries to grow. This present study takes into consideration the key factors affecting industrial sector activity, with particular focus on the payment system. The payment system has short-run and long-run effects on industrial sector activity.

The model relating industrial sector activity to the various factors may, therefore, be presented in the form of UECM and DOLS. The UECM model is employed because it possesses the capacity to eliminate the problem of endogeneity, and also suitable for estimating both short-run and long-run effects. The model may be derived from the basic framework presented below:

(1)

(1)

(2)

(2)

The framework shows the functional relationships between industrial sector activity and the exogenous variables in (1), with the empirical version stated in (2). The endogenous variable is IDPt (industrial sector activity), while the exogenous variables are DPt (digital payment), PKt (physical capital), HKt (human capital), PYt (personal income), and TT (trade openness). The parameters αj and μit represent impact and error term, respectively. The framework is transformed to the unrestricted VECM, as shown below:

(3)

(3)

(4)

(4)

Where,

IDPt = industrial sector activity (endogenous variable)

Zt – 1 = vector of lagged exogenous variables (j = 1, 2, …., 6)

.png) = first difference operator

= first difference operator

αj = long-run coefficients of exogenous variables

λi = short-run coefficients of exogenous variables.

The model shows that industrial activity depends on five underlying variables, and the lagged endogenous variable as indicated in equation (3), in conformity with the theoretical requirements of UECM. On the other hand, equation (4) indicates the short-run and long-run relationships between industrial activity and the variables. The parameters αj (j = 1, 2, ……., 6) represent long-run coefficients of the exogenous variables, while λj (j = 1, 2, . …., 6) are short-run coefficients.

The DOLS model is also constructed to support the UECM model, in order to ensure consistent and dependable estimation results. It is a dynamic equation model commonly estimated to determine the long-run relationship between endogenous and exogenous variables, with the advantage of eliminating the problem of endogeneity (Stock & Watson, 1993). The model in its reduced form is presented in (5). It is made dynamic in (6) by introducing leads and lags. The leads and lags are introduced to minimize serial correlation and correct for endogeneity.

.png/10_1177_0976030X241250105-eq5(1)__177x27.png) (5)

(5)

(6)

(6)

Where,

IDPt = industrial sector activity (endogenous variable)

Xt = vector of exogenous variables (j = 1, 2, …., 5)

.png) j = coefficients of exogenous variables

j = coefficients of exogenous variables

The model simply relates industrial activity (IDPt) to digital payment (DPt), physical capital (PKt), human capital (HKt), personal income (PYt), and trade openness (TTt).

Basic Concepts in the Model

Industrial Activity

This concept refers to a specific branch of economic activity involving production or manufacturing of goods, and provision of services. It encompasses activities by firms engaged in offering similar or different products. These activities are characterized by their unique features, which include product type, technology, and the market they serve. Industrial activity is governed by a set of regulations, and takes place in a competitive environment. Manufacturing represents the major hub of industrial activity. According to International Labor Organization (2023), the other components of industrial activity include construction, mining, electricity, gas, water supply, services, etc. Before the advent of Covid-19, China led the world in manufacturing with over $2.01 trillion output (West & Lansang, 2018), followed by the United States ($1.87 trillion), Japan ($1.06 trillion), Germany ($700 billion), and South Korea ($372 billion). Overall, China, United States, and Japan contributed about 48% of world manufacturing output. The Covid-19 pandemic disrupted manufacturing activity regionally and globally, as manufacturing export of China and Japan dropped by over 17.8% in 2020, but the export of US increase slightly by 0.7% (Chinaorgcn, 2023). However, China was able recover quickly in 2021 and increased manufacturing export by 6.7% to retain its leadership position among the five top manufacturing countries in the world (Kansas City Fed, 2023). According to Safeguard Global (2023), China contributed 28.4% of world manufacturing output in 2023, followed by the United States (16.6%), Japan (7.5%), Germany (5.8%), and India (3.3%). India has made spectacular progress in manufacturing by climbing to the fifth position among world industrial countries.

Digital Payment

This system of payment involves electronic transfer of money from one account to another using digital devices. The system encompasses payment methods that use digital channels, such as the internet, mobile phones, and automated devices to transmit and receive money. The instruments of transfer include mobile bank applications, credit and debit cards, prepaid cards, etc. Digital payment can be described as primary, partial, or full. Primary digital payment enables the payer to transfer money directly to account of the payee who then withdraws the cash from the account. Partial digital payment allows the payer to transfer money to the account of a third-party agent who receives the payment and disburse cash to the payee. Full digital payment is one in which the payer transfers cash to the payee who receives it digitally and also spends it digitally. Digital payment offers significant benefits to individuals, firms, governments, and international organizations. The system of digital payment has evolved rapidly over the last two decades, with the introduction of different modes of transactions, such as point of sale transfer, online sales transfer, automated teller machine transfer, automated clearing house transfer, digital wallet transfer, etc. It has also expanded rapidly to cover transactions within countries and across borders. The expansion is facilitated by increasing proliferation of smartphones and consumer adaptation to digital technology. It is anticipated that the digital payment system will continue to witness rapid growth in developing countries, particularly India and Indonesia, where smartphones are increasingly encroaching on rural areas due to government push for digital driven economy. The unified payment interface, digital India, and the introduction of helpline 14444 are a few initiatives the Indian government has launched to support digital payment system. These initiatives helped in positioning India as the country with the highest digital transactions in the world, accounting for about 46%, as at 2022. India is followed by Brazil, China, Thailand, and South Korea (Unified Payments Interface, 2023). In general, the Asia-Pacific region leads other regions of the world in the digital payment transactions.

Estimation Techniques

The UECM methodology is employed in determining the effect of exogenous variables on industrial activity in each country, following Aliyu and Ismail (2017) and Hussain (2007). The methodology allows each variable to adjust and minimize the endogeneity problem. The DOLS methodology is also employed to determine the effects. It is a dynamic equation technique that corrects for endogeneity and serial correlation by including leads and lags of exogenous variables. The leads and lags ensure that the model accounts fully for changes in industrial activity. These techniques of UECM and DOLS are employed in this study because of their ability to minimize serial correlation and endogeneity problem. They are preferred to the basic and less complex methodologies of error correction mechanism and ordinary least squares, due to their capacity that allows estimation to be done without imposing restrictions of linearity or nonlinearity. The lack of restriction, therefore, makes them more suitable in empirical studies.

The data employed in estimation are index of industrial production (industrial sector activity), volume of electronic money transfers (digital payment), gross fixed capital formation (physical capital), adult literacy rate (human capital), disposable income (personal income), and ratio of import and export to GDP (trade openness).

Empirical Results

Model Estimation Results

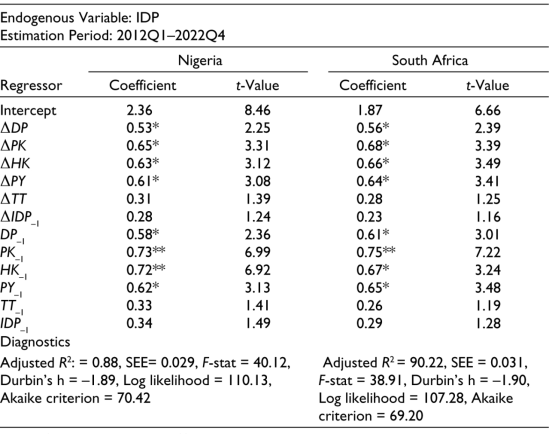

The estimation results of the UECM are reported in Table 1. In Nigeria, the short-run and long-run effects of digital payment are 0.53 and 0.58, respectively, which are significant at the 5% level. The results, therefore, suggest that digital payment had appreciable effect on industrial activity in Nigeria. However, these effects are lower than the effects of physical capital and human capital, which are above 0.64 and significant at 5%. Personal income also produced significant effect of over 0.60, which exceeds the effect of digital payment. It is only trade openness that had insignificant effects lower than 0.34. The response of industrial activity to its own lag is indicated by the coefficient of IDP–1, which is below 0.35, suggesting that current activity does not significantly depend on past level of activity. In South Africa, the results are not significantly different from Nigeria. The short-run and long-run impacts of digital payment (0.56 and 0.61) are significant at 5%. It follows that digital payment-enhanced industrial activity, as much as it deed in Nigeria. Physical capital and human capital had more significant impact of over 0.65, while personal income also exerted more significant impact of over 0.63. The impact of trade openness falls below 0.30 and insignificant at 5%, making it the only variable with unimpressive impact. The response of current industrial activity to the past level of activity is below 0.30, which is also insignificant.

Table 1. Unrestricted Error Correction Model Estimation Results.

Notes: * Significant at 5% level, **Significant at 1% level; IDP––industrial activity, DP––to digital payment, PK––physical capital, HK––human capital, PY––personal income, TT––trade openness; the first difference operator D attached to the variables indicates short-run, while the variables without the operator indicate long-run.

In summary, the results show that industrial activity in both countries benefited appreciably from digital payment, which was largely complemented by some of the control variables. The diagnostics show that estimation errors are highly minimized, which makes the estimation results robust and reliable. The extent to which the benefits can be sustained depends on the policy direction of the countries.

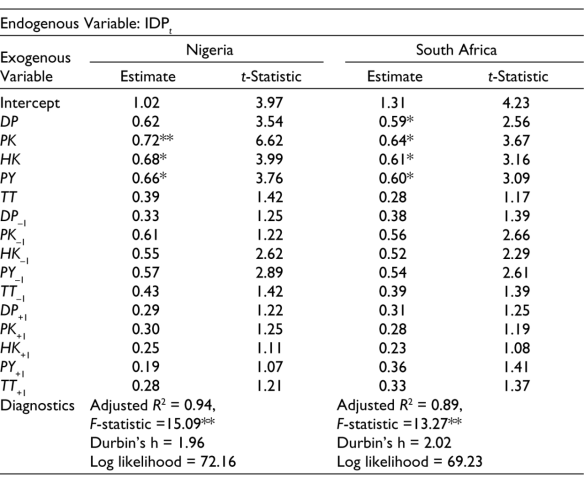

The DOLS model was also estimated to back up the UECM estimation and ensure dependability of results. The DOLS results are reported in Table 2 for the two countries. In Nigeria, digital payment had significant long-run impact of 0.62 on industrial activity, at the 5% level, which is, however, surpassed by physical capital (0.72), human capital (0.68), and personal income (0.66). Trade openness is the only exogenous variable that had insignificant impact of 0.39. In South Africa, the impact of digital payment is observed to be 0.59, is also lower than the impact physical capital (0.64), human capital (0.61), and personal income (0.60). The only variable with insignificant effect is trade openness (0.28). The results are similar to the estimates produced by the UECM model, and clearly suggests that digital payment played appreciable role in facilitating industrial activity in both countries, which was strongly complemented by physical capital, human capital, and personal income.

Table 2. Dynamic Ordinary Least Squares Estimation Results.

Notes: * Significant at the 5% level; ** Significant at the 1% level; Leads and lags = 1.

IDP––industrial activity, DP––to digital payment, PK––physical capital, HK––human capital, PY––personal income, TT––trade openness; the variables with leads and lags are only included to minimize the problem of endogeneity in estimation.

The lags and leads are all positive in both countries, thus minimizing the endogeneity problem in estimation. Also, the adjusted coefficients of R2 (0.94, 0.89) indicate that all the variables were able to account for 94% of systemic change in Nigeria, and 89% of systemic change in South Africa. The overall impact of variables is significant at 1% in both countries, as indicated by the F-statistics (15.09, 13.27). The Durbin’s h values (1.96, 2.02) and log-likelihood values (72.16, 69.23) show that serial correlation is highly minimized, thus making the estimated results unbiased and reliable.

To ensure that the variables in each country are stationary, unit root test is conducted on the residuals of DOLS regression, by using the PP technique proposed by Phillips and Perron (1988). The results, reported in Table 3, show that the residuals are non-stationary in levels for both countries, as indicated by the insignificant test statistics. However, the statistics are significant in first differences, hence the null hypothesis that variables are non-stationary is rejected, which makes the estimation results non-spurious.

Table 3. Unit Root Test Results on Residuals of DOLS Regression.

Note: *Significant at the 5% level; Phillips-Perron test.

Forecasting Capacity of Estimated Model

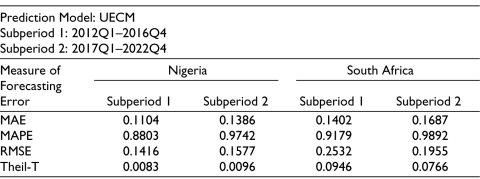

The forecasting capacity is tested by using UECM estimation results. This is done by splitting the study period into two approximately equal subperiods. The data for each subperiod is fitted into the estimated UECM model to produce forecast errors in the two subperiods, which are then evaluated to determine the forecasting capacity. For a model to have good forecasts, the errors in the two subperiods should be similar. This procedure has been adopted in several studies, such as Otavio et al. (2011), Jiang and Liu (2011), Kuo (2016), etc. In Table 4, all the measures of forecast error have values less than unity, indicating that the errors are negligible in both countries. The forecasting capacity of the estimated model can, therefore, be considered quite good, which makes the model reliable for short-run forecasts of industrial activity.

Table 4. Results of Forecasting Test.

Note: MAE––Mean absolute error, MAPE––Mean absolute prediction error, RMSE––root mean square error, Theil-T––Theil’s coefficient of inequality.

Structural Stability

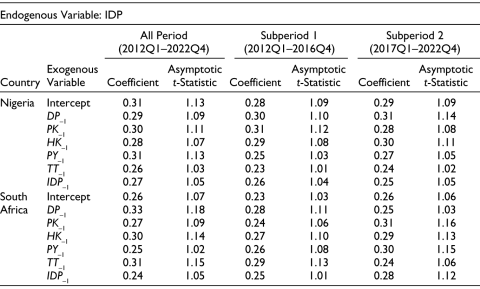

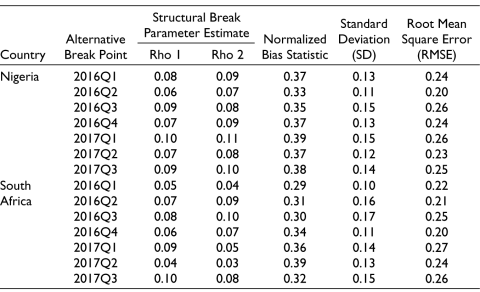

The empirical results have shown how industrial activity is affected by digital payment and other variables. It is, therefore, possible to use the estimates as a basis for policymaking. However, the results can only be considered useful for policymaking if structural stability exists within the model. The maximum likelihood estimator is employed to test for stability, which involves splitting the entire period of study into two subperiods, by choosing a suitable breakpoint (Yu et al., 2008). The breakpoint, as shown in Table 5, is the period 2016Q4, which was characterized by economic disturbance in Nigeria and South Africa due to the downturn in global oil market. The table reports maximum likelihood estimates of the whole period and subperiods, which are not significant at 5%. Again, the subperiod estimates of each variable are not significantly different. The test, therefore, indicates acceptance of the null hypothesis of no structural instability, hence the estimated results may be considered suitable for policy making. In Table 6, the insignificant variation in values Rho, normalized bias statistic, standard deviation, and root mean square error, indicate that the stability test results are unbiased and reliable.

Table 5. Maximum Likelihood Structural Stability Estimates.

Note: IDP––industrial production, DP––digital payment, PK––physical capital, HK––human capital, PY––purchasing power, TT––trade openness.

Table 6. Maximum Likelihood Reliability Estimates.

Note: Alternative breakpoints are distributed evenly around the period 2016Q4.

Policy Implications and Imperatives

In both countries, the UECM estimation produced results that reveal significant short-run and long-run effects of digital payment on industrial activity. The DOLS estimation results are largely similar to the long-run effects of UECM. The significant role of digital payment was strongly complemented by physical capital, human capital, and personal income, while trade openness played an insignificant role. These findings, therefore, have some useful policy implications:

Conclusion

In this study, an investigation was undertaken to determine the role of digital payment in fostering industrial sector activity in key Sub-Saharan African economies, during the period 2012Q1–2022Q4. The study adds to the growing research works on industrial activity in emerging countries. The methodologies of UECM and DOLS were employed to investigate the issue. The estimation results of UECM and DOLS, which are not significantly different revealed that:

The forecasting capacity of estimated model was tested by using UECM estimation results, which produced negligible forecast errors. It shows that the model possesses a good forecasting capacity, and is reliable for predicting short-run trends in industrial activity. The test of stability also revealed no significant structural break, hence the estimated model may be considered suitable for policy making. These findings, therefore, suggest that:

Declaration of Conflicting Interest

The authors declared no potential conflicts of interest concerning the research, authorship, and/or publication of this article.

Funding

This research did not receive any specific grant from funding agencies in the public, commercial, or not for profit sectors.

ORCID iD

Samson Edo https://orcid.org/0000-0002-8238-8576

Adejumo, A. V. (2020). Foreign direct investment-led industrialization: Any direction for spillovers in Nigeria? Journal of Co-operative and Business Studies, 5(1), 14–43.

Aga, A. K. (2014). The impact of foreign direct investment on economic growth: A case study of Turkey 1980–2012. International Journal of Economics and Finance, 6(7), 71–84.

Akpan, E. S., & Eweke G. O. (2017). Foreign direct investment and industrial sector performance: Assessing the long-run implication on economic growth in Nigeria. Journal of Mathematical Finance, 7(2), 391–411.

Ali, A. (2020). Industrial development in Saudi Arabia: Disparity in growth and development. Problems and Perspectives in Management, 18(2), 23–35.

Aliyu, A. J., & Ismail N. M. (2017). Food imports and exchange rate: The application of dynamic cointegration framework. Malaysian Journal of Mathematical Sciences, 11(2), 101–114.

Banerjee, A. V. (2000). Notes toward a theory of industrialization in developing world. In N. Banerjee & S. Marjit (Eds), Development, displacement and disparity (pp. 139–159). Orient Longman.

Chen, J., & Xie, I. (2019). Industrial policy, structural transformation and economic growth: Evidence from China. Frontiers of Business Research in China, 13(4), 18–29.

China.org.cn. (2023). Covid-19 impact on China’s industries. https://www.china.org.cn

Engidaw, A. E. (2021). The effect of external factors on industry performance: The case of lalibela city micro and small enterprises, Ethiopia. Journal of Innovation and Entrepreneurship, 10(10), 1–14.

Grossman, G., & Helpman, E. (1990). Comparative advantage and long-run growth. American Economic Review, 80(4), 796–815.

Iamsiroroj, S., & Ulubasoglu, M. A. (2015). Foreign direct investment and economic growth: A real relationship or wishful thinking? Economic Modelling, 51(4), 2000–2213.

Inada, M. (2013). The effects of foreign direct investment on industrial growth: Evidence from a regulation change in China (Working Papers 856). Kyoto University, Institute of Economic Research.

International Labor Organization. (2023). International standard industrial classification of all economic activities (ISIC). ILO.

International Trade Administration. (2023). South Africa country commercial guide. ITA.

Jiang, H., & Liu, C. (2011). Forecasting construction demand: A vector error correction model with dummy variables. Construction Management and Economics, 29(3), 967–979.

Kansas City Fed. (2023). China’s post-covid recovery: Implications and risk. Economic Bulletin. Federal Reserve Bank.

Kasri, R. A., Indrastomo, B. S., Hendranastiti, N. D., & Prasetyo, M. B. (2022). Digital payment and banking stability in emerging economy with dual banking system. Heliyon, 8(11), 1–12.

Kiely, R. (1994). Development theory and industrialization: Beyond the impasse. Journal of Contemporary Asia, 24(2), 133–160.

Kummritz, V. (2016). Do global value chains cause industrial development? (CTEI Working Papers series 01–16). Centre for Trade and Economic Integration.

Kuo, C. (2016). Does the vector error correction model perform better than others in forecasting stock price? An application of residual income value theory. Economic Modelling, 52(2), 772–789.

Legros, P., & Newman, A. (1995). Wealth effect, distribution and the theory of organization. Journal of Economic Theory, 70(2), 312–341.

Li, X., & Liu, X. (2005). Foreign direct investment and economic growth: An increasingly endogenous relationship. World Development, 33(3), 393–407.

Martorano, B., Sanfilippo, M., & Haraguchi, N. (2017). What factors drive successful industrialization? Evidence and implications for developing countries. Inclusive and Sustainable Industrial Development (Working Paper Series no. WP 7 | 2017). UNIDO.

Mishra, D., Mody, A., & Murshid, A. P. (2001). Private capital flows and growth. Finance and Development, 38(2), 2–5.

Morduch, J. (1990). In Risk production and savings: Theory and evidence from Indian household. Harvard University Press.

Nigeria Bureau of Statistics. (2022). Annual report and statistics.

Otavio, R. M., Doornik, B., & Oliveira, G. (2011). Modelling and forecasting a firm’s financial statement with VAR-VECM Model. Brazilian Business Review, 8(3), 20–39.

Pandya, V., & Sisombat, S. (2017). Impacts of foreign direct investment on economic growth: Empirical evidence from Australian economy. International Journal of Economics and Finance, 9(5), 121–132.

Phillips, P. C., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346.

Rahman, A. S. (2010). An exceptionally simple theory of industrialization (Working Papers 27). US Naval Academy.

Romer, P. (1990). Endogenous technological change. Journal of Political Economy, 98(5), 21–37.

Safeguard Global. (2023). Top 10 manufacturing countries 2023. https://safeguardglobal. com

Samantha, N., & Liu, H. (2018). The effect of foreign direct investment on industrial sector growth: Evidence from Sri Lanka. Journal of Asian Development, 4(2), 88–106.

Samouel, B., & Aram, B. (2016). The determinants of industrialization: Empirical evidence for Africa. European Scientific Journal, 12(10), 219–239.

Saroy, R., Jain P., Awasthy, S., & Dhal, S. C. (2023). Impact of digital payment adoption on Indian banking sector efficiency. Journal of Banking and Financial Technology, 7(1), 1–13.

Singh, A. K., & Kumar, S. (2021). Assessing the performance of factors affecting industrial development in India states: An empirical analysis. Journal of Social Economics Research. 8(2), 135–154.

Solow, R. (1956). A contribution to the theory of economic growth. Quarterly Journal of Economics, 70(1), 65–94.

Stock, J. H., & Watson, M. W. (1993). A simple estimator of co-integrating vectors in higher order integrated systems., Econometrica, 61(4), 783–820.

Sugihara, K. (2019). Multiple paths to industrialization: A global context of the rise of emerging states. In K. Otsuka & K. Sugihara (Eds), Paths to the emerging state in Asia and Africa. Springer.

Swan, T. (1956). Economic growth and capital accumulation. Economic Record, 32(3), 334–361.

Worku, G. (2010). Electronic banking in Ethiopia––Practices, opportunities and challenges. Journal of Internet Banking & Commerce, 12(2), 42–58.

Tongxina, A., Yuejinb, F., & Huanc, Z. (2011). An analysis of the model of China’s industrial restructuring and upgrading-borrowing ideas from the experience of Japan. Energy Procedia, 5(1), 1461–1466.

Unified Payments Interface. (2023). India UPI: A global front-runner in digital payment systems. https://www.npci.org.in

Vertakova, Y., Plotnikovb, V., & Culicov, M. (2015). The key factors, determining the industrial development of Russia under the conditions of membership in the WTO. Procedia Economics and Finance, 24(3) ,743–749.

West, D. M., & Lansang, C. (2018). Global manufacturing scoreboard: How U.S compares with 18 other nations. Brooking Research Paper. https://www.brookings.edu

Whitfield, L., Staritz, C., & Morris, M. (2020). Global value chains, industrial policy and economic upgrading in Ethiopia’s apparel sector. Development and Change, 51(4), 1018–1043.

Yang, F., Sun, Y., Zhang, Y., & Wang, T. (2021). Factors affecting the manufacturing industry transformation and upgrading: A case study of Guangdong–Hong Kong–Macao Greater Bay area. International Journal of Environmental Research and Public Health, 18(2), 1–14.

Yu, J., Jong, R., & Lee, L. (2008). Quasi-maximum likelihood estimators for spatial dynamic panel data with fixed effects when both N and T are large. Journal of Econometrics, 146(1), 118–134.