IIMS Journal of Management Science

Search

Search

Ambrose Ogbonna Oloveze1 , Charles C. Ollawa1, Kelvin Chukwuoyims2

, Charles C. Ollawa1, Kelvin Chukwuoyims2 and Victoria Ogwu Onya2

and Victoria Ogwu Onya2

1 Department of Marketing, Michael Okpara University of Agriculture, Umudike, Abia State, Nigeria

2 Department of Business Administration, Alex Ekwueme Federal University Ndufu-Alike Ikwo, Ebonyi State, Nigeria

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The purpose of the study is to evaluate micro, small and medium enterprises’ (MSMEs) reaction to the pan-African payment and settlement system (PAPSS). The new cross-border e-payment technology is designed to facilitate cross- border instant payments, motivate cross-border businesses and promote sub-Saharan African trades which have been a real problem following the involvement of third currency, untimely payment and regulations that impact payments across borders. The study is important because of the non-existence of empirical results on what motivates MSMEs’ intention to use it and how the experience might impact the intention to use PAPSS. Thus, the study considered the impact of MSMEs’ previous experience on e-payment as a moderating influence on intention to use PAPSS. An adapted questionnaire that was structured on 7-point Likert scale was used in the survey to collect data from MSMEs in Nigeria. Structural equation modelling and the Hayes process for moderation were used in the analysis. The authors learned that ease of use is the strongest indirect determinant of intention to use PAPSS while perceived compatibility is the strongest direct determinant of intention to use PAPSS. Further, the authors discovered the important role of the simplicity of the innovation and its compatibility with users’ characteristics in promoting intention to use. The level of experience is confirmed to be significant in moderating intention to use PAPSS. Therefore, deeper involvement of the apex banks and commercial banks in communicating simplicity is paramount to achieve significant progress, while the services of tech experts and professionals can be utilised to provide periodic information to business owners through organised TV and radio programmes. Notably, this is a novel study that focuses on new cross-border payments in sub-Saharan Africa.

E-payment, PAPSS, intention to use, MSME, cross-border payment, sub-Saharan Africa

Introduction

The era of digital technology is tremendously transforming the global economy. This is inclusive of the sub-Saharan African economy where technology has continued to thrive in changing the dynamics of business operations for micro, small and medium enterprises (MSMEs) in product offering, services and payment processes. Typically, economies like the Nigerian economy have shown rapid progress in the adoption of digital innovations like e-payment (Igudia, 2018). These are driven by factors such as interoperability, the mobile-first generation that loves instant payments, the informal sector demand for transparency, the rising use of m-payments and the demand for frictionless payments (Nairametrics, 2023a). Despite the progress, African MSMEs are cumbered with several challenges such as poor level of information technology (IT) skills (Igudia, 2018), deficient financial infrastructure, high exclusion rate (Oyelami et al., 2020) and poor IT infrastructure that mostly appear in form of network instability (Abdulmumin, 2020). In the midst of these challenges, Nigerian MSMEs have continued to demand for an innovative payment system that will improve the efficiency and performance of their businesses (Thisday, 2023).

In Nigeria, the activities of MSMEs constitute 96% of total operating ventures in different economic sectors, with 73% of sole proprietorship businesses representing the highest in ownership structure (PwC, 2020). MSMEs are about 41.5 million in Nigeria (Small & Medium Enterprises Development Agency of Nigeria and National Bureau of Statistics, 2017). They contribute significantly to economic growth and development, employment growth and industrialisation (National Bureau of Statistics, 2019). Statistically, they contribute about 77% of workforce employment, 50% of gross domestic product and 8% of exports (PwC, 2020). Despite the contributions to the national economy, the export contribution is poor compared with MSMEs’ 49.4% and 68% contribution in India and China, respectively (Taiwo-Oguntu, 2022). The factors accounting for this include MSMEs’ poor competitiveness, inadequacy of finance, policy and regulatory issues that hinder MSMEs’ development, poor linkage to the potentials of regional markets and lack of policies that promote MSMEs’ participation in regional markets (Okojie, 2022). However, the role of technology in the global economy, its application in MSMEs’ operations, IT skill and knowledge needs of owners, need for instant payments and the competitiveness of the sector are recognised to be critical in improving the contribution of MSMEs in cross-border trades (Taiwo-Oguntu, 2022).

Remarkably, Nigeria’s MSME industry has the highest number of businesses in the sub-Saharan region at 99.8% and is the greatest contributor to employment generation at 84% (PwC, 2020). These MSMEs’ survival rate after five years of operation is about 20% because of the challenges associated with compliance regulations and multiple taxes, insufficiency of cashflows and issues with obtaining finance (Enabling Business Environment Secretariat, 2021). The industry is cumbered with delayed payments, cashflows and revenue challenges because of associated terms of trade policies (PwC, 2020). Though upskilling, business digitalisation and integration of technological advancements are gaps to be covered in the industry (PwC, 2020), the industry records an abysmal adoption rate of innovations (Igboeli & Bisallah, 2020). Generally, their performance is impacted by rising inflation, high interest and exchange rates, the pressure to reduce the price of their products (PwC, 2020), while the existing payment infrastructure badly impacts access to forex (Abraham, 2023). Banks are the major institutions involved in cross-border payments in the sector with studies indicating that 61% of MSMEs prefer banks’ solutions to 19.5% of MSMEs opting for fintech solutions (Abraham, 2023). However, MSMEs feel comfortable with the banks across sub-Saharan Africa because of years of business and trust in the system (Abraham, 2023). Recently, fintech such as NALA, eTranzact and Flutterwave have evolved to offer services to MSMEs in Nigeria to accelerate commerce in the region (Michael, 2023).

Payments in Africa are majorly through real-time gross settlement systems (RTGS) transfers (Interledger Foundation, 2021). Recently, the African Export–Import Bank (Afreximbank) and African Continental Free Trade Agreement (AfCFTA) introduced the pan-African payment and settlement system (PAPSS), which is driven towards promoting cross-border payments in the African market (KPMG, 2021). African payment systems are highly fragmented (Interledger Foundation, 2021). PAPSS serves as a centralised payment settlement system for promoting the instant payment of product purchases across national frontiers in Africa. It ‘is a central financial market infrastructure that supports payment arrangements for the purpose of expanding the international trade of African states, and to facilitate central bank’s economic and financial integration’ (Stanbic IBTC, n.d., p. 1). The goal is to drastically minimise reliance on third currency in payment for goods, positively impact e-commerce in Africa and facilitate instant payments and safety of business transactions (Aro, 2022). It has been successfully piloted in Nigeria, Ghana, Guinea, Gambia and Liberia with further planned rollouts in 2023 at Zimbabwe, Zambia and Djibouti (Rwandapost, 2023). The goal is to boost African trade by executing payments in local currencies since payments are the lifeblood of trade (Aelex, 2022). The cutting-edge technology requires a participating bank or payment service provider to sign up to the system and prefund the settlement account (KMPG, 2021). With this, instant payments occur in local currencies once the importer issues payment instructions to the participant bank (KMPG, 2021), thereby enabling payments and receipts in local currency (Aelex, 2022). The issue with exchange rates is resolved through PAPSS as it is available to the participating bank and communicates to the importer. The process occurs instantaneously or near instantaneously (KPMG, 2021). The key advantage to the entrepreneur and MSMEs is facilitation of intra-African trade and cross-border payments (Aelex, 2022), minimisation of heavy reliance on third currency, provision of low-cost measure and risk-controlled instant payment (Stanbic IBTC, n.d.). The major attraction to entrepreneurs and MSMEs is the chance of instantaneous payment (Aelex, 2022).

However, the e-payment system in Nigeria is characterised by online transfers, automated teller machine (ATM) transactions, mobile money operators (MMOs), point of sale (PoS) transactions, unstructured supplementary service data (USSD) transfers, mobile app transfers (not mobile money), national electronic fund transfer (NEFT), RTGS transfers and direct debts with online transfers accounting for the largest percentage of e-payments (Statista Research Department, 2022). The adoption of e-payment was accelerated by the COVID-19 pandemic leading to 40.9% and 46.5% increases in value and volume of transactions, respectively (Nairametrics, 2023b). This is further deepened by the naira scarcity that increased the adoption of e-payment channels while becoming a menace to users because of the e-payment glitches at the time. However, experience is an important variable in adopting innovation. Extant studies indicate that it arises from an impression (Carbone & Haeckel, 1994) and influences behaviour (Fishbein & Ajzen, 1975) while the level of effort committed to the usage of the system depends on the level of experience (Liebana-Cabanillas et al., 2014). Thus, what are the determinants of MSME owners’ intention to adopt PAPSS? To what extent does the level of experience moderate MSMEs’ intention to adopt PAPSS? The purpose of the study is to estimate MSMEs’ reaction to new payment technology for cross-border payment and evaluate the impact of their level of experience on adoption.

Literature Review

The significance of accepting new technology has made it an attraction to researchers, so studies have continued to evolve with the emergence of technological innovations in the business environment. With the emergence of PAPSS, its successful rollouts and involvement of the banks as partners in the operation, the success can be predicted given the existing business relationships between MSME owners and banks in cross-border transactions. However, banks are not the only parties involved in recent times. The advancements in technology have facilitated the involvement of fintech in offering opportunities to MSMEs in cross-border payments. For instance, fintech such as AZA Finance that operates in Ghana, Nigeria, Kenya and several other nations (AZA Finance, n.d.), NALA operates in Tanzania, Flutterwave and Lemfi operate in sub-Saharan Africa (Michael, 2023), and while there is the existence of collaborated efforts between banks and fintech such as Access Bank and eTranzact’s involvement in Nigeria, Ghana and Kenya (Abraham, 2023); and Access Bank and Thunes partnership that offers cross-border payments across 13 markets in Africa (Moses-Ashike, 2023). The goal of these involvements is to promote cross-border business transactions, facilitate payments and increase the scale of businesses in the region.

However, attracting new users and maintaining old ones are of interest in marketing. With respect to innovation, several models and theories have been used in the literature to study consumer behaviour. Some of them include the technology acceptance model (TAM) (Davis, 1989), diffusion of innovation (DOI) (Rogers, 2003) and theory of reasoned action (Fishbein & Ajzen, 1975). The present study is focused on a model of behaviour that deals with the acceptance of innovation. This includes TAM and DOI. First, the usefulness of TAM in e-payment studies is supported by the robustness of the model, its applicability in different types of technological innovation, reaffirmation of the validity of the theory through studies and its specific ability to deal with factors that influence the adoption of information system (Jeong & Yoon, 2013). The limitation of TAM such as the omission of vital variables (Jeong & Yoon, 2013) has resulted in the combination of the factors with other model’s factors (Hidayat-ur-Rehman et al., 2022; Liebana-Cabanillas et al., 2014; Oloveze, et al., 2022a). For instance, Coskun et al. (2022) explored factors influencing the adoption of online payment systems by using TAM and DOI theories to confirm relative advantage as the most important predictor of intention to adopt an online system. In another study involving mobile payments, Ali et al. (2022) integrated the frameworks of TAM, DOI and unified theory of acceptance and use of technology to predict usage behaviour; relative advantage was confirmed as the most significant direct factor influencing intention to use. Schierz et al. (2010) identified compatibility, mobility and subjective norm as the determinants of adopting m-payment services. Liebana-Cabanillas et al. (2014) developed a model that included external influences, trust and risk to original TAM with age as a moderating variable. The result supports the extension of TAM to study innovations. Oloveze et al. (2022a) extended the TAM construct with trust, customisation, risk and subjective norm to study cardless cash and consumer psychology in Nigeria and discovered that customisation is the most vital significant determinant of intention to use. Sheng et al. (2011) demonstrated that perceived usefulness, ease of use, compatibility and perceived risk are significant determinants that influence the acceptance of mobile banking. Finally, Yang et al. (2012) considered the effects of behavioural beliefs, social influence and personal traits to confirm perceived risk, compatibility, personal innovativeness in IT, subjective norm, relative advantage and perceived fee as significant determinants of m-payment service adoption across time. In this regard, the present study considered the adoption of PAPSS by MSMEs through factors of TAM and DOI models by including experience as a moderating variable on intention to use PAPSS.

Hypotheses Development

Ease of Use

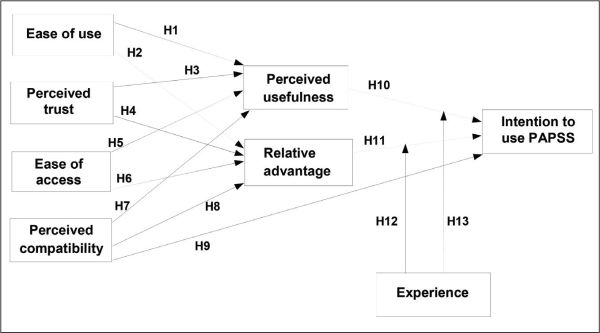

Ease of use (EoU) is the perception that users have about an innovation specifically in being less complicated to use or simple in application. It is a key variable of Davis’ (1989) TAM. It is argued to influence perceived usefulness (Hossain et al., 2017) but not supported as a direct influence on behavioural intention (Davis, 1989). Thus, TAM suggests a simultaneous influence on intention particularly from self-efficacy and instrumentality. It has been variedly applied in the study of innovations such as online shopping (Oloveze et al., 2022b) and location-based studies (Hossain et al., 2017). With respect to PAPSS, it is believed that as a novel payment system, it should be simple in application and implementation, thereby making it a better option than the existing payment system. Thereto, the authors consider a nexus between EoU and relative advantage when the implementation by users is perceived to be simpler than the existing option. Thus, we hypothesise:

H1: EoU is positively related to perceived usefulness towards adopting PAPSS.

H2: EoU is positively related to the relative advantage towards adopting PAPSS.

Perceived Trust

Perceived trust is a perception of being trustworthy, maintenance of promised security and a psychological state of entrusting reliance and confidence in expected payment outcomes. It is often associated with the confidentiality of data and level of integrity in service usage (Kalinic et al., 2019). It is vital in the acceptance of innovations (She et al., 2017) given its significant role in the pre-adoption and post-adoption of innovations (Talwar et al., 2020). Studies suggest that it can positively improve perceived usefulness (Liebana-Cabanillas & Alonso-Dos-Santos, 2017) and intention (Ali et al., 2022). It can improve users’ recognition of the superior benefit of an innovation over an existing one especially where users perceive it to be more reliable, safe, trustworthy and promising than existing options. Thus, we hypothesise:

H3: Perceived trust is positively related to perceived usefulness towards adopting PAPSS.

H4: Perceived trust is positively related to relative advantage towards adopting PAPSS.

Ease of Access

The concept of accessibility is gradually integrated into the e-payment system to gain a deeper insight on issues of accessibility by potential innovation users. It is a multidimensional construct that consists of computer, and information accessibility, reliability, ease of learning (Rice & Shook, 1988) and system usability (Karahanna & Straub, 1999). In this study, the focus is on system usability, accessibility to information and reliability of the novel payment system. Extant studies suggest a relationship between ease of access and system usability, thereby enhancing adoption (Poon, 2008). Accessibility is claimed to influence users’ perceived usefulness of a system (Fonchamnyo, 2013) such that it improves the potential of future usage (Liebana-Cabanillas et al., 2013). Where accessibility to use PAPSS is perceived to be simple to make and receive payments instantly than existing option, users will most likely have positive reactions to its use. Therefore, we hypothesise:

H5: EoA is positively related to perceived usefulness towards adopting PAPSS.

H6: EoA is positively related to the relative advantage towards adopting PAPSS.

Perceived Compatibility

The concept of compatibility is one of the technological characteristics that influence adoption. It deals with the extent of consistency in values, beliefs and previous experiences associated with the potential user (Rogers, 2003). Intention to adopt innovation is enhanced where there is compatibility between the potential users’ needs and the technology offerings (Hidayat-ur-Rehman et al., 2022). Studies suggest its influence on perceived usefulness (Ramos-de-Luna et al., 2017) and intention to use (Schierz et al., 2010) especially when there is coherence between the potential adopters’ values, lifestyle and innovation characteristics. Further, the offer of a superior experience is associated with compatibility where users’ values and lifestyles are consistent with the choice of better ways of doing things. Thus, where users perceive that the innovation will offer a better experience, it will improve the chance of adoption. Therefore, we hypothesise:

H7: Perceived compatibility is positively related to perceived usefulness towards adopting PAPSS.

H8: Perceived compatibility is positively related to the relative advantage towards adopting PAPSS.

H9: Perceived compatibility is positively related to the intention to adopt PAPSS.

Perceived Usefulness

Perceived usefulness is one of the vital variables of TAM. It is the degree to which an innovation is able to improve users’ performance (Davis, 1989). The innovation must offer utility to potential users to have any chance of adoption (Oloveze et al., 2021). Studies suggest that it impacts intention to use (Ali et al., 2022). In this study, the key usefulness is the intended promotion of cross-border trade and instant payment in local currency, and minimisation of excessive dependence on third currency. Therefore, we hypothesise:

H10: Perceived usefulness is positively related to intention to adopt PAPSS

Relative Advantage

In e-payment, every new technology is considered to have an edge over older ones given that it is a requirement for the sustenance and survival of new technology (Utomo et al., 2022). Relative advantage is a concept that considers an innovation to be better in benefit offering, performance and utility than existing ones (Khanra et al., 2021). In the e-payment system, it consists of better benefits of time utility, transparency of transaction, security and superior satisfaction (Moncada et al., 2022). Studies confirm its effect on intention to use (Ali et al., 2022; Hidayat- ur-Rehman et al., 2022). Therefore, we hypothesise:

H11: Relative advantage is positively related to intention to adopt PAPSS.

Experience

Experience is a concept that has gained the attention of professionals given its applicability in various fields. However, Bilgihan et al. (2016) argue that information on experience is fragmented. Experience is the impression carried by the user after being in contact with a product or service, and this forms or consolidates perception (Carbone & Haeckel, 1994). It influences current behaviour where the previous experience is positive about an item (Fishbein & Ajzen, 1975) so that higher use experience with previous innovations positively influences the adoption of similar innovations. This is often influenced by higher benefits and less invested efforts such that potential users with a low level of experience are motivated by intrinsic and extrinsic benefits to the extent that they invest more time (Liebana-Cabanillas et al., 2014). Extant literature indicates the existence of contrasting results. Hernández et al. (2009) and Liebana-Cabanillas et al. (2014) argue that users with a low level of experience consider usefulness more in their intention to adopt a system. Experience has the tendency to produce deep impacts on consumer/user memory especially when it is associated with the benefits and features of an item (Chase & Dasu, 2014). In this context, it includes a blend of knowledge and occurrences that can collectively shape user attitude and behaviour. Users with experience of similar innovation or common IT skills will appreciate the usefulness, thereby improving the user’s perception of usefulness and usage. Extant literature suggests that users with IT experience and previous experience of related innovation are more likely motivated by the usefulness in improving efficiency and performance (Dholakia & Uusitalo, 2022), which in turn has improved positive influence on users’ intention (Liebana-Cabanillas et al., 2014; Niemelä-Nyrhinen, 2009). Similarly, users with an increased experience of related innovation are more likely to understand and appreciate the better utility, performance and benefit of an innovation compared with existing options. The relative advantage is anchored on a previous experience of users in being able to discover the difference between existing options against PAPSS innovation. Increased user experience of the operation of IT or similar innovation tends to create a pathway for users’ mental assessment of the available options to the users. Thus, with regard to the moderating effect of experience, the users with a low level of experience in IT or similar innovation will require a higher perception of usefulness compared with the users that are more experienced. Though some studies revealed no moderating effect of experience on the relationship between perceived usefulness and intention (Castaneda et al., 2007; Gefen et al., 2003), others suggest a significant moderating effect (Liebana-Cabanillas et al., 2014). Similarly, with relative advantage, the ability of the users to understand and perceive the difference between the utility of two different innovations is anchored on the level of the users’ experience. This will suggest that usefulness and relative advantage are more important to users who are inexperienced. This is because studies suggest that the impact of experience in moderating the effect of usefulness and relative advantage on intention tends to reduce with time because of the knowledge that the user was able to acquire through experience (Taylor & Todd, 1995; Venkatesh et al., 2003). Therefore, any innovation such as PAPSS can be evaluated using previous experience. This will lead to different levels of user perception of usefulness and relative advantage towards intention to use. In this study, perceived usefulness is posited to be moderated by experience so that the effect of perceived usefulness on intention to use PAPSS is higher among MSMEs with a low level of e-payment experience. The impact of relative advantage on intention to use is posited to be higher among low-level experienced users of e-payment, considering that the insufficient experience will make them pay more attention to the better and improved benefits as motivation for adoption. Therefore, we hypothesise:

H12: The effect of perceived usefulness on intention to use PAPSS is significantly higher among MSMEs with low e-payment experience.

H13: The effect of relative advantage on intention to use PAPSS is significantly higher among MSMEs with low e-payment experience.

Research Methodology

Measurement Development

The questionnaire items were adapted from the literature. Figure 1 shows the conceptual model of the study and the different paths in the model. Perceived usefulness, EoU and compatibility were adapted from Schierz et al. (2010). Each variable was measured with four items. Intention to use was adapted from Davis (1989) and measured with three items. Ease of access was adapted from Liebana-Cabanillas et al. (2013) and measured with four items. Perceived trust was adapted from Liebana-Cabanillas et al. (2014) and measured with three items. Relative advantage was adapted from Moore and Benbasat (1991) and measured with three items. The questionnaire was designed on 7-point Likert scale. Preliminary checks were done for reliability and suitability of the scale using experts in the field.

Figure 1. Conceptual Model.

Data Collection

Data were collected through self-administration and online methods using a questionnaire designed on Google Form. The link was shared to first contacts while snowball sampling was also adopted to share the link to other appropriate respondents. The MSME owners were selected from a cluster of MSMEs who accept the e-payment channel in their business. A total of 314 samples were drawn. Twenty-nine (9.2%) copies were screened out for not having used the e-payment channel in their business, thus making the valid forms used to be 285 (90.8%).

Results

The results from the respondents revealed that out of the 285 valid forms, 76% of male owners of MSME were represented in the study while 24% of female respondents participated in the survey. This confirms the male dominance of MSMEs in Nigeria, which is consistent with earlier studies (CSEA, 2023). The age of the respondents revealed that 54% of respondents were below 35 years, while 46% of respondents were above 35 years. With experience, 62.5% had high experience of the usage of e-payment channels while 37.5% had low experience. Studies confirmed that experience can significantly influence the success of entrepreneurial ventures (Genty et al., 2015). This is consistent with the adoption of practices and payment methods that MSME owners perceive can improve performance.

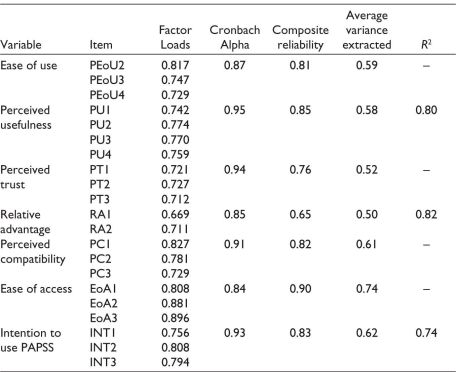

Confirmatory Factor Analysis: Reliability and Validity

STATA and SPSS 21 were used in the analysis. Common method bias (CMB) was conducted through Herman’s single-factor test by adjusting all items to a single factor using an unrotated option. The result of 50% indicates that CMB is not a problem. Confirmatory factor analysis was executed for reliability and validity using varimax rotation with Kaiser normalisation. The Kaiser–Meyer–Olkin is 0.928, thereby confirming sampling adequacy. Bartlett’s test of sphericity value of 6560.781 at p = 0.000 confirms the rejection of the null hypothesis of no difference in the variance of the responses. It validates data suitability for factor analysis. Reliability was executed through Cronbach’s alpha, composite reliability and average variance extracted using thresholds of 0.6, 0.7 and 0.5, respectively (Hair et al., 2006). The result in Table 1 shows that the thresholds were met, thereby confirming the reliability of the instrument. Validity was executed using convergent validity through the factor loadings of the indicators. All the loadings were above 0.6 (Bagozzi & Yi, 1988), thereby confirming the validity of the instrument. However, ease of use, perceived compatibility, ease of access and relative advantage were not added to the analysis because the loadings were less than 0.6. Therefore, relative advantage was measured with 2 items. This is accepted in situations where the two retained items have high correlation (that is r > 0.70) and fair uncorrelation with other variables (Worthington & Whittaker, 2006; Yong & Pearce, 2013). In this case, the r value of RA1 and RA2 is 0.768.

Table 1. Measurement Model Evaluation.

Testing of Hypotheses

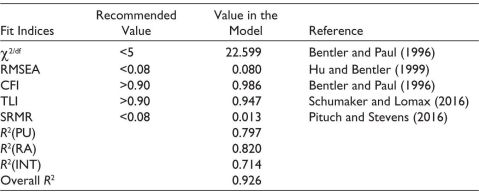

Structural equation modelling (SEM) through maximum likelihood and the Hayes process model for moderation were used in the analysis. First, the fit of the structural model was confirmed through the goodness-of-fit indicators following the recommendations in the literature. The values for all the indicators exceed the recommended thresholds in literature except the chi-square value as shown in Table 2. Chi-square is influenced by large samples as obtained in the present study. The R2 value (0.926) of the model further confirms the fit of the structural model. R2 is a reliable indicator of variance explained in the model which should be closer to 1 (Falk & Miller, 1992).

Table 2. Model Fit Indices.

Note: RMSEA = root mean squared error of approximation; CFI = comparative fit index; TLI = Tucker–Lewis index; SRMR = standardised root mean squared residual; RA = relative advantage; INT = intention to use.

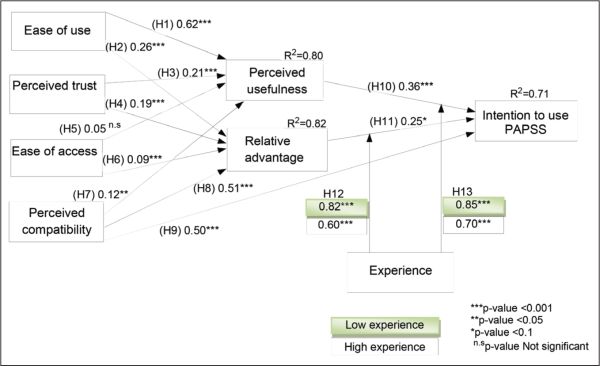

Second, the paths were examined through standardised estimates, statistical significance and critical ratio of the paths as shown in Table 3 and Figure 2. Ten of the 11 assessed paths were significant. The findings revealed that EoU is positive and significantly related to perceived usefulness and relative advantage. Therefore, the result supports H1 (β = 0.62, p .png) 0.001) and H2 (β = 0.26, p

0.001) and H2 (β = 0.26, p .png) 0.001). Further, H3 (β = 0.21, p

0.001). Further, H3 (β = 0.21, p .png) 0.001) and H4 (β = 0.19, p

0.001) and H4 (β = 0.19, p .png) 0.001) were confirmed, thus proving the significant effect of perceived trust on perceived usefulness and relative advantage, respectively. H5 was rejected, thereby revealing that ease of access does not influence perceived usefulness. However, H6 (β = 0.09, p

0.001) were confirmed, thus proving the significant effect of perceived trust on perceived usefulness and relative advantage, respectively. H5 was rejected, thereby revealing that ease of access does not influence perceived usefulness. However, H6 (β = 0.09, p .png) 0.001) is supported, thereby confirming the significant effect of ease of access on relative advantage. H7, H8 and H9 were from perceived compatibility. The findings reveal that perceived compatibility significantly influences perceived usefulness, relative advantage and intention to use PAPSS. Therefore, the results confirm and support H7 (β = 0.12, p

0.001) is supported, thereby confirming the significant effect of ease of access on relative advantage. H7, H8 and H9 were from perceived compatibility. The findings reveal that perceived compatibility significantly influences perceived usefulness, relative advantage and intention to use PAPSS. Therefore, the results confirm and support H7 (β = 0.12, p .png) 0.05), H8 (β = 0.51, p

0.05), H8 (β = 0.51, p .png) 0.001) and H9 (β = 0.50, p

0.001) and H9 (β = 0.50, p .png) 0.001), respectively. Also, the results show that perceived usefulness and relative advantage have positive and significant influence on the intention to use PAPSS. The results support and confirm H10 (β = 0.36, p

0.001), respectively. Also, the results show that perceived usefulness and relative advantage have positive and significant influence on the intention to use PAPSS. The results support and confirm H10 (β = 0.36, p .png) 0.001) and H11 (β = 0.25, p

0.001) and H11 (β = 0.25, p .png) 0.1).

0.1).

Figure 2. Result of Conceptual Model.

Table 3. Hypothesised Relationships.

Notes: **p-value < 0.001; *p-value <0.05.

The moderating effect of experience is illustrated in Table 3 and Figure 2. The Hayes process was adopted in assessing the moderating effect of experience on intention to use PAPSS. The continuous items were mean centred. The 5000 bootstrapping method was used with the 95% confidence level for confidence intervals and the bias-corrected bootstrap CI method. The result confirms that experience significantly moderates the effect of perceived usefulness and relative advantage on intention to use PAPSS between the two groups. This is supported by the p values of the estimates H12 (β = 0.82, p 0.001) for low experience and (β = 0.60, p 0.001) for high experience with a significance difference (f-value = 9.93, p 0.001). With perceived usefulness, the hypothesis is confirmed H13 (β = 0.85, p 0.001) for low experience and (β = 0.70, p 0.001) for high experience with a significance difference (f-value = 5.69, p 0.05).

Discussion, Implications, Conclusion and Limitation

Discussion of Results

The purpose of the study is the reaction of MSMEs to the cross-border novel payment system and the impact of their level of experience on intention to adopt the innovation. The structural model was validated, thus proving the three-layer model to be a good fit in the estimation. Notably, the model was anchored on the innovation characteristics of PAPSS through relative advantage and the personal characteristics of MSMEs’ potential users through perceived usefulness. The model proved that the indirect effect in the first layer (EoU, perceived trust, ease of access and perceived compatibility) influences the variables in the second layer (perceived usefulness and relative advantage), whereas the second layer estimates confirm the direct effect on intention to use PAPSS. Perceived compatibility is estimated indirectly and directly because of the significance of the alignment of values and believes with characteristics of innovation. This is confirmed in the study. Further, the relationship between the second layer and intention to use PAPSS was tested and confirmed. Thus, with the support of the paths, the results are discussed.

First, EoU is the most significant determinant of perceived usefulness among the variables. Previous studies indicate the importance of simplicity of innovation and effortlessness in usage as a condition for the success of adoption. It aligns with previous studies on technological payment innovation (Liebana-Cabanillas et al., 2014; Oloveze et al., 2022b; Ramos-de-Luna et al., 2017) and confirms its important role in the adoption of payment innovation in developing nations. Thus, EoU is the strongest indirect factor for PAPSS greater penetration in Nigeria and sub-Saharan nations where PAPSS has been piloted. Further, the relationship between EoU and relative advantage proves that the adoption of PAPSS is facilitated when its application and usage are easier and better than the previous existing payment option. Therefore, projecting the EoU is fundamental. This demands the use of strategic marketing communications by the right sources such as the participating bank, apex bank and service providers to disseminate the relative advantage of PAPSS on effortlessness is usage.

Second, perceived trust is positive and significantly related to perceived usefulness as the second most important factor. This is similar to earlier studies on payment innovation (Liebana-Cabanillas & Alonso-Dos-Santos, 2017). The result reveals the significant role of trust in pre-adoption, thereby deepening the emphasis on users’ trust in a reliable payment system that delivers on promises. Regardless of the promises of the technology, consistency in reliability, trustworthiness and offer of better performance than previous innovation is critical in motivating MSME users to adopt PAPSS. Further, trust is associated with a relative advantage, though the relationship is weak. However, it indicates the importance of deepening trust issues around the new payment system and projecting the superior security it has over existing options. Customers and users of the payment system tend to patronise a payment system that offers better security and superior benefits. Designing strategies to promote the benefit is necessary for improved adoption.

Third, perceived compatibility is theorised as a direct and indirect determinant of intention to use PAPSS. The positive results are confirmed in the literature (Ramos-de-Luna et al., 2017; Schierz et al., 2010). The implication is that the coherence of the characteristics of PAPSS with the MSME users’ values and lifestyles is vital in adopting PAPSS. Thus, the innovation characteristics should be tailored to the lifestyle of users and their values while aligning it with their past experiences on e-payment. Though the relationship is weak on perceived usefulness, the effect on relative advantage and intention to use PAPSS is the highest, thereby revealing compatibility as the most significant direct predictor of relative advantage and intention to use.

Fourth, ease of access is proven to be associated with relative advantage, though the effect level is weak. The positive result aligns with earlier results (Fonchamnyo, 2013). Thus, the adoption of PAPSS is dependent on better usability, better access to information and more reliability of the system. With this potential, future usage is improved where MSMEs perceive better benefit of accessibility in making and receiving instant payment for e-commerce transactions than existing payment options. This implies that there is a need to design friendly policies that encourage MSME users’ adoption of PAPSS. Communicating the benefit to MSMEs is essential to enable them to gain better information on the new payment technology.

Fifth, perceived usefulness significantly predicts intention to use PAPSS. The positive result is consistent with TAM and earlier studies (Ali et al., 2022; Davis 1989; Oloveze et al., 2022b). MSME users place value on PAPSS from its ease of handling payments and promotion of instant payments in local currency. Further, the result contributes to the existing body of knowledge by validating the path between usefulness and intention to use new payment technology.

Sixth, the moderating effect of experience between relative advantage and intention to use PAPSS is higher among users with low experience than those with high experience. The result indicates the important role of knowledge, and IT skill and innovativeness in adoption. Where MSME users have a low level of experience, the tendency to pay more attention to better benefits of the innovation over the existing payment system is justified.

Seventh, experience moderates the influence of perceived usefulness on intention to use PAPSS. The influence is higher among users with low experience with the e-payment system, thereby proving consistency with earlier studies (Hernández et al., 2009; Liebana-Cabanillas et al., 2014). Those with a low e-payment system experience are motivated by intrinsic and extrinsic benefits as well as the usefulness of the innovation than ones with high experience in the e-payment system. Notably, users with low experience will commit more effort and seek more information to understand the usefulness than ones with high experience.

Implications and Contributions

The implications of the findings border on the theoretical contribution and managerial implication. This is a novel study following the novelty of the innovation, its localisation and drive to contribute to improved commerce within sub-Saharan Africa. It involved a three-layer model to identify the direct and indirect effects of the variables that influence MSMEs’ intention to use PAPSS. Theoretically, the result confirms that perceived compatibility has the strongest direct impact on the intention to use PAPSS. Perceived usefulness and relative advantage also had a direct effect on intention to use PAPSS. The model also confirmed the indirect influences on the intention to use PAPSS. This includes EoU influence on perceived usefulness and relative advantage; perceived trust influence on perceived usefulness and relative advantage; ease of access path to relative advantage; and perceived compatibility path to perceived usefulness and relative advantage.

From the managerial perspective, the focus should be on aligning the operation and use to the users’ previous experience, values, needs and beliefs of technology being able to impact business. In this regard, the involvement of the apex banks and commercial banks is paramount in creating and deepening communication on its values and contribution to business operations. The promotional communications should emphasise the difference and how it is better than earlier options. Second, the low values of perceived usefulness and relative advantage suggest the need to provide more information on its usefulness to the businesses and on how the innovation is superior in performance compared with the earlier options in existence. Further, since experience is established to have a moderating influence in the study, the services of tech experts and professionals can be utilised to provide information to business owners through either organised TV programmes, commercials or sponsored awareness programmes. Notably, the adoption of this innovation reveals that where it is connected to the users’ beliefs, values and previous experience, the volume of trade will increase, and more MSMEs will use it while its potential will gain further attraction in other regions.

Conclusion

The study considered the moderating effect of experience on intention to use PAPSS. A three-layer model was used to identify the significant factors and the moderating effect of experience on the relationships. The model was tested using SEM analysis and the Hayes process. The model evaluation proved that the model was appropriate and a good fit. The results of the analysis provided an understanding that the variables have linear relationships towards MSMEs’ intention to use PAPSS. The major variable with the strongest direct significant effect is perceived compatibility while EoU has the strongest significant indirect effect. The result from experience further proved that experience has a significant role in intention to use PAPSS. MSMEs with low experience have a higher perception of usefulness and relative advantage to the intention to use PAPSS than ones with high experience. However, the study had a number of limitations.

Limitation and Suggestion for Further Studies

One of the few limitations is the localisation of the study to Nigeria. Nigeria is one of the five African states where the innovation has been rolled out. Therefore, in line with future studies, the direction can be on the integration of the operation of PAPSS among MSMEs in different geographical locations. Another limitation is that the study adopted a cross-sectional survey, thereby limiting the evolvement of users’ behaviour to the innovation that occurs with time. This calls for a longitudinal survey to provide deeper insight into the predictors of MSME users’ intention to adopt PAPSS. This will deepen the robustness associated with the path relationships. The use of a non-probabilistic sampling technique is another key limitation given that samples were not randomly selected. Thus, future studies can adopt a probabilistic sampling approach given that it can impact external validity. Further, future studies should consider the inclusion of more variables and estimate how firm readiness and innovativeness of owners can mediate the predictors of PAPSS usage.

Declaration of Conflicting Interest

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iDs

Ambrose Ogbonna Oloveze  https://orcid.org/0000-0003-0320-9793

https://orcid.org/0000-0003-0320-9793

Kelvin Chukwuoyims  https://orcid.org/0000-0003-3210-726X

https://orcid.org/0000-0003-3210-726X

Victoria Ogwu Onya  https://orcid.org/0000-0003-8958-5356

https://orcid.org/0000-0003-8958-5356

Abdulmumin, S. M. (2020). The role of e-payment systems on economic growth in Nigeria.?https://portal.bazeuniversity.edu.ng/student/assets/thesis/202012101556481476 396142.pdf

Abraham, A. (2023). Banks are winning the opportunity to facilitate cross-border payments for Africa’s small businesses. https://techcabal.com/2023/08/05/banks-winnnin-cross-border-payments-small-busines-africa/

Aelex. (2022). Launch of the pan-African payment and settlement system: A new dawn for cross-border financial transactions in Africa. https://www.aelex.com/wp-content/uploads/2022/01/Launch-of-the-Pan-African-Payment-and-Settlement-System-%E2%80%93-a-new-dawn-for-cross-border-financial-transactions-in-Africa-.pdf

Ali, M., Syed, A. R., Faiza, H., Chin-Hong, P., & Chawly, L. Y. (2022). An integrated framework for mobile payment in Pakistan: drivers, barriers, and facilitators of usage behavior. Journal of Financial Services Marketing. https://doi.org/10.1057/s41264-022-00199-0

Aro, B. (2022). Emefiele: Pan-African payment platform will reduce use of dollars, pounds in continent’s trade. The Cable. https://www.thecable.ng/emefiele-pan-african-payment-platform-will-reduce-use-of-dollars-pounds-in-continents-trade/amp

AZA Finance (n.d.). Payment methods in West Africa: Ghana. https://azafinance.com/ payment-methods-in-west-africa-ghana/

Bagozzi, R. P., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1), 74–94.

Bentler, P. M., & Paul, D. (1996). Covariance structure analysis: Statistical practice, theory, directions. Annual Review of Psychology, 47, 563–592.

Bilgihan, A., Kandampully, J., & Zhang, T. (2016). Towards a unified customer experience in online shopping environments: Antecedents and outcomes. International Journal of Quality and Service Sciences, 8(1), 102–119.

Carbone, L. P., & Haeckel, S. H. (1994). Engineering customer experience. Marketing Management, 3(3), 8–19.

Castaneda, J. A., Munoz-Leiva, F., & Luque, T. (2007). Web acceptance model (WAM): Moderating effects of user experience. Information & Management, 44(4), 384–396.

CSEA. (2023). Policy brief: Women participation in MSME in Nigeria: Prospects, challenges and policy recommendations. https://cseaafrica.org/wp-content/uploads/2023/06/Policy-Brief-Womens-Participation-in-MSME-in-Nigeria-Prospects-Challenges-and-Policy-Recommendations-NEW.pdf

Chase, R. B., & Dasu, S. (2014). Experience psychology: A proposed new subfield of service management. Journal of Service Management, 25, 574–577.

Coskun, M., Saygili, E., & Karahan, M. O. (2022). Exploring online payment system adoption factors in the age of COVID-19: Evidence from the Turkish banking industry. International Journal of Financial Studies, 10(19), 1–27, https://doi.org/10.3390/ijfs10020039

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340.

Dholakia, R., & Uusitalo, O. (2002). Switching to electronic stores: Consumer characteristics and the perception of shopping benefits. International Journal of Retail and Distribution Management, 30(10), 459–469.

Enabling Business Environment Secretariat. (2021). Micro, small and medium enterprises (MSMEs) regulatory cost of compliance report. https://ngfrepository.org.ng:8443/bitstream/123456789/4903/1/MICRO%20SMALL

Falk, R. F., & Miller, N. B. (1992). A primer for soft modeling. University of Akron Press.

Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention and behavior: An introduction to theory and research. Addison-Wesley.

Fonchamnyo, D. C. (2013). Customers’ perception of e-banking adoption in Cameroon: An empirical assessment of an extended TAM. International Journal of Economics and Finance, 5(1), 166–176.

Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. MIS Quarterly, 27(1), 51–90.

Genty, K., Idris, K., Abd. Wahat, N. & Abd. Kadir, S. (2015). Demographic factors as a predictor of entrepreneurs’ success among micro, small and medium enterprises (MSMEs) owners in Lagos State, Nigeria. IOSR Journal of Business and Management, 17(2), 125–132.

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (6th ed.). Pearson Educational International.

Hernández, B., Jiménez, J. & Martín, M. J. (2009). Key web site factors in e-business strategy. International Journal of Information Management, 29(5), 362–371.

Hidayat-ur-Rehman, I., Alzahrani, S., Rehman, M. Z., & Akhter, F. (2022). Determining the factors of m-wallets adoption. A twofold SEM-ANN approach. PLoS One, 17(1), e0262954. https://doi.org/10.1371/journal.pone.0262954

Hossain, M. A., Hasan, M. I., Chan, C., & Ahmed, J. U. (2017). Predicting user acceptance and continuance behaviour towards location-based services: The moderating effect of facilitating conditions on behavioural intention and actual use. Australasian Journal of Information, 21, 1–22.

Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structured Equation Modeling, 6(1), 1–55.

Igboeli, U. H., & Bisallah, H. I. (2020). Information and communication technology in managing small and medium enterprises in Nigeria. Open Journal of Management Sciences, 1(2), 1–11.

Igudia, O. P. (2018). Electronic payment systems adoption by SMEs in Nigeria: A literature review. Nigerian Journal of Management Sciences, 6(2), 150–165.

Interledger Foundation. (2021). Open and instant payments in Africa, current landscape and opportunities. https://interledger.org/our-work/reports/open-and-instant-payments-in-africa.pdf?_cchid=4598b4e3af600a5d136f86bf38827d57

Jeong, B. K., & Yoon, T. E. (2013). An empirical investigation on consumer acceptance of mobile banking services. Business and Management Research, 2(1), 31–40.

Kalinic, Z., Liebana-Cabanillas, F. J., Munoz-Leiva, F., & Marinkovic, V. (2019). The moderating impact of gender on the acceptance of peer-to-peer mobile payment systems. International Journal of Bank Marketing, 38(1), 138–158. https://doi.org/10.1108/IJBM-01-2019-0012

Karahanna, E., & Straub, D. W. (1999). The psychological origins of perceived usefulness and ease-of-use. Information & Management, 35(4), 237–250.

Khanra, S., Dhir, A., Kaur, P., & Joseph, R. P. (2021). Factors influencing the adoption postponement of mobile payment services in the hospitality sector during a pandemic. Journal of Hospitality and Tourism Management, 46, 26–39. https://doi.org/10.1016/j.jhtm.2020.11.004.

KPMG. (2021). The AfCFTA series: Introduction of the pan-African payment and settlement system (PAPSS) for intra-African trade. https://kpmg.com/ng/en/home/services/advisory/accounting-advisory-/introduction-of-the-pan-african-payment-and-settlement-system-intra-african-trade.html

Liebana-Cabanillas, F., & Alonso-Dos-Santos, M. (2017). Factors that determine the adoption of Facebook commerce: The moderating effect of age. Journal of Engineering and Technology Management, 44, 1–18. http://dx.doi.org/10.1016/j.jengtecman.2017.03.001

Liebana-Cabanillas, F., Munoz-Leiva, F., & Rejon-Guardia, F. (2013). The determinants of satisfaction with e-banking. Industrial Management & Data Systems, 113(5), 750–767. https://doi.org/10.1108/02635571311324188

Liebana-Cabanillas, F., Sánchez-Fernández, J., & Muñoz-Leiva, F. (2014). The moderating effect of experience in the adoption of mobile payment tools in virtual social networks: The m-payment acceptance model in virtual social networks (MPAM-VSN). International Journal of Information Management, 34, 151–166.

Michael, C. (2023). NALA enters Nigeria to drive cross-border payments. https://businessday.ng/technology/article/nala-enters-nigeria-to-drive-cross-border-payments/

Moncada, J. B., Montanez, C. G. O., Castro Jr, E. T., Romano, N. P., & Titoy, M. A. (2022). Adaptation of e-payment and its influence on consumption value among the consumers in Butuan City, Philippines. International Journal of Research publications, 109(1), 146–158. https://doi.org/10.47119/IJRP1001091920223913

Moore, G. C., & Benbasat, I. (1991). Development of an instrument to measure the perception of adopting an information technology innovation. Information Systems Research, 2(3), 192–222.

Moses-Ashike, H. (2023). Access Africa, Thunes move to improve cross-border payments in Africa. https://businessday.ng/companies/article/access-africa-thunes-move-to-improve-cross-border-payments-in-africa/

Nairametrics. (2023a). Nigeria payments system vision 2025, nationally utilised, internationally recognised. https://nairametrics.com/wp-content/uploads/2023/01/Nigeria-Payment-System-2025.pdf

Nairametrics. (2023b). E-payments sustained growth momentum in 2022. https://nairametrics.com/2022/08/29/e-payments-sustained-growth-momentum-in-2022/

National Bureau of Statistics. (2019). Micro, small and medium scale enterprises (MSME) national survey, 2017 report. https://www.nigerianstat.gov.ng/pdfuploads/SMEDAN%20REPORT%20Launch%20Presentation%202017.pdf

Niemelä-Nyrhinen, J. (2009). Factors affecting acceptance of mobile content services among mature consumers. University of Jyväskylä, Jyväskylä Studies in Business and Economics.

Okojie, J. (2022). SMEDAN moves to expand MSMEs export contribution, tackle challenges. Businessday, 19 December. https://businessday.ng/news/article/smedan-moves-to-expand-msmes-export-contribution-tackle-challenges/

Oloveze, A. O., Ogbonna, C., Ahaiwe, E. O., & Ugwu, A. O. (2022b). From offline shopping to online shopping in Nigeria: Evidence from African emerging economy. IIM Ranchi Journal of Management Studies, 1(1), 55–68.

Oloveze, A. O., Okonkwo, R. V. O., Oteh, O. U., Nwachukwu, C. P., & Chukwuoyims, K. (2022a). Cardless cash adoption and consumer psychology in a cashless market: Structural equation model (SEM) approach. Journal of Psychology and Allied Disciplines, 1(1), 19–34.

Oloveze, A. O., Oteh, O. U., Nwosu, H. E., & Obasi, R. O. (2021). How user behaviour is moderated by affected commitment on point of sale terminal. Rajagiri Management Journal, 16(1), 2–20. https://doi.org//10.1108/RAMJ-05-2020-0019

Oyelami, L. O., Adebiyi, S. O., & Adekunle, B. S. (2020). Electronic payment adoption and consumers’ spending growth: Empirical evidence from Nigeria. Future Business Journal, 6(1), 2–14. https://doi.org/10.1186/s43093-020-00022-z

Pituch, K. A., & Stevens, J. P. (2016). Applied multivariate statistics for the social sciences: Analyses with SAS and IBM’s SPSS (6th ed.). Routledge.

Poon, W. C. (2008). Users’ adoption of e-banking services: The Malaysian perspective. Journal of Business & Industrial Marketing, 23(1), 59–69.

PwC. (2020). PwC’s MSME survey 2020: Building to last. Nigeria report. https://www.pwc.com/ng/en/assets/pdf/pwc-msme-survey-2020-final.pdf

Ramos-de-Luna, I., Montoro-Rios, F., Liebana-Cabanillas, F., & Gil-de-Luna, J. (2017). NFC technology acceptance for mobile payments: A Brazilian perspective. Review of Business Management, 19(63), 82–103. https://doi.org/10.7819/rbgn.v0i0.2315

Rice, R. E., & Shook, D. (1988). Access to, usage of, and outcomes from an electronic message system. ACM, Transactions on Office Information Systems, 6, 255–276.

Rogers, E. M. (2003). Diffusion of innovations (5th ed.). The Free Press.

Rwandapost. (2023). Pan-African payment system rollout reaches three more countries. Rwandapost, 5 April. https://therwandapost.com/pan-african-payment-system-rollout-reaches-three-more-countries

Schierz, P. G., Schilke, O., & Wirtz, B. W. (2010). Understanding consumer acceptance of mobile payment services: An empirical analysis. Electronic Commerce Research and Applications, 9(3), 209–216.

Schumaker, R. E., & Lomax, R. G. (2016). A beginner’s guide to structural equation modeling (4th ed.). Routledge.

She, Z. Y., Sun, Q., Ma, J. J., & Xie, B. C. (2017). What are the barriers to widespread adoption of battery electric vehicles? A survey of public perception in Tianjin, China. Transport Policy, 56, 29–40. https://doi.org/10.1016/j.tranpol.2017.03.001.

Sheng, M., Lu, W., & Yinjun Yu. (2011). An empirical model of individual mobile banking acceptance in China. Paper presented at International Conference on Computational and Information Sciences, Chengdu, China, October 21–23; pp. 434–437.

Small & Medium Enterprises Development Agency of Nigeria and National Bureau of Statistics. (2017). National survey of micro, small and medium enterprises (MSMEs), 2017. https://smedan.gov.ng/images/NATIONAL%20SURVEY

Stanbic IBTC. (n.d.). Pan-African payment and settlement system (PAPSS) brochure. https://www.stanbicibtcbank.com/static_file/Nigeria/nigeriabank/Business

Statista Research Department. (2022). Volume of e-payment transactions in Nigeria between January and August 2020 by channel.https://www.statista.com/statistics/1178137/volume-of-e-payment-transactions-in-nigeria-by-channel/

Taiwo-Oguntu, O. (2022). SMEDAN to increase MSMEs contribution to export basket from 6% to minimum of 10%–DG. Independent, 14 December. https://independent.ng/smedan-to-increase-msmes-contribution-to-export-basket-from-6-to-minimum-of-10-dg/

Talwar, S., Dhir, A., Khalil, A., Mohan, G. & Islam, A. K. M. N. (2020). Point of adoption and beyond. Initial trust and mobile-payment continuation intention. Journal of Retailing and Consumer Services, 55,102086.

Taylor, S., & Todd, P. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144–176.

Thisday. (2023). How CBN revolutionalised payment systems in Nigeria. https://www.thisdaylive.com/index.php/2022/11/21/how-cbn-revolutionized-payment-systems-in-nigeria/

Utomo, S. M., Alamsyah, D. P., Indriana, & Susanti, L. (2022). Online customer behaviour in mobile payment e-wallet: The model of relative advantage. Journal of Theoretical and Applied Information Technology, 100(11), 3654–3663.

Venkatesh, V., Morris, M. G., Davis, G. B. & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478.

Worthington, R. L., & Whittaker, T. A. (2006). Scale development research: A content analysis and recommendations for best practices. The Counseling Psychologist, 34, 806–838. https://doi.org/10.1177/0011000006288127

Yang, S., Lu, Y., Gupta, S., Caso, Y., & Zhang, R. (2012). Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Computers in Human Behavior, 28, 129–142.

Yong, A. G., & Pearce, S. (2013). A beginner’s guide to factor analysis: Focusing on exploratory factor analysis. Tutorials in Quantitative Methods for Psychology, 9, 79–94. https://doi.org/10.20982/tqmp.09.2.p079